The Conversation (0)

Australian-owned Firebird Metals Limited (ASX: FRB, Firebird or the Company) is pleased to announce that it has been granted Mining Lease 52/1086 for the Company’s 100% owned Oakover Manganese Project, located 85km east of Newman.

HIGHLIGHTS

Firebird Managing Director, Mr Peter Allen, commented: “The granting of Mining Lease 52/1086 is a significant milestone for Firebird and the Oakover Project, marking an important step in our long- term downstream processing and vertical integration strategy.

“Oakover is a large and near-surface manganese project with robust economics and an 18-year Life-of- Mine. Our vision is to become a global leader in the manganese industry by seamlessly integrating our mining operations and innovative downstream processing solutions, to support the advancement of the Li-ion and Na-ion battery sectors. The location of our proposed manganese sulphate plant in China, places us at the forefront of this market and with the integration of Oakover will allow us to maintain a competitive advantage by ensuring a 100% owned and secure supply of high-quality manganese feedstock.

“Securing this lease brings us closer to that goal, providing a foundation for out stage two, low-cost manganese-based cathode material operations which is underpinned by the successful development of Oakover.”

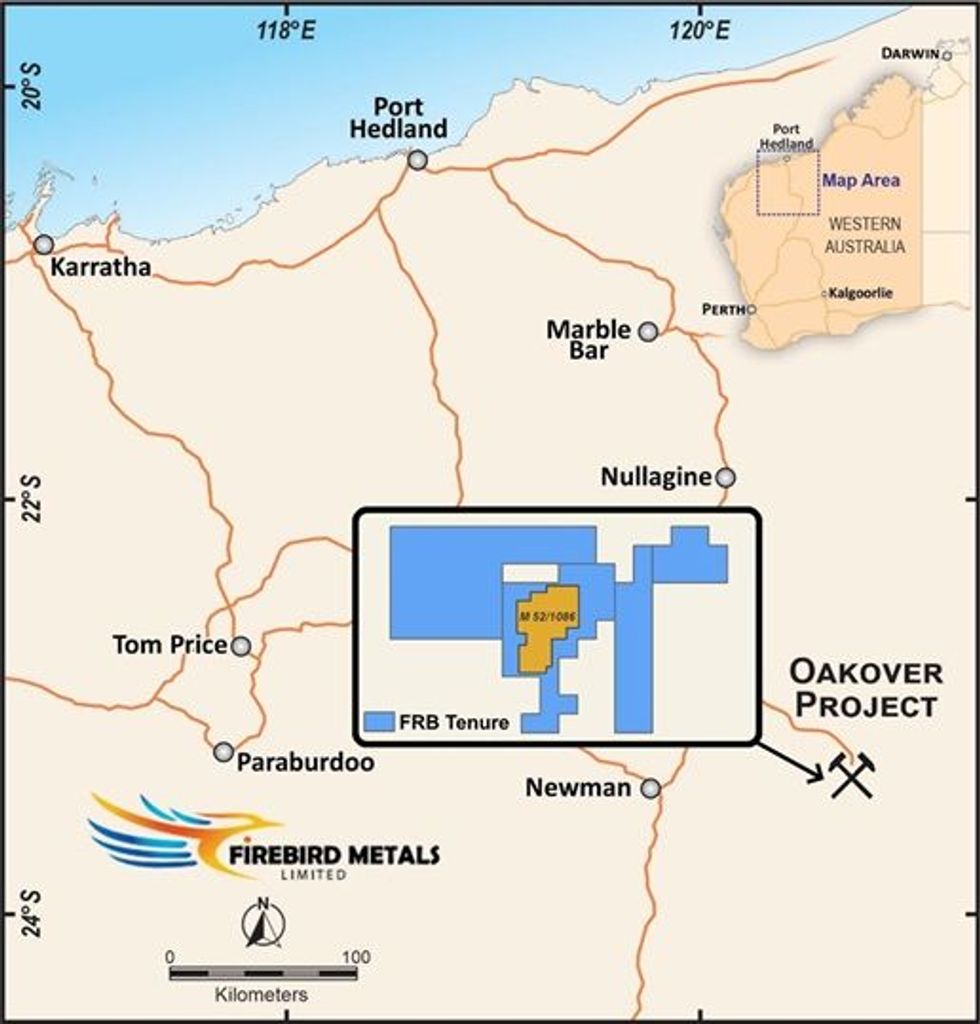

Figure 1: Oakover Project location

Figure 1: Oakover Project location

The granted Mining Lease is conditional on receiving approval from the Department of Energy, Mines, Industry Regulation and Safety (DEMIRS) for a mining proposal.

The Company’s long-term strategy is to grow into low-cost manganese-based cathode material business, leveraging its world-class team, unique processes and technology and its own mineral resources. The Oakover Project boasts a Mineral Resource Estimate1 of 176.7 Mt at 9.9% Mn, with 105.8 Mt at 10.1% Mn in an Indicated category.

Through the execution of this strategy, Firebird aims to secure a natural cost advantage in LMFP cathode production, particularly by integrating manganese sulphate (MnSO₄) from its proposed production plant in China.

Oakover development programs will remain focussed on completing environmental surveys and reports as well as mining studies to feed into the mining proposal.

Click here for the full ASX Release

This article includes content from Firebird Metals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.