The Conversation (0)

Flynn Gold Limited (ASX: FG1, “Flynn” or “the Company”) is pleased to announce a maiden JORC compliant Exploration Target for the Trafalgar, Brilliant and Link Zone prospects at its 100%-owned Golden Ridge Project in North-east Tasmania.

Highlights

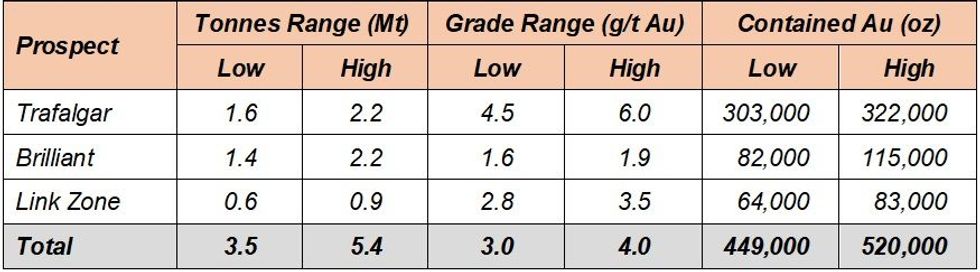

The combined Exploration Target range is listed in Table 1:

Table 1 – Combined Exploration Target for Trafalgar, Brilliant and Link Zone

Table 1 – Combined Exploration Target for Trafalgar, Brilliant and Link Zone

Flynn Gold’s Managing Director and CEO, Neil Marston states: “Following several successful drill campaigns testing the gold mineralisation at Golden Ridge, we are pleased to report an initial JORC-compliant Exploration Target for the Trafalgar, Brilliant and Link Zone prospects.

“The Exploration Target is open in all directions and encompasses less than 30% of the known gold anomalism at Golden Ridge which highlights the substantial future growth potential of this exciting project.

“This is a significant step toward our next goal of defining a maiden JORC Mineral Resource for the project. There is potential to significantly increase the tonnage and grade at Golden Ridge with in-fill and expansion drilling, which will be a major focus for the Company during 2025.”

Exploration Target

The Golden Ridge Project is located within EL17/2018 in North-east Tasmania (see Figure 7).

Flynn has calculated JORC compliant Exploration Targets for the Trafalgar, Brilliant and Link Zone prospects at Golden Ridge dated 8th November 2024. Table 2 below provides a summary of the Exploration Targets for each prospect:

Table 2 - Exploration Targets for Trafalgar, Brilliant and Link Zone prospects at the Golden Ridge project.

Table 2 - Exploration Targets for Trafalgar, Brilliant and Link Zone prospects at the Golden Ridge project.

The combined Exploration Target only encompasses areas where Flynn has drill-tested vein mineralisation at locations shown in Figure 1 and does not include areas of anomalous soil geochemistry, which the Company considers to be highly prospective for gold mineralisation and intends to drill-test in the future.

The drill-tested Trafalgar, Brilliant and Link Zone prospects define a significant zone of gold mineralisation extending over a strike length of approximately 3km, which is contained within a broader 9km zone of gold anomalism that trends along the contact between the Golden Ridge granodiorite and the Mathinna supergroup metasediments (Figures 1 - 3).

Potential gold vein extensions at Trafalgar and Brilliant ,defined by anomalous gold-in-soil geochemistry along strike of and surrounding the Exploration Target veins, were not included in the Exploration Target calculation.

Work is currently in progress to in-fill these areas with soil sampling and trenching prior to exploration drill-testing.

Click here for the full ASX Release

This article includes content from Flynn Gold, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.