The Conversation (0)

Latin Resources Limited (ASX: LRS) (“Latin” or “the Company”) is pleased to provide an update for recent activities and next steps in relation to the advancement of its 100% owned Cloud Nine Halloysite‐Kaolin Deposit (“Cloud Nine”) in Western Australia. The Company released its maiden Mineral Resource Estimate (“MRE”) of 207Mt Inferred Resources at Cloud Nine in May 20211.

HIGHLIGHTS

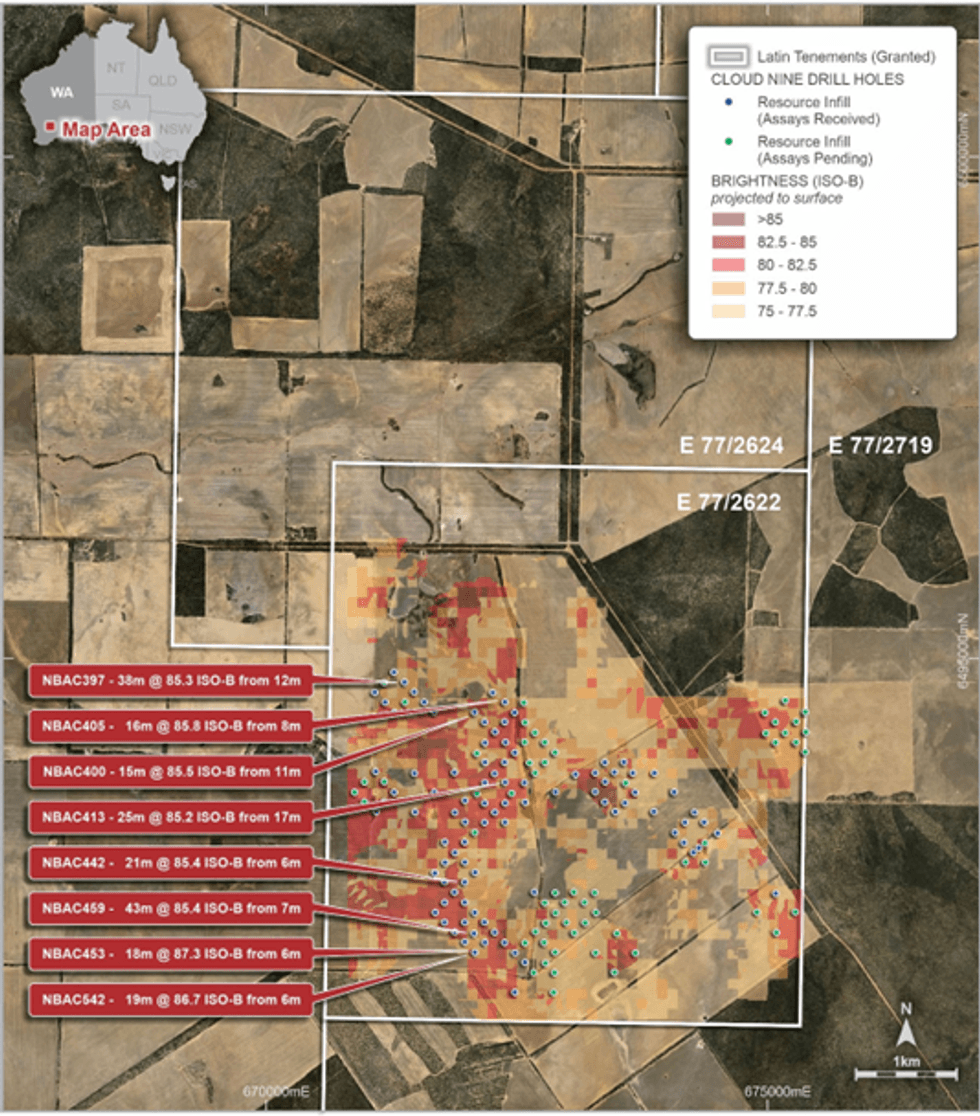

To date, nearly two thirds of the composites from the Cloud Nine Resource in‐fill drilling program have been analysed for brightness (Figure 1). The remaining holes’ sample analysis has benefited from optimising the analysis pathway, coupled with a drop in COVID‐related staffing issues at the laboratory. The remaining results are expected towards the end of July.

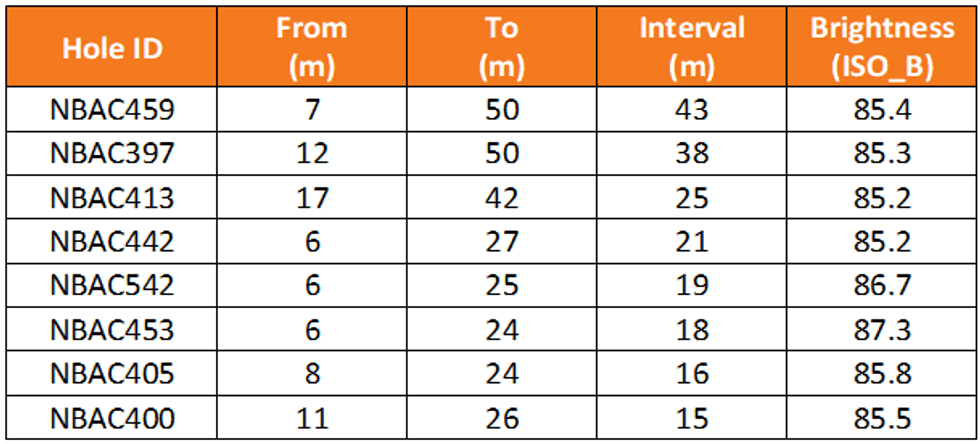

The drilling thus far2 has returned significant, near surface thicknesses of kaolinised granite with brightness values above 85 ISO‐B. A total of 66% of the drill holes analysed so far, returned results above 80 ISO‐B, with selected significant results >85 ISO‐B including:

