The Conversation (0)

Golden Deeps Ltd (ASX: GED) is pleased to announce the intersection of significant sulphide mineralisation in all three completed diamond drillholes at its 100% owned Havilah Project in the Lachlan Fold Belt Copper-Gold Province of central NSW (see Figure 1, below, and regional location, Figures 3 and 4).

Image 1: HVD003, 85.8m to 86m: semi-massive sulphide patches of copper sulphide - chalcopyrite (cpy) and zinc sulphide - sphalerite (sph) in Ordovician mafic volcanics (pXRF readings up to 18.5% Cu, 34.8% Zn* – see Appendix 3)

Image 1: HVD003, 85.8m to 86m: semi-massive sulphide patches of copper sulphide - chalcopyrite (cpy) and zinc sulphide - sphalerite (sph) in Ordovician mafic volcanics (pXRF readings up to 18.5% Cu, 34.8% Zn* – see Appendix 3)

*Cautionary Note in relation to disclosure of visual estimates and pXRF readings described in this release and detailed in Appendix 2 and 3 respectively: The Company cautions that visual estimates of sulphide mineralisation abundance and pXRF readings should never be considered a proxy or substitute for laboratory analyses. Laboratory assays (ICP MS/OES and Fire Assay for gold) are required to determine representative grades and intervals of the elements associated with the visible mineralisation reported from geological logging and pXRF readings. Core is being sampled for submission to ALS laboratories in Orange, NSW. Laboratory analytical results are expected within 3 to 6 weeks.

Golden Deeps CEO Jon Dugdale commented: “The intersection of sulphide mineralisation in all three initial holes at Havilah, including thick zones of copper and zinc sulphide mineralisation in HVD003, indicates we’re on top of a large porphyry-sulphide system with similar characteristics to other major copper-gold discoveries in the Lachlan Fold Belt such as Cadia-Ridgeway and the recent Boda-Kaiser discovery.

“We look forward to completing the remainder of our diamond drilling program and receiving the laboratory results from the holes completed, which will be released as soon as they come to hand and are compiled.”

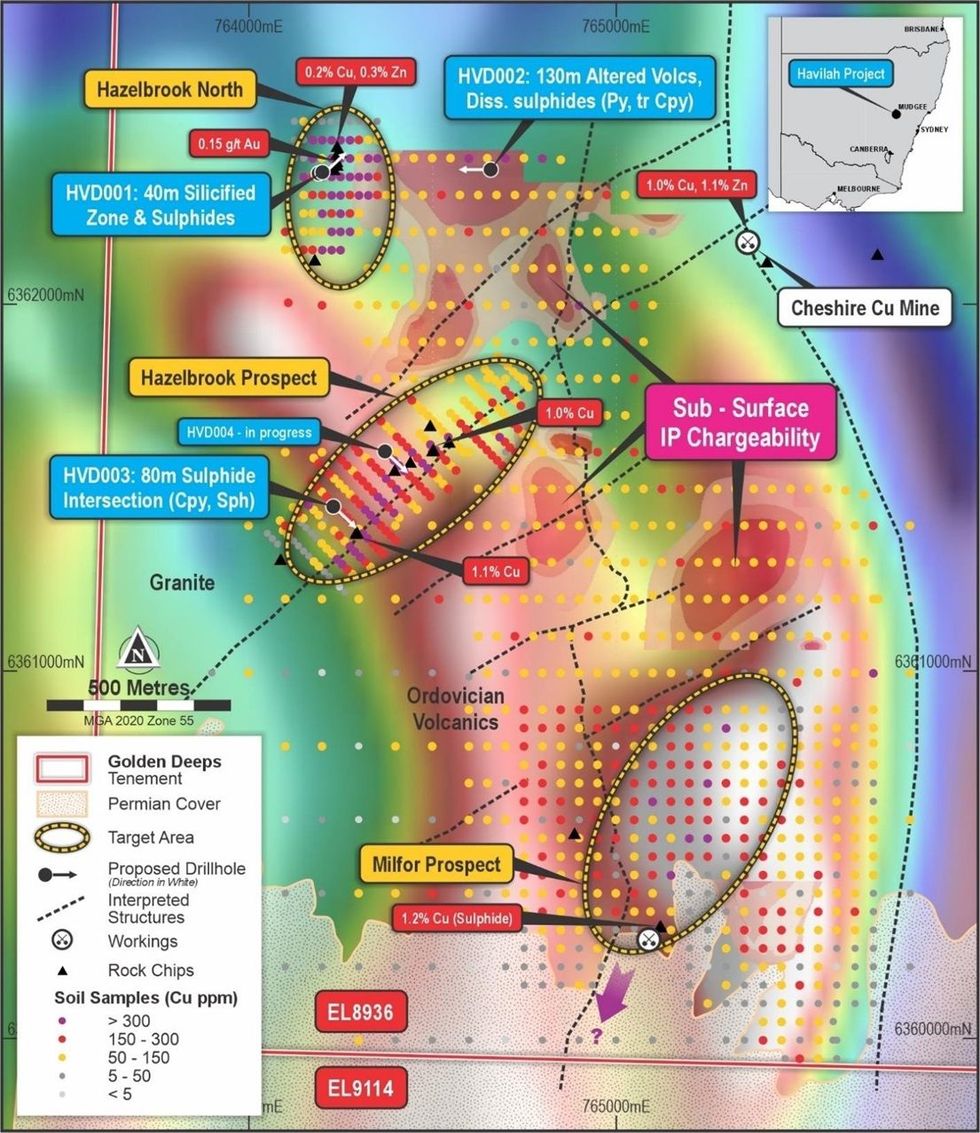

Figure 1: Havilah Project, soil and rockchip copper anomalies on magnetics image with current drilling

Figure 1: Havilah Project, soil and rockchip copper anomalies on magnetics image with current drilling

The third hole of the program, HVD003, tested the Hazelbrook target where an extensive northeast-southwest trending copper-zinc soil anomaly has been defined with rockchip values of over 1% Cu3 (Figure 1).

HVD003 intersected a sulphide mineralised zone from 85m to 119m which included patches and stringers (averaging 1-2%) of the copper-sulphide - chalcopyrite and the zinc-sulphide - sphalerite. These patches occur within extensively altered (Ordovician) mafic volcanic/volcanoclastic rocks with disseminated chalcopyrite-sphalerite-pyrite mineralisation which occurs from 85m to 166m (over 80m) (see Appendix 2).

The mineralisation aligns with the surface soil and rockchip copper-zinc anomaly, striking northeast, dipping to the northwest, and the drilling intersection approximating true width (see cross section, Figure 2, below).

Click here for the full ASX Release

This article includes content from Golden Deeps, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.