The Conversation (0)

GTI Energy Ltd (ASX: GTR) (GTI or Company) is pleased to advise of positive results from the recently completed airborne radiometric and magnetic survey completed at its 100% owned Green Mountain Project (Project) located in Wyoming’s prolific Crooks Gap/Green Mountain/Great Divide Basin uranium production district.

GTI Executive Director Bruce Lane commented “The aerial geophysical survey has provided us with clear direction as to where to drill at Green Mountain. We have been able to utilise the historical drilling and geological information completed by Kerr McGee Corporation, Wold Nuclear and others during the 1970’s and 1980’s to help interpret and extrapolate significant additional anomalous uranium trends, particularly within the eastern part of the extensive Green Mountain land position. The land package is surrounded by significant uranium deposits and resources owned by Rio Tinto, Energy Fuels, Ur Energy & UEC, so we know we are in an area with real potential. Our next step is to progress work on refining drill targets and permitting”.

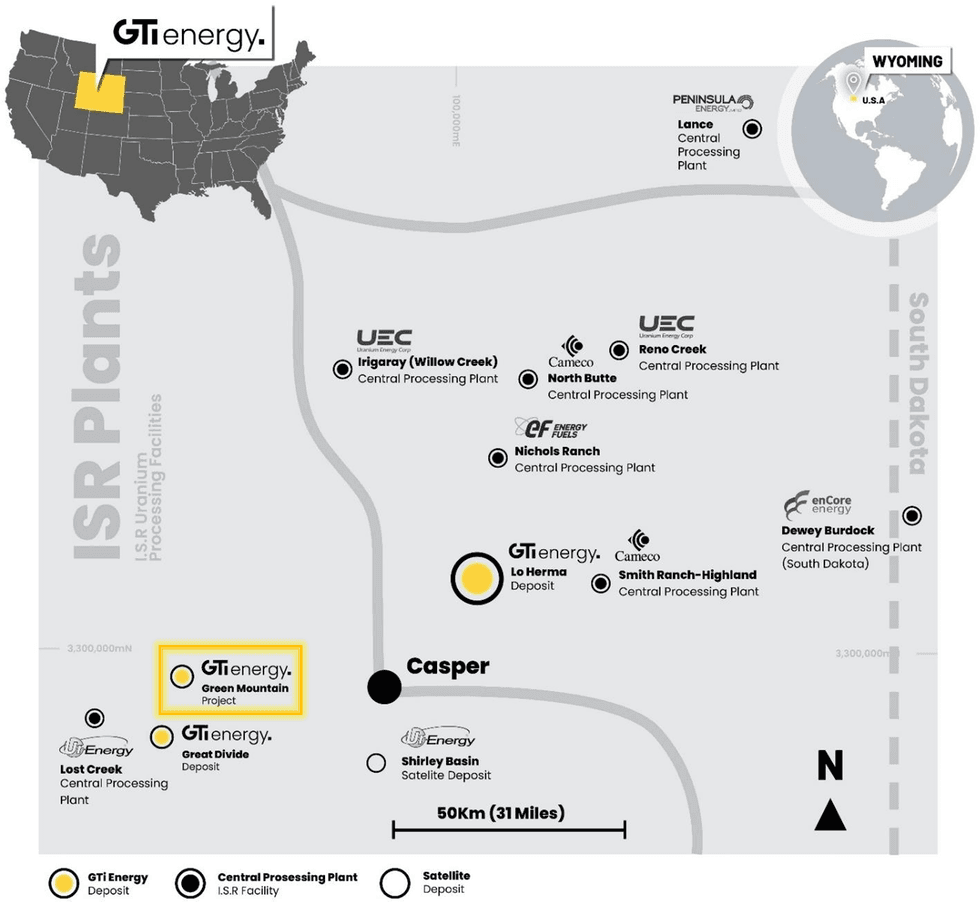

GTI’s 100% owned Green Mountain ISR Uranium Project (Green Mountain) is located in Sweetwater County, Great Divide Basin (GDB), Wyoming (WY) within a few miles of GTI’s Great Divide Basin projects and within 60 miles of GTI’s Lo Herma project in Wyoming’s Powder River Basin (Figure 1).

FIGURE 1. GTI WYOMING PROJECT LOCATIONS & URANIUM PROCESSING PLANTS 1

FIGURE 1. GTI WYOMING PROJECT LOCATIONS & URANIUM PROCESSING PLANTS 1

GTI’s Green Mountain Project covers ~14,000 acres (~5,665 hectares) of underexplored mineral lode claims (Claims) and benefits from historical Kerr McGee uranium drilling data and oil-well exploration drill logs which confirm the presence of roll fronts within the Battle Springs formation which hosts neighbouring major uranium deposits.

The Properties are located in the neighbourhood of Energy Fuel’s (EFR) 30Mlb Sheep Mountain deposit, Ur-Energy’s (URE) 14Mlb Lost Soldier ISR deposit, UEC’s (UEC) Antelope deposit & Rio Tinto’s (RIO) Big Eagle (past producing), Jackpot, Desert View, Phase II, & Willow Creek deposits (Figure 2). The Claims lie south of Green Mountain, ~5kms from GTI’s existing Odin claim group & within 15km of GTI’s Thor project where two successful drill programs were completed during 2022.

Click here for the full ASX Release

This article includes content from GTI Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.