Table 1: Selected significant Cloud Nine kaolin brightness intersections (>85 ISO‐B)

Figure 1: Drillholes with brightness results received and pending, from the Cloud Nine Resource in‐fill drilling

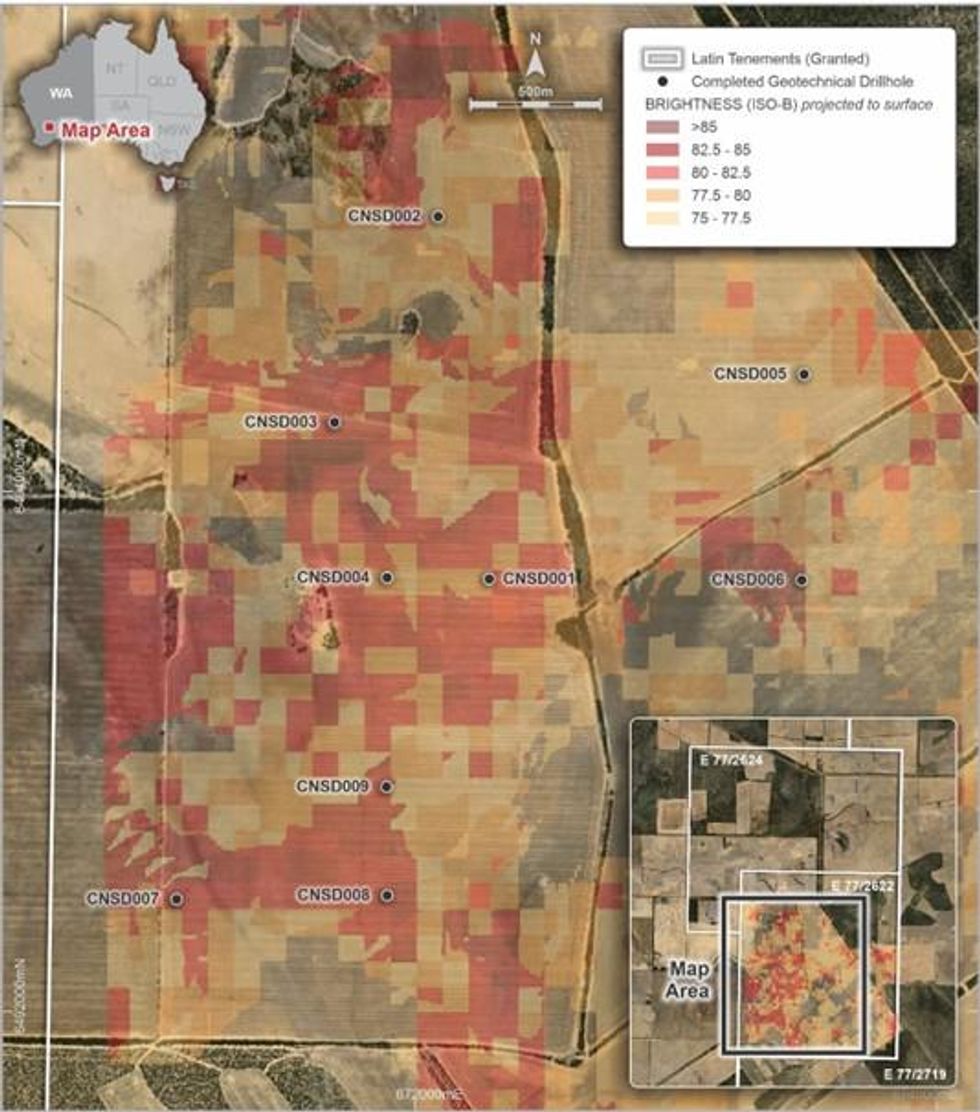

SONIC GEOTECHNICAL DRILLING

The recently completed sonic geotechnical drilling program, comprising 9 PQ (85mm) drill holes for 365 metres, was designed to provide representative core samples from within the footprint of the existing JORC MRE (Figure 2).

The in‐situ dry bulk density data is an integral part of the ongoing resource estimation work at Cloud Nine and will improve the confidence levels in the current Inferred JORC Resource, while the geotechnical data is required for the mine design and scheduling work currently underway as part of the Company’s Pre‐Feasibility Studies (“PFS”) and other studies.

Figure 2: Cloud Nine – location of sonic drill collars

REGIONAL AEROMAGNETIC SURVEY

The Company has engaged Southern Geoscience Consultants (SGC) to manage a high detail airborne magnetic and radiometric survey covering the Company’s extensive regional tenement package (Figure 3). The regional survey will assist in defining further exploration targets along almost 105 kilometres of prospective tenure and comprises over 13,800 line kilometres on 50 metre spaced east west lines.

Click here for the full ASX Release

This article includes content from Latin Resources Limited (ASX: LRS), licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.