Cygnus Metals Limited (ASX:CY5) is pleased to announce highly promising results from a desktop study on its Auclair project in Canada’s lithium-rich James Bay region.

Highlights

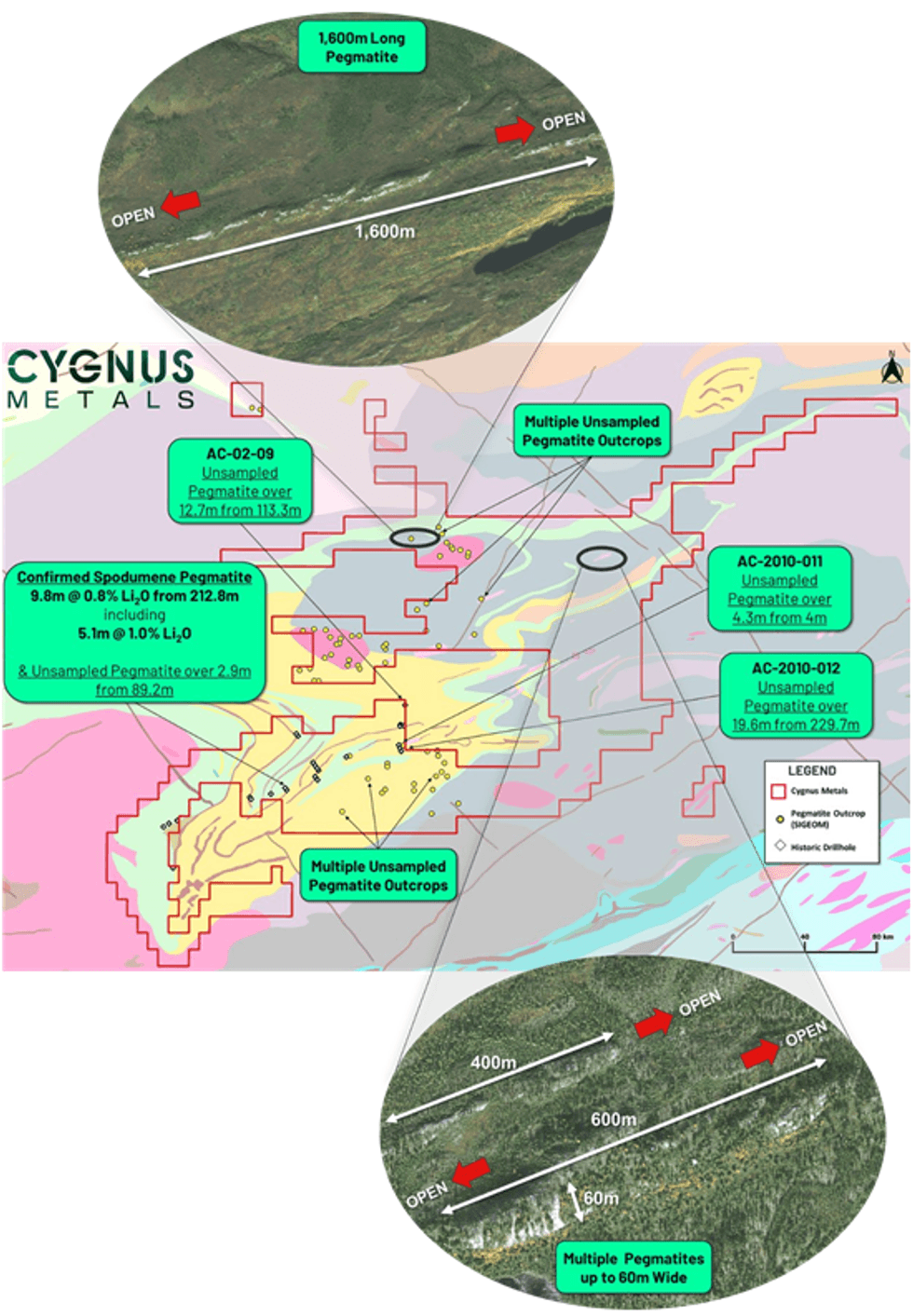

- Initial desktop studies have already identified 67 pegmatites which have never been sampled for lithium and a further 14 pegmatite intervals across five historic drill holes which have never been assayed

- Identified pegmatites measure up to 1.6km in strike and 60m in width (Figure 1)

- Partial assays* received from sampling of historic drill hole AC-2010-004 returned:

- 9.8m @ 0.8% Li2O from 212.8m, including 5.1m @ 1.0% Li2O and 1m @ 1.2% Li2O

(*Assays are partial as the full pegmatite interval could not be recovered due to winter conditions)

- Cygnus has an exceptional first mover opportunity to conduct the first ever lithium exploration at Auclair, with mineralisation in drill hole AC-2010-004 completely open and never followed up

- Exploration is about to commence with geophysics (including LiDAR), mapping and rock chip sampling in June. Diamond drilling is scheduled to commence in July to follow up the spodumene-bearing pegmatites in hole AC-2010-004

- Through strategic acquisition, Cygnus has already increased its ground position at Auclair to a belt scale 337km2

- The project boasts excellent infrastructure with year-round road access and high-voltage transmission lines running through the project as well as being located within 80km of the Nemiscau AirportThe project is located in the same greenstone belt and just 60km due east of Critical Elements Resource Corp’s Rose Deposit (34.2Mt @ 0.9% Li2O), and just 50km northeast of Whabouchi (55.7Mt @ 1.4% Li2O), which is owned and operated by Nemaska Lithium1

Cygnus Managing Director David Southam said: “These results highlight Auclair's immense potential. To have so many pegmatites and known spodumene in an area never explored for lithium is a remarkable start and puts Cygnus in a prime position to make a discovery in the region. Given what we already know about Auclair, we are wasting no time ramping up exploration, with drilling scheduled to start in July.”

The study identified 67 pegmatites which require immediate follow-up. Cygnus has also received assays which confirm previously reported visuals of spodumene mineralisation from sampling of historic gold exploration core at Auclair (refer ASX release dated 28 February 2023).

Figure 1: Unsampled pegmatites across the Auclair Project both in drilling and outcrop. – Background regional geology interpretation from SIGEOM.

Figure 1: Unsampled pegmatites across the Auclair Project both in drilling and outcrop. – Background regional geology interpretation from SIGEOM.

Auclair is a recent addition to the Cygnus lithium project portfolio in James Bay and was acquired due to its immense potential to host significant spodumene-bearing lithium pegmatites. The Company has since grown the project to 337km2 through two separate acquisitions and now has a dominant land position across the highly prospective Eastmain greenstone belt (EGB).

Click here for the full ASX Release

This article includes content from Cygnus Metals, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.

Figure 1: Unsampled pegmatites across the Auclair Project both in drilling and outcrop. – Background regional geology interpretation from SIGEOM.

Figure 1: Unsampled pegmatites across the Auclair Project both in drilling and outcrop. – Background regional geology interpretation from SIGEOM.