The Conversation (0)

Metals Australia Ltd (ASX: MLS) (“Metals Australia” or “the Company”) is pleased to announce that drilling is set to commence to test priority targets identified at the Company’s Big Bell North tenements (EL51/2058 and EL51/2059) in Western Australia’s world-class Murchison Gold Province. The tenements lie within the regional structural corridor which hosts major gold deposits including the Meekatharra and Mt Magnet gold mining centres (Figure 2).

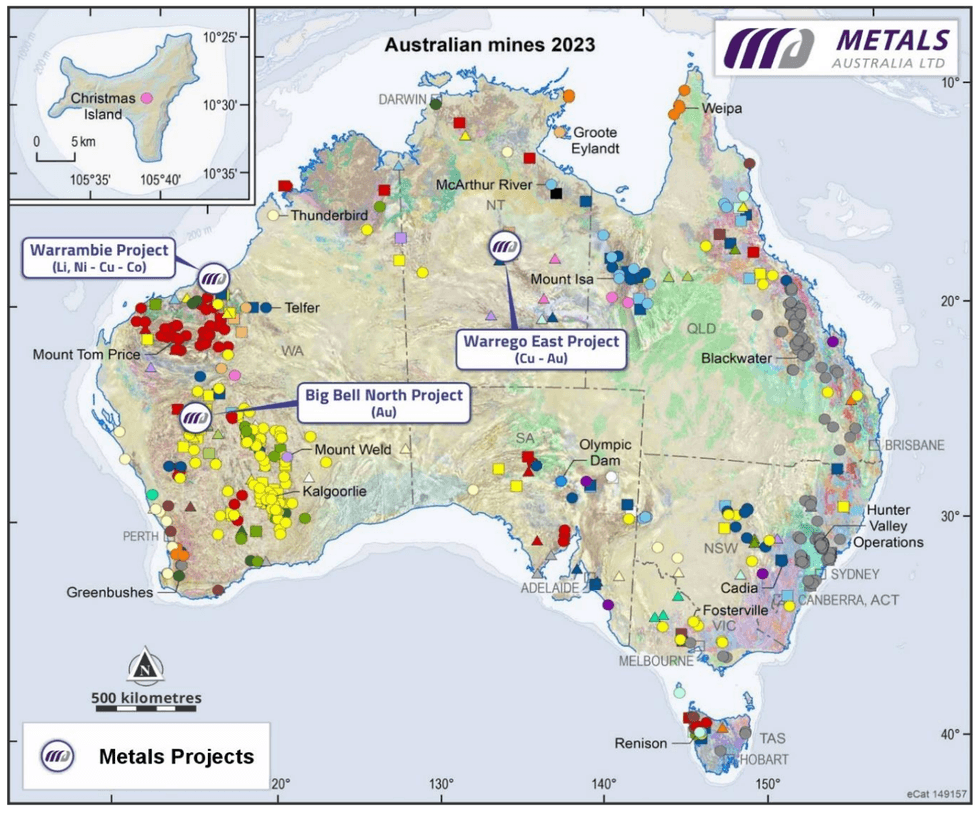

Figure 1: Metals Australia - Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)

Figure 1: Metals Australia - Critical Minerals and gold exploration projects in world-class mineral terranes (adapted from Geoscience Australia, Australian Mineral Deposits)

Metals Australia Ltd CEO Paul Ferguson commented:

“The drilling program we are set to commence at our highly prospective Big Bell North gold project in Western Australia’s prolific Murchison Gold Province is the latest step in the Company’s aggressive push to unlock value from our suite of gold and critical mineral projects, which are all located in wellestablished mining regions in Australia and Canada.”

Our Big Bell North project, where there has been no modern-day exploration, has advanced rapidly during 2024 on the back of a methodical, phased exploration approach from our geological team. This started with an extensive fixed wing aeromagnetic survey covering over 5,200-line km which yielded two interpreted shear zones of significance.

We followed this up with detailed gravity survey work, which revealed the likelihood of greenstones within the shear zones. This is significant because gold mineralisation within the Murchison domain is often concentrated within such greenstone belts and is structurally controlled, thus enhancing the potential of the targets we are now set to drill.

In addition to Big Bell North, we continue to advance plans for an extensive soil survey and follow-on drilling program at the Warrego East copper-gold project in the Northern Territory, which is on track to commence later this year, ahead of the wet season, once permitting and land access arrangements are finalised.

We are also awaiting results and interpretation from two other recently completed exploration programs at Warrambie in the Pilbara, where our aircore drilling program has been completed; and our Corvette River project in Quebec’s James Bay region in Canada, where assay results from the phase one field program are imminent. Exploration at Corvette River is extensively focused on gold, silver, base metals (Cu-Pb-Zn) and lithium.

At our flagship Lac Carheil high-grade flake graphite project in Quebec, positive dialogue continues as we seek to build alignment on the project’s benefits with all stakeholders. Our significant cash reserves leave us well-placed to accelerate our various exploration programs as we continue striving to unlock the true value of our suite of projects in Australia and Canada.”

Click here for the full ASX Release

This article includes content from Metals Australia, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.