The Conversation (0)

DY6 Metals Ltd (ASX: DY6, “DY6” or “Company”), a strategic metals explorer targeting Heavy Rare Earths (HREE) and critical metals in southern Malawi, is pleased to announce the assay results from the 8-diamond drill (DD) holes (totalling 900m) at its flagship Machinga Project in southern Malawi.

HIGHLIGHTS

The Company’s CEO, Mr Lloyd Kaiser said:

“The assay results are showing outstanding intersections across multiple drill holes, especially MMD007 returning 15.1m @ 1.01%TREO with substantial Niobium grade, and a high proportion of valuable heavy rare earth elements from holes drilled for metallurgical material. The successful RC and DD drilling program has greatly improved the geological team’s interpretation of the Machinga system including the structural and lithological controls. The final assay results and historic intersections will feed into our current geological model to guide our next exploration program design. The Company now moves towards progressing a technical evaluation of the mineralisation to target a REO concentrate and Niobium by-product”.

A strongly mineralised hydrothermal breccia system striking NW-SE and dipping shallowly ~35° to the NE has been confirmed by the recent drilling. Pleasingly, very high-grade zones have been intersected from the diamond drill holes, as well as the suggestion of the mineralised zones thickening at depth and open to the NE. Significant drill intercepts received from the final batch of assays are included in Table 2. Significant intercepts include:

(Results returned an average of 29% HREO:TREO and 3.6% DyTb:TREO at a cutoff grade of >0.25%TREO)

Diamond drill holes MDD006, MDD007 and MDD008 were drilled downdip to obtain sufficient sample material to initiate the metallurgical test work program in Q1, 2024. The assay results are positive and significant for the Company as they continue to demonstrate continuity of mineralisation down dip and along strike of Machinga with excellent width and grade of mineralisation for a heavy rare earth rich deposit. As part of the upcoming metallurgical test work program, using core from this campaign, the Company will assess the amenability of the mineralisation to be treated through a relatively simple beneficiation process.

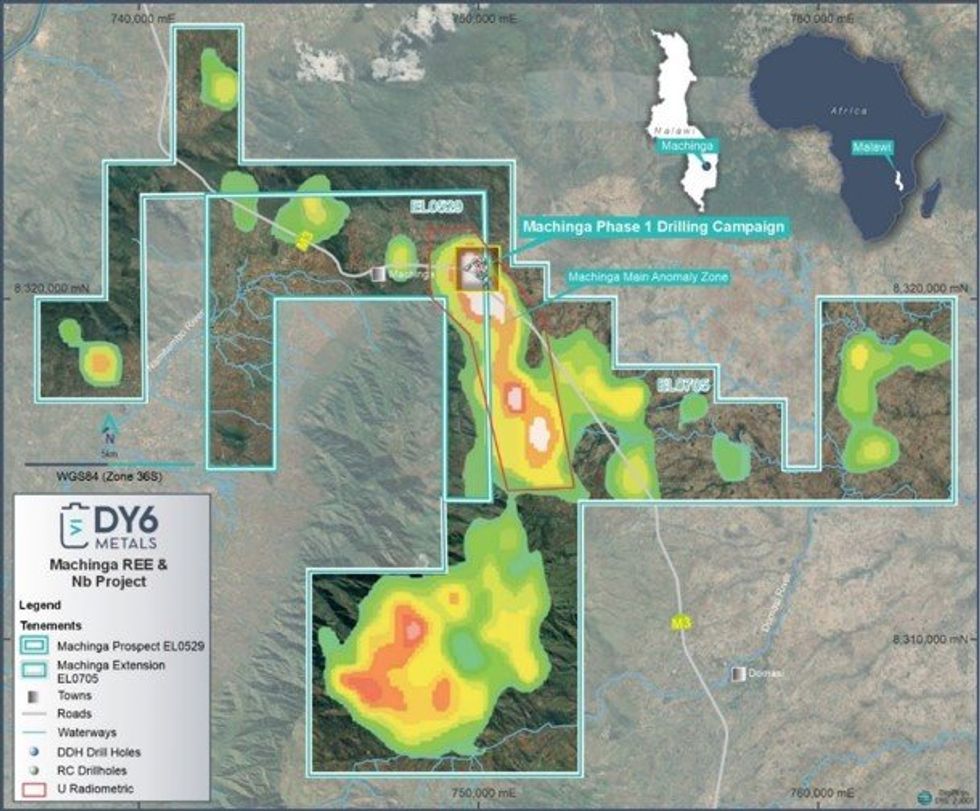

Figure 1. Machinga Project location in Southern Malawi (U radiometric)

Figure 1. Machinga Project location in Southern Malawi (U radiometric)

The diamond drill program consisted of 5 holes to 150m and 3 holes to 50m depths to determine the structural setting and geology of the Machinga deposit and to obtain material for initial metallurgical studies.

The first 5 holes were to understand the geological nature of the deposit, its structural configuration and obtain contextual data to the results of the RC drillholes, both recent and historical.

Click here for the full ASX Release

This article includes content from DY6 Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.