The Conversation (0)

Moab Minerals Limited (ASX: MOM) (Moab or the Company) is pleased to provide an update of activities at the Manyoni Uranium Project in Tanzania, Africa.

Highlights:

Moab Managing Director, Mr Malcolm Day, commented: “I visited the Manyoni Uranium Project last week and am excited to report that drilling has started. The Company only settled the transaction on 9th July and in less than two months has been able to ‘hit the ground running’. The drilling program is expected to run over the next few months with most of the assay results available in November/December. I look forward to updating shareholders in coming months in regard the advancement of the Manyoni Uranium Project”.

About the Manyoni Uranium Project

Tanzania Uranium Projects (Moab 94.00%)

On 12 March 2024, the Company announced the acquisition of a package of advanced uranium projects in Tanzania (refer ASX Announcement 12 March 2024) (Acquisition). The Company completed the Acquisition on 9 July 2024.

The Acquisition includes the Manyoni and Octavo Uranium Projects, covering a total of 216 km2. The projects are strategically located just 5km north of Manyoni town, the Manyoni Uranium Project enjoys convenient access to modern railway and sealed highway infrastructure as well as readily available power and water resources.

The Manyoni Uranium Project was previously explored, and extensively drilled, by Uranex Ltd from the early 2000’s until 2013.

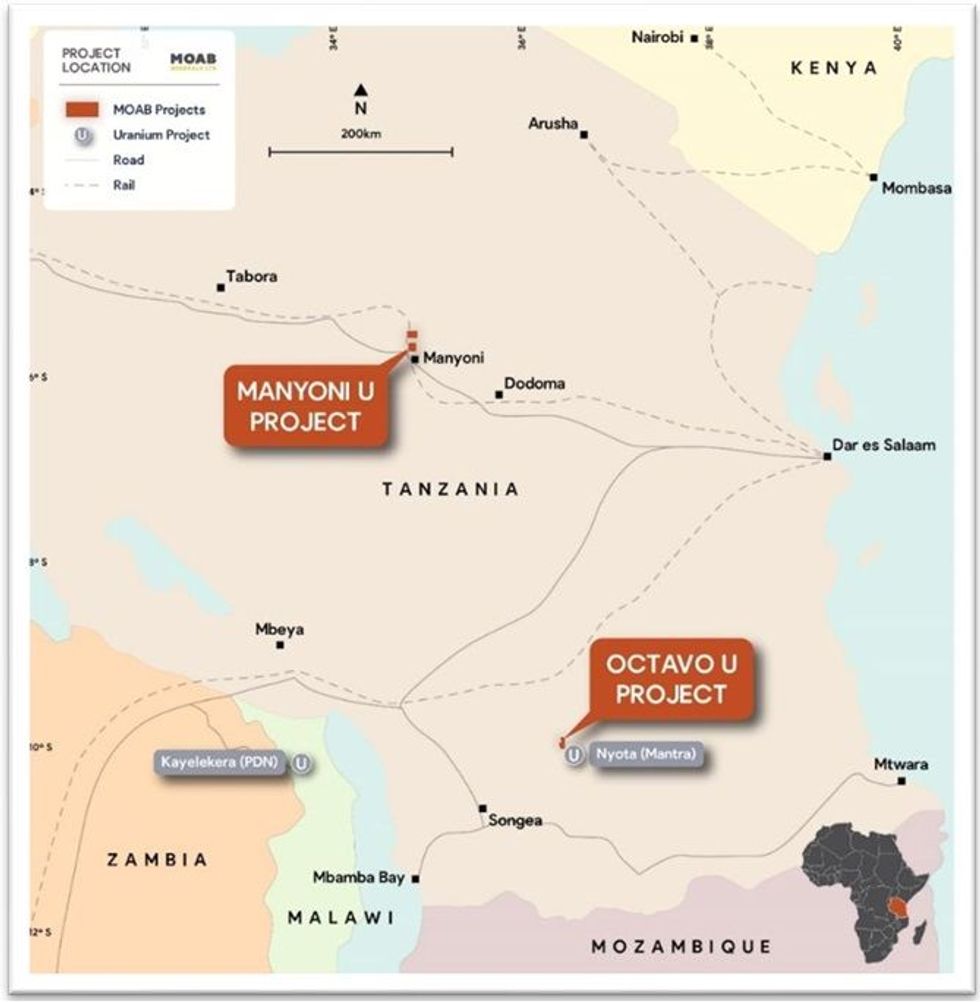

Project Location

The Manyoni Uranium Project tenements are located in the Republic of Tanzania (pop. 65 million), Africa, approximately 100km northwest of the capital city of Dodoma (pop. 765,000). The location of the uranium project at Manyoni is shown in Figure 1 and Figure 2.

Core drilling underway at Manyoni uranium project

Core drilling underway at Manyoni uranium project

Figure 1. Location of the Manyoni Uranium Project

Figure 1. Location of the Manyoni Uranium Project

Figure 2. Location of Manyoni Tenements

Figure 2. Location of Manyoni Tenements

Geological Setting and Uranium Mineralisation

The tenements are located in the central part of the Tanzanian Archaean Shield, which is a stable platform of granite-gneiss terrane with marginal greenstone belts. Radiometrically “hot” granites have been subject to erosion over geological time and have contributed uranium and other metals into the pluvial streams and lakes which drain the shield.

In the Manyoni area the uranium is deposited in a shallow playa lake system as schröckingerite (in the lake sediments) and carnotite in the granitic saprolite below the lake sediments. The mineralisation varies from flat lying to shallowly dipping as it follows the direction of the palaeo- drainage to the south-east while the average depth to the top of mineralisation varies from 3m to 10m.

Validation Drilling (Stage One Drilling)

Moab has completed a substantial review of historic databases that were acquired from the property vendors. Moab has appointed Resource specialists Datamine/Optiro to assist the Company with planning a program of Validation drilling designed to verify historical drill results. A program of 60 drill holes involving PQ Triple Tube core drilling adjacent to old drill holes that contained uranium mineralisation is planned to commence in the 1st Quarter FY2024/2025. The objectives of the program include:

It is estimated that this initial program will be completed in 2nd Quarter FY2024/2025. On completion of the Validation drilling program the information will be used to update the wire-frame model for mineralized domains thereby facilitating resource estimation, depending on results.

Exploration Drilling (Stage Two Drilling)

In addition to the above drilling, Moab is planning to undertake an exploration drilling program that is designed to locate extensions to the known mineralisation at Manyoni. This will be based on grid drilling on a 400m x 400m and 200m x 200m pattern around the known mineralisation. The Manyoni uranium mineralisation is at shallow depth, varying from 3m to 15m to the top of mineralisation, and flat lying. Moab has executed a drilling contract for a minimum of 1500m of PQTT core drilling covering Stages one and two drilling, with the option to drill an additional 1500m.

Click here for the full ASX Release

This article includes content from MOAB Minerals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.