The Conversation (0)

CuFe Ltd (ASX: CUF) (CuFe or the Company) is pleased to provide an update on the status of CuFe’s Tennant Creek Cu-Au project, which is owned 55% by CuFe and 45% by Gecko Mining Company Pty Ltd. The project has an existing JORC 2012 resource of 7.3MT at 1.7% Copper and 0.6g/t Gold (refer to CuFe’s ASX release dated 3 April 2023).

HIGHLIGHTS

Technical Review and Scope

A detailed technical review of the Tenant Creek geology, historical data sets and exploration targets has been undertaken by Mr John Dobe as a technical consultant to CuFe. Mr Dobe is a geologist with >30 years of global exploration experience (predominantly Homestake/Barrick) specialising in project generation and project evaluations at all stages of exploration, from grassroots through to brownfields. John has a detailed understanding of mineral deposits with particular focus on porphyry Cu-Au, IOCG, epithermal Au, orogenic Au, Sediment-hosted Cu, SEDEX, and VHMS deposits.

The scope of the review included auditing and consolidation of historical drill hole geological and geophysical databases, exploration target review, generation and ranking. The outcomes of the review have helped derive an exploration strategy with the aim of growing the global resources at the CuFe Tennant Creek Project.

Review Findings and Target Ranking

The Gecko and Orlando Corridors are well explored and current resources are mostly well defined with multiple generations of surface and underground drilling including RAB, vacuum, RC and Diamond. The sharp and well-defined nature of the mineralisation does provide further opportunities for additional resources extensions immediately adjacent to the known deposits. Geophysical data is also abundant and wide ranging including IP, Helitem, magnetics, gravity and seismic.

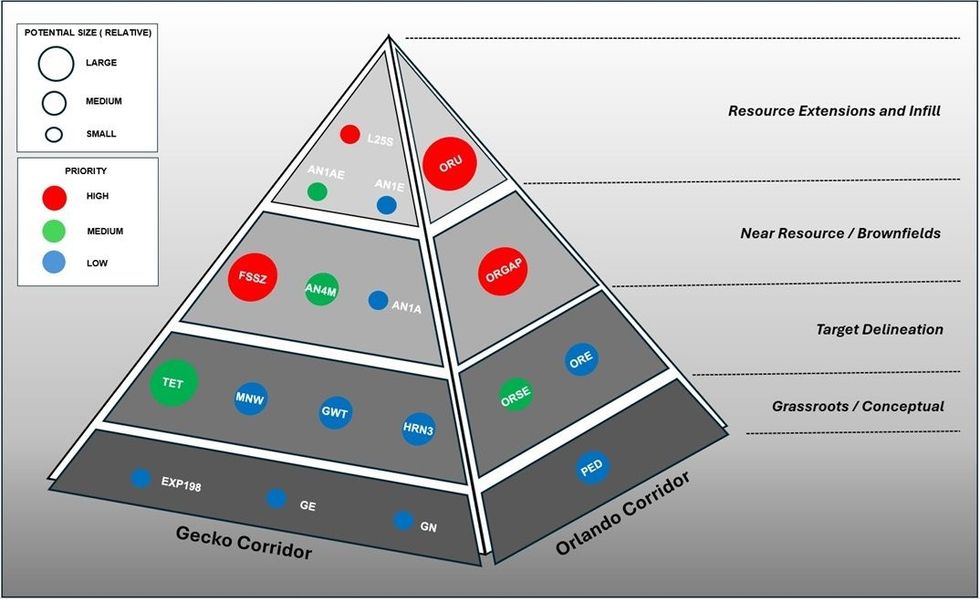

Exploration targets in aim of growing the global resource have been identified within the Orlando and Gecko Corridor and have been allocated the following categories:

1. Resource extensions and infill

2. Near Resource / brownfields

3. Target Delineation

4. Grassroots / Generative

Resource extensions and infill targets have a higher degree of certainty and potential than those that are grassroots generative and conceptual in nature.

Targets have also been ranked by priority on the basis of their complexity, exploration maturity and prospectivity. Their relative potential size has been estimated based on technical review/analysis and conceptual models and projections (See Figure 1).

