The Conversation (0)

Highlights

Olympio’s Managing Director, Sean Delaney, commented:

“Acquiring the advanced Bousquet Gold Project presents a significant opportunity for Olympio to expand our exposure to one of the world’s premier gold-bearing structures—the renowned Cadillac Break. The project is strategically positioned between substantial gold deposits to the east and west, with numerous high-grade gold prospects featuring gold both at surface and in drilling. This makes Bousquet an exceptional exploration target. The geological setting and mineralisation style closely resemble the nearby million-ounce O’Brien Project, where high-grade gold zones are often associated with visible gold in quartz veining.

“The Project is next to working gold mines with under-utilised mills (<20km by road), with a major highway, railway and hydroelectric power all traversing the centre of the project.

Bullion are divesting Bousquet to focus on their large Bodo polymetallic project which provides Olympio with this great opportunity to explore in one of the world’s best gold regions.”

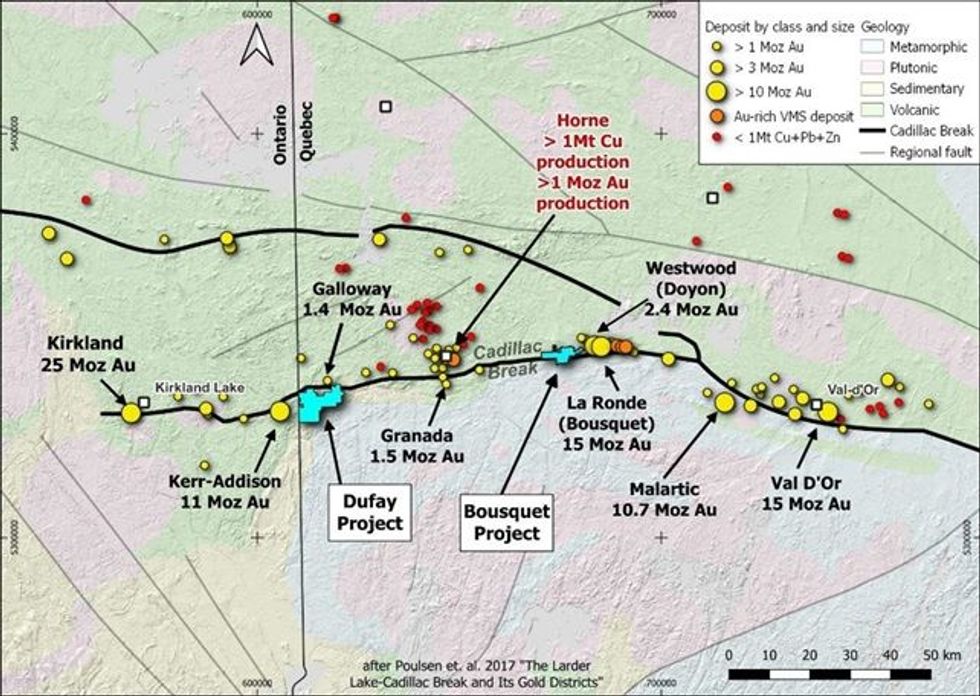

Figure 1 Setting of Olympio projects, Bousquet and Dufay, on the Cadillac Break

Figure 1 Setting of Olympio projects, Bousquet and Dufay, on the Cadillac Break

The Bousquet Gold Project is a strategic land acquisition which complements the Dufay Gold-Copper Project 60km to the west along the renowned Cadillac Break. The southern half of the project covers a well-defined, regionally mineralised zone to the south of the Cadillac Break, which hosts numerous gold prospects within Timiskaming Group sediments that are exclusively correlated with the development of the Cadillac Break.

The Bousquet Project includes several advanced gold prospects and numerous structural and geophysical targets that remain untested by drilling or modern exploration. The majority of drilling on the project is pre-1947, and all prospects remain under-explored.

HIGH GRADE QUARTZ VEINS IN FAVOURABLE GEOLOGICAL CONTEXT

Gold mineralisation at Bousquet is structurally controlled, quartz vein-hosted, high-grade gold associated with second and third order structures peripheral to the Cadillac Break, which is typical of the majority of mineralisation on the Cadillac Break1.

Click here for the full ASX Release

This article includes content from Olympio Metals Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.