The Conversation (0)

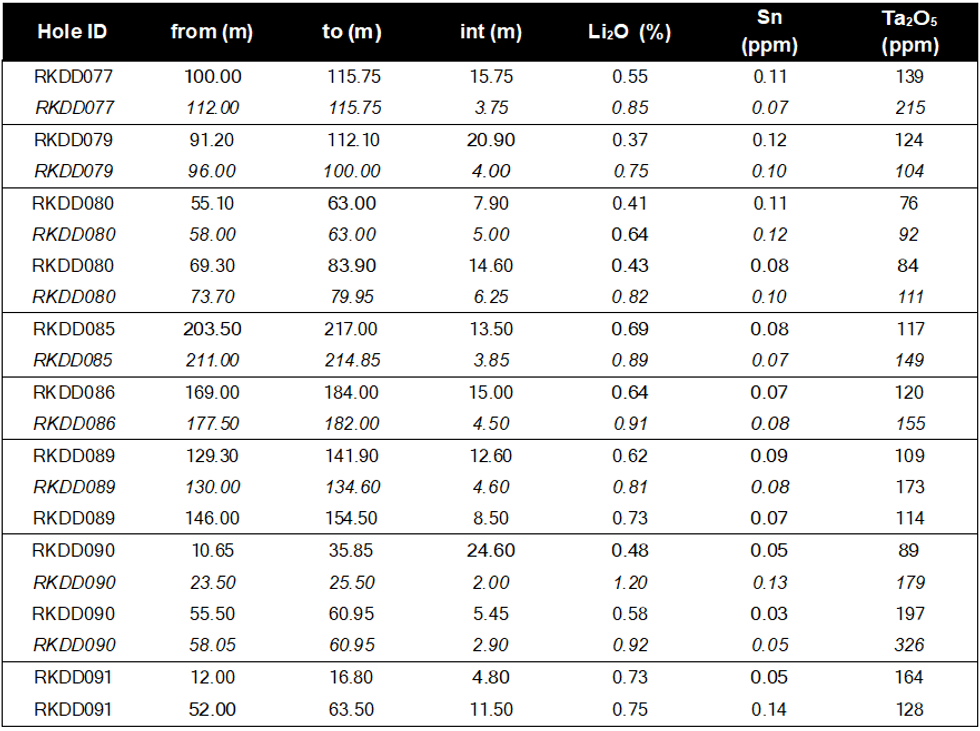

Battery and critical metals explorer and developer Pan Asia Metals Limited (ASX: PAM) (‘PAM’ or ‘the Company’) is pleased to provide an update for eighteen (18) more drill holes completed at the Reung Kiet lithium prospect. Results continue to support thegeological model of extensive lithium mineralisation hosted in lepidolite rich pegmatite dykes-veins and adjacent metasediments. The mineralised zone is currently defined over a strike length of plus 1km and remains open along strike to the north and south, and at depth especially in the south.

HIGHLIGHTS

Pan Asia Metals Managing Director Paul Lock said: “We near the end of the drilling program at the Reung Kiet Lithium Prospect and the results remain very positive with the step out drilling continuing to demonstrate extensions at depth and along strike of the existing Mineral Resource and the infill drilling supporting and enhancing the existing Mineral Resource. The results at the southern end of the prospect are particularly good. Final assays required for the updated Mineral Resource will be received shortly and then CSA Global will start the required modelling and estimation work. A move to Bang I Tum is imminent and then we can start our diamond drilling program there to test the Exploration Target as well as the extension zone as previously reported. We are quite excited about this program; non-selective rock chip and channel assays were some of the highest received at Reung Kiet, with 44 of 64 samples average 1.56% Li2O at a 0.30% Li2O cutoff, 35 samples were greater than 1.00% Li2O, 12 samples greater than 2.00% Li2O and the maximum grade was 2.62% Li2O.”

The Reung Kiet Lithium Project (RKLP) is one of PAM’s key assets. RKLP is a hard rock lithium project with lithium hosted in lepidolite/mica rich pegmatites chiefly composed of quartz, albite, lepidolite and muscovite, with minor cassiterite and tantalite as well as other accessory minerals. Previous open pit mining extracting tin from the weathered pegmatites was conducted into the early 1970’s.

PAM’s objective has been to continue drilling with the aim of increasing and upgrading the existing Mineral Resource, which will then be used as part of a Pre-Feasibility Study that will consider various options to determine the technical and economic viability of the project including the production profile of lithium carbonate and or lithium hydroxide and associated by-products. PAM is focusing on lepidolite as a source of lithium as peer group studies indicate that lithium carbonate and lithium hydroxide projects using lepidolite as their plant feedstock have the potential to be placed near the bottom of the cost curve. Lepidolite has also been demonstrated to have a lower carbon emission intensity than other lithium sources.

Click here for the full ASX Release

This article includes content from Pan Asia Metals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.