Figure 1: Targets defined during the technical review within the Gecko and Orlando corridors.

Figure 1: Targets defined during the technical review within the Gecko and Orlando corridors.

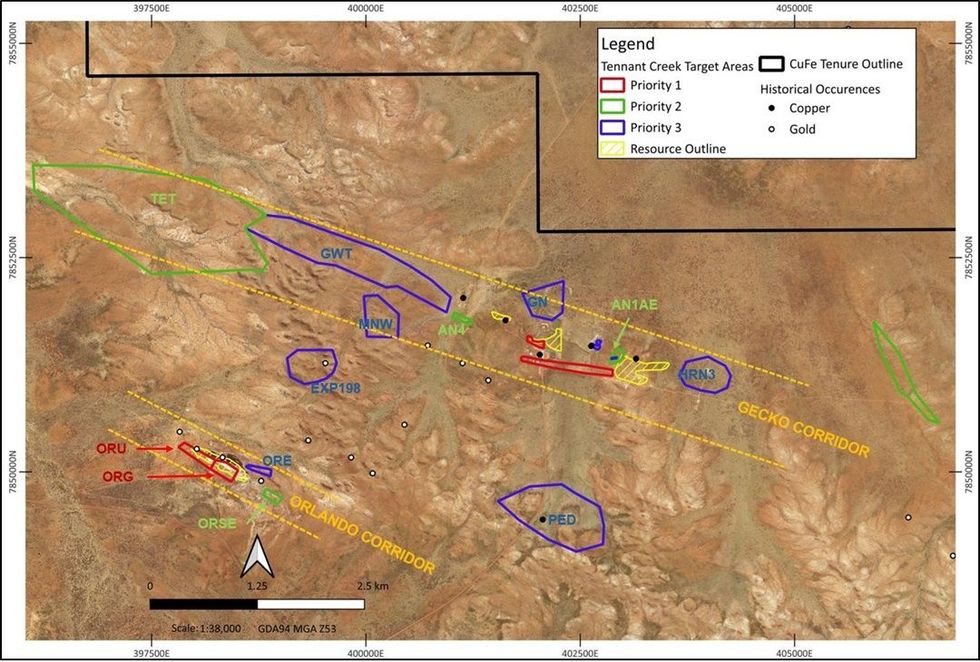

Four high priority targets have fallen out of the technical review that are located with both the Gecko and Orlando corridors. Spatially the targets are shown in Figure 2.

Figure 2: Location of the targets and the Orlando and Gecko Corridors

Figure 2: Location of the targets and the Orlando and Gecko Corridors

Orlando Corridor

Five targets have been identified within the Orlando Corridor, two of which are high priority, potentially adding to resources by extension and near resources / brownfields discoveries. Orlando underground resource extension includes the interpretation and modelling of the Orlando underground resources that are not included within the current Orlando Resource.

Recently MEC consulting was engaged by CuFe to review the Orlando Resources and historical drilling data. The review confirmed that there is drill hole data that supports extensions of copper and gold mineralisation from the existing open pit, into and around the historical underground workings. Currently this mineralisation is not interpreted and or reported in the existing 2023 Orlando Resource (See Figure 3 and refer to CuFe ASX announcement 3 April 2023). An immediate workstream has been initiated to develop a global resource for the Orlando deposit based on an updated validated drill hole data base including recently sourced Grade Control drilling from the Open Pit mining and historic drilling where QA/QC can be achieved. This target ranks high in terms of priority based on the short lead time with no drilling required and minimal execution costs. It also has the potential to grow the underground resource at Orlando with reasonable confidence considering the drill intercepts are confirmed and historical underground mining has recovered cooper and gold from these levels.

The second high priority target within the Orlando Corridor is an area immediately below the open pit and adjacent to the underground where there is a gap in drill coverage that leaves a portion of the resource open along strike and at depth (See Figure 3). Testing this gap will require deep drilling in the order of 350m but the potential scale of this target justifies its high ranking and priority.

Click here for the full ASX Release

This article includes content from CUFE LTD, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.