The Conversation (0)

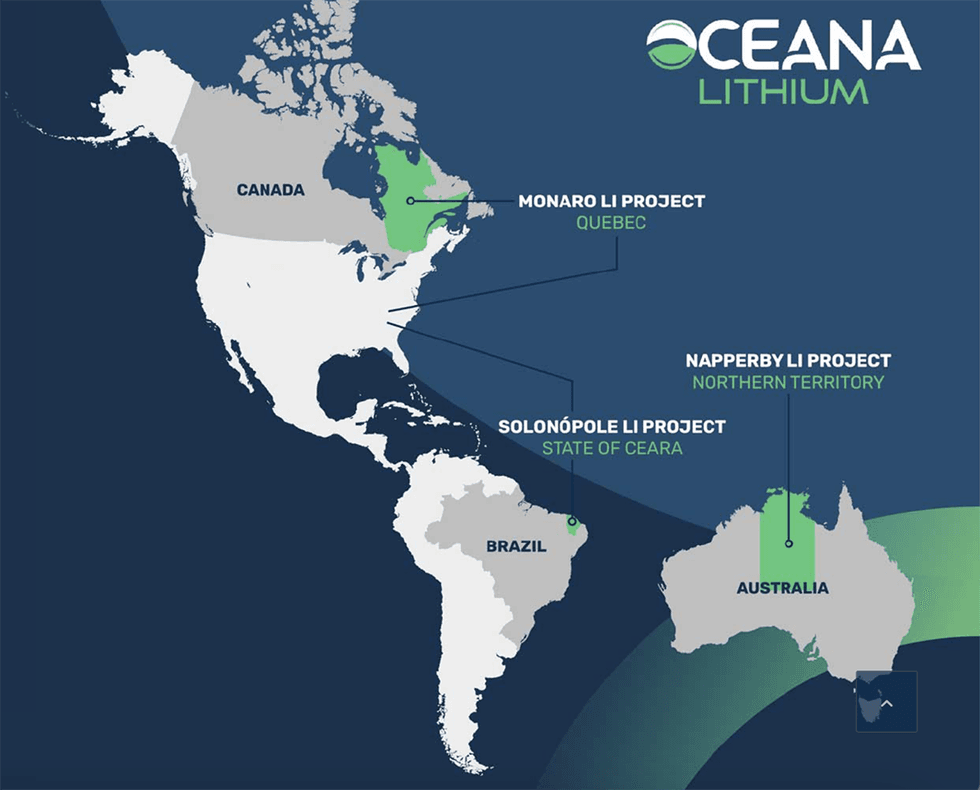

Oceana Lithium (ASX:OCN) is well-positioned to explore three strategic and highly prospective lithium projects in Australia, Canada and Brazil — all tier-one mining jurisdictions. Oceana Lithium is an early-stage exploration company with flagship Solonópole project displaying considerable promise.

The company's well-informed exploration strategy stems from veteran geologists and mining professionals with decades of experience between them. It's already identified multiple exploration targets across all three projects, all of which are highly prospective and known to contain lithium.

Oceana's Solonópole project consists of eight permits covering 114 square kilometers of highly prospective ground. Detailed field mapping by Oceana's Brazilian subsidiary Ceara Litio has identified a significant mineralized pegmatite corridor within the company's claim. The permits also cover several historic artisanal mining sites previously tapped for lithium, tantalum, niobium and tin.

This Oceana Lithium profile is part of a paid investor education campaign.*

Click here to connect with Oceana Lithium (ASX:OCN) to receive an Investor Presentation