The Conversation (0)

Tartana Minerals Limited (ASX: TAT) (the Company) is pleased to advise that it has entered into a non-binding term sheet to acquire a private explorer, Queensland Strategic Metals Pty Ltd (QSM) (the Acquisition).

Highlights:

Completion of the Acquisition remains subject to formal documentation being executed and shareholder approval by Tartana’s shareholders for the purposes of ASX Listing Rule 10.1, 10.11, and 7.1 (further detailed below), amongst other conditions precedent. There can be no assurances that the transaction will complete until such time that all conditions precedent have been met. A summary of the terms of the non-binding agreement is set out at Annexure A.

Acquisition Rationale

QSM’s EPMs and ML are located Far North Queensland and are complementary to Tartana’s existing exploration portfolio with two copper projects with high grade copper surface mineralisation as well as several EPMs covering critical mineral prospects. The critical mineral EPMs are in proximity to Tartana’s own Herberton (Emuford) EPM Application (EPMA 27220) and are part of move by Tartana to increase its exposure to tin, tungsten and silver and other critical metals.

With Tartana’s Copper Sulphate production continuing to produce healthy cash flows, the Company has also been focused on investigating the development of primary copper mineralisation at the Tartana open pit as well as increasing its exploration portfolio to incorporate additional and complementary projects targeting copper and critical metals. While the former has involved drilling a metallurgical hole (D15) and completing metallurgical test work (flotation recoveries and ore sorting), the opportunity to acquire QSM addresses the latter.

About QSM

QSM has, over the course of recent years aggregated ten EPMs and one ML covering 771 km2 in Far North Queensland (See Figure 2). QSM has acquired the tenements through a series of transactions with tenure holders with a focus on discovery of hardrock critical and strategic metal projects, particularly tin, tungsten and copper.

In some cases the vendors of these tenements have held them for a significant period of time with a focus on alluvial mining over hard-rock exploration. QSM was able to secure attractive terms to acquire these tenements by leaving the alluvial rights in the hands of the vendors or Queensland Alluvial Resources Pty Ltd (further detailed below).

QSM has 7 project areas which are listed in Figure 1. Each project area contains prospects recorded by the Queensland Department of Resources and these are listed under each project/EPM. The dominant metal associated with each project is colour coded with many relating to the minor metals; tin, tungsten and antimony.

While there are many prospects in several of the permits, QSM has completed site visits and discussed the various prospects with ‘old time miners’ to establish which particular projects offer potential scale and potential unmined mineralisation. These projects are in bold in Figure 1.

Figure 1. QSM tenure and various prospects. QSM has prioritised the projects which are identified in bold.

Figure 1. QSM tenure and various prospects. QSM has prioritised the projects which are identified in bold.

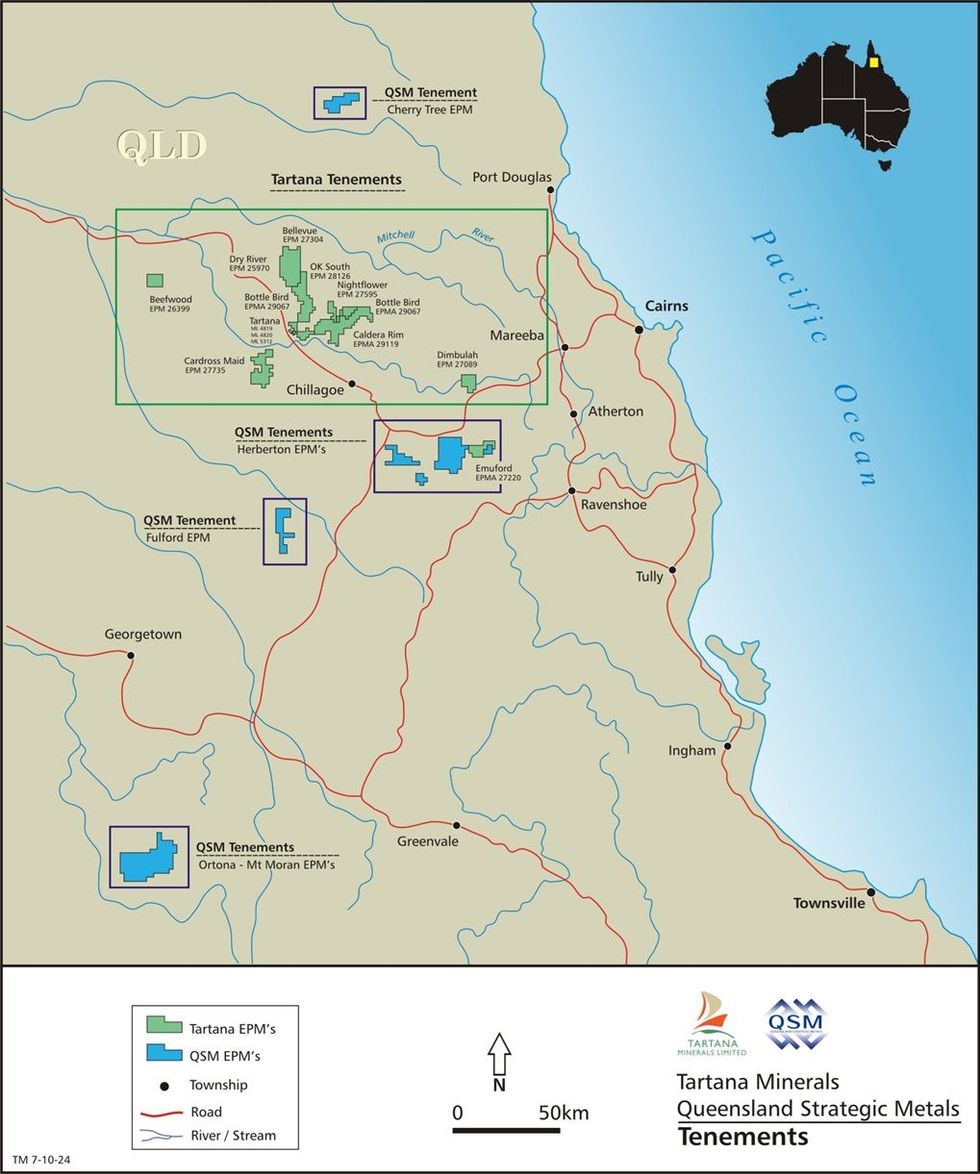

Figure 2. Tartana and QSM EPMs.

Figure 2. Tartana and QSM EPMs.

A detailed project review has been provided at Annexure B.

Click here for the full ASX Release

This article includes content from Tartana Minerals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.