The Conversation (0)

Elixir Energy Limited (“Elixir” or the “Company”) is pleased to announce a material increase in the contingent resources booking for its 100% owned ATP 2044 in Queensland (Project Grandis).

HIGHLIGHTS

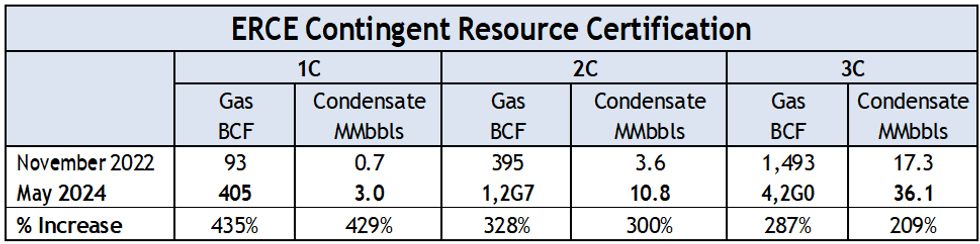

The updated estimate of contingent resources in ATP 2044 is as set out in the table below. The subclass of Contingent Resources (as defined under the PRMS – illustrated in Appendix 1) is “Development Unclarified”.

These estimates have been independently certified by international firm ERC Equipoise (“ERCE”).

Notes:

These are unrisked contingent resources that have not been risked for the chance of development and there is no certainty that it will be economically viable to produce any portion of the contingent resources.

These contingent resources are classified as “Development Unclarified”.

Detailed notes on the background to the preparation of the contingent resources report are set out in Appendix 1.

These contingent resources estimates are for the sandstones only in the gas bearing Permian section, and do not include the prospective coal resources, which will be the subject of stimulation and production testing in the coming months.

This upgrade in contingent resources is largely due to:

1. The lowering of the Lowest Known Gas (LKG) from Daydream-1 to Daydream-2 as a result of the successful Lorelle sandstone testing; and

2. The overall improved sandstone reservoir development and resulting increasing net to gross from Daydream-1 to Daydream-2.

Elixir’s technical team and ERCE analyzed drilling, logging and test data to make these estimates. Specific analysis including seismic interpretation, core analysis, wireline petrophysics, chromatographic gas analysis, DFITs, production test analysis and gas sampling have all been incorporated in the resources estimates. The key contingency for Project Grandis is the flowrate. Whilst the Company has achieved a flowrate of 1.3 million cubic feet per day from the lower-most Lorelle Sandstone, the upper zones have not yet been tested.

The Daydream-2 appraisal program is expected to resume in the next month or so. Further updates on more specific time-frames are expected to follow shortly, as current negotiations with various sub- contractors are finalized.

Elixir’s Managing Director, Mr Neil Young, said: “We are naturally delighted with the ongoing material build-up of the very significant contingent resources in our exceptionally well located Project Grandis project. As our appraisal program resumes in the next month or so, the success case should deliver yet more substantial increases.”

Click here for the full ASX Release

This article includes content from Elixir Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.