The Conversation (0)

Galena Mining Ltd. (“Galena” or the “Company”) (ASX:G1A) announces achievement of the key objectives from the 2020 Abra Drilling Program and has subsequently completed an updated JORC Code 2012 Mineral Resource estimate (“April 2021 Resource”) for the Abra Base Metals Project (“Abra” or the “Project”) located in the Gascoyne region of Western Australia. The April 2021 Resource has been independently prepared by Optiro Pty Ltd (“Optiro”).

Managing Director, Alex Molyneux commented, “The objectives associated with the 2020 Abra Drilling Program were successfully completed. The Project now has over 100 kilometres of drilling in its database, and the geological confidence and understanding of the deposit continues to improve. Almost all of the new holes were drilled within the previous Mineral Resource envelope and over 75% of those holes achieved expected or better results. This Mineral Resource update will now feed into an optimised mine plan, and mine development will allow for underground drilling to continue Resource development, particularly the conversion of significant Inferred Mineral Resources associated with the Core Zone

mineralisation, which remains open in several directions and also hosts the interpreted copper-gold zone.”

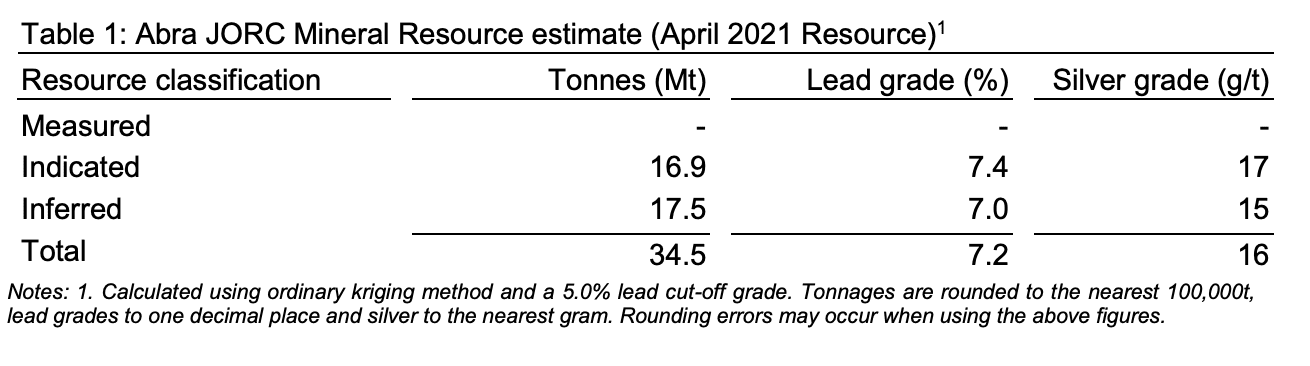

Table 1 (below) states the Abra April 2021 Resource at a 5.0% lead cut-off grade.

2020 ABRA DRILLING PROGRAM AND OBJECTIVES

The completed 2020 Abra Drilling program included 57 drill-holes totalling 24,834 cumulative linear meters and was designed to achieve three specific objectives. These objectives were mainly focussed on the original Mineral Resource estimate and potential grade and continuity risk

of certain areas within that estimate, and they were:

(i) Lead-silver orebody infill drilling – Some infill drilling that had previously been planned to take place from underground once the decline was in place was pulled forward into the 2020 Abra Drilling Program. This aimed to further tighten the drill-hole spacing over the first four years of proposed production to 20 by 20 metres and up to 30 by 30 metres or better, compared with a more variable drilling density of up to 40 by 40 metres and up to 60 by 60 metres in that area previously.

(ii) Drilling into selected lead-silver ‘metal rich’ zones – Some drill-holes successfully targeted selected areas within the Abra lead-silver mineralisation where higher concentrations of metal (in both grade and thickness) were projected from previous drilling campaigns, in particular drill-hole AB147, which became the best high-grade lead-silver drill-hole ever at Abra, and the follow-up drill-holes that were added to the program in its vicinity (see Galena ASX announcements of 19 October 2020, 18 November 2020, 22 January 2021 and 24 February 2021).

(iii) Gold-copper exploration – Some of the drilling, in particular drill-hole AB195 (see Galena ASX announcement of 22 February 2021) successfully targeted the newly interpreted gold and copper drilling targets to the south and south east of the leadsilver mineralisation and at depth (see Galena ASX announcement of 29 June 2020).

The first two of these objectives enable the Company to optimise mine planning, which is now underway.

MINERAL RESOURCES

Geological model

Abra is located in the Gascoyne region of Western Australia within clastic and carbonate sediments of the Proterozoic Edmund Group. Abra is a base metals replacement-style deposit, where the primary economic metal is lead. Silver, copper, zinc and gold are also present within

the established lead mineralised zones but are of lower tenor.

Abra can be divided into two main parts, the upper “Apron Zone” and lower “Core Zone”.

The Apron Zone comprises stratiform massive and disseminated lead sulphide (galena), with minor copper sulphide (chalcopyrite) and zinc sulphide (sphalerite) mineralisation within the lower conglomerate unit (KCLC) of the Edmund Basin Kiangi Creek Formation and the Upper

Carbonate Unit (UID) of the Irregully Formation. The Apron Zone is characterised by flat-lying alteration zones containing jaspilite (Red Zone), barite (Barite Zone), silica-sericite (Micrite Zone), siderite and dolomite (Carbonate Zone), and haematite and magnetite (Black Zone). Distinct stratiform alteration domains can be defined within the Apron Zone and have assisted in the definition of the distribution of the lead mineralisation and construction of the lead mineralisation lodes. The Apron Zone extends for over 1,200 metres along strike and 750 metres down dip, dipping gently south.