The Conversation (0)

Warriedar Resources Limited (ASX: WA8) (Warriedar or the Company) is pleased to provide an update on drilling progress and release the first results from diamond drilling undertaken at the Ricciardo deposit within its Golden Range Project, located in the Murchison region of Western Australia (Figure 1).

HIGHLIGHTS:

This is the first diamond drill program at Ricciardo since 2014, when just three (3) diamond holes were drilled by the previous operator.

The results reported in this release are for four (4) (255m) of the 16 (1420m) diamond holes drilled to date. Approximately 2,200m of diamond drilling is planned as part of the current phase of combined RC and diamond drilling at Ricciardo and M1.

The results from these initial four diamond holes extend the high-grade shoot below the Silverstone North pit and infill a previous gap in the high-grade zone of the MRE below the northern part of the Ardmore pit (adding confidence and continuity to the MRE in this area).

These outcomes, while stemming from only a small part of the overall current phase of drilling, continues to demonstrate the outstanding MRE growth potential that exists at Ricciardo and along the broader ‘Golden Corridor’ trend.

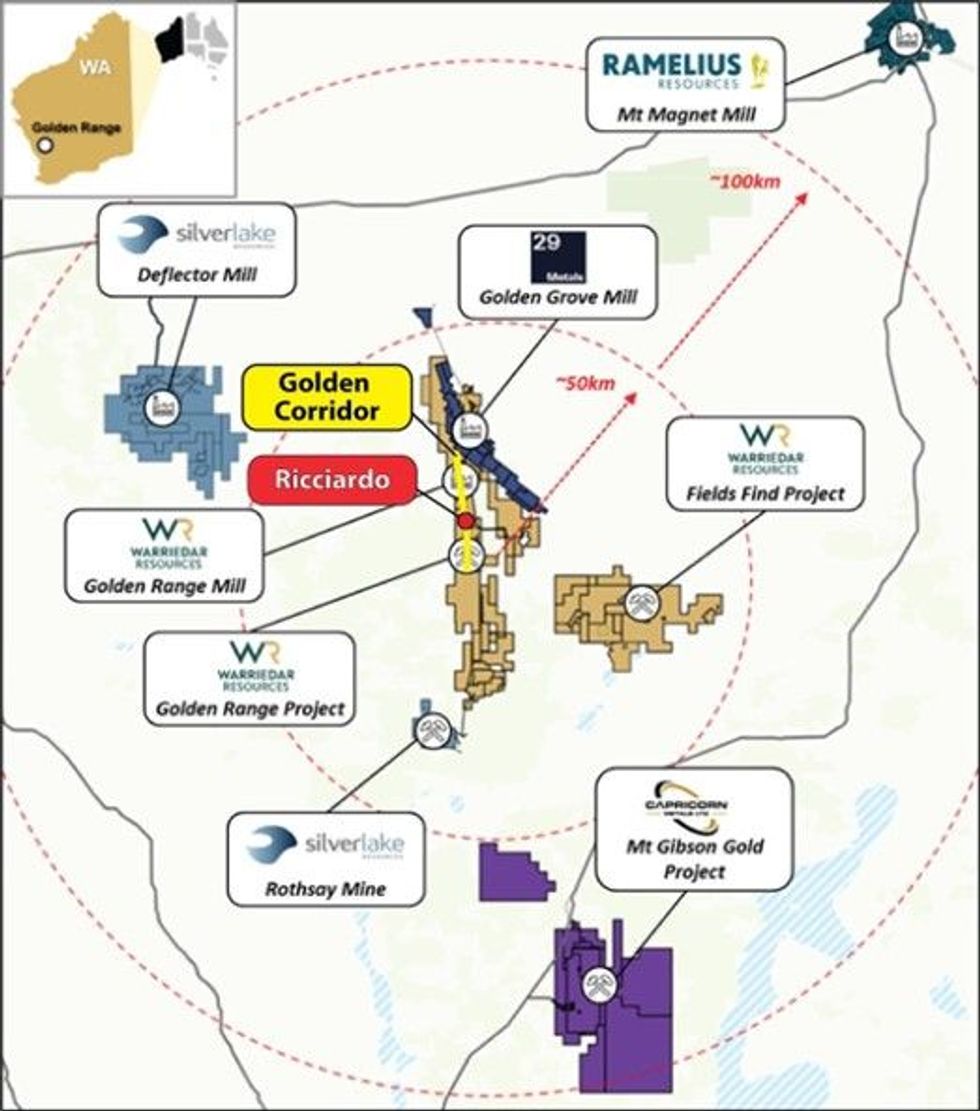

Figure 1: The Golden Range and Fields Find Projects Mines and projects within trucking distance of the Warriedar tenure are shown. The location of the Ricciardo deposit within the 25km-long ‘Golden Corridor’ at the Golden Range Project is annotated

Figure 1: The Golden Range and Fields Find Projects Mines and projects within trucking distance of the Warriedar tenure are shown. The location of the Ricciardo deposit within the 25km-long ‘Golden Corridor’ at the Golden Range Project is annotated

The Ricciardo gold system (within the Golden Range Project) spans a strike length of approximately 2.3km, with very limited drilling having been undertaken below 100m depth. Ricciardo possesses a current Mineral Resource Estimate (MRE) of 8.7 Mt @ 1.7 g/t Au for 476 koz gold.1 The oxide material at Ricciardo has been mined by previous operators.

Click here for the full ASX Release

This article includes content from Warriedar Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.