The Conversation (0)

Miramar Resources Limited (ASX:M2R, “Miramar” or “the Company”) advises that it has identified multiple very large uranium targets within the Company’s 100%-owned Bangemall Projects, in the Gascoyne region of Western Australia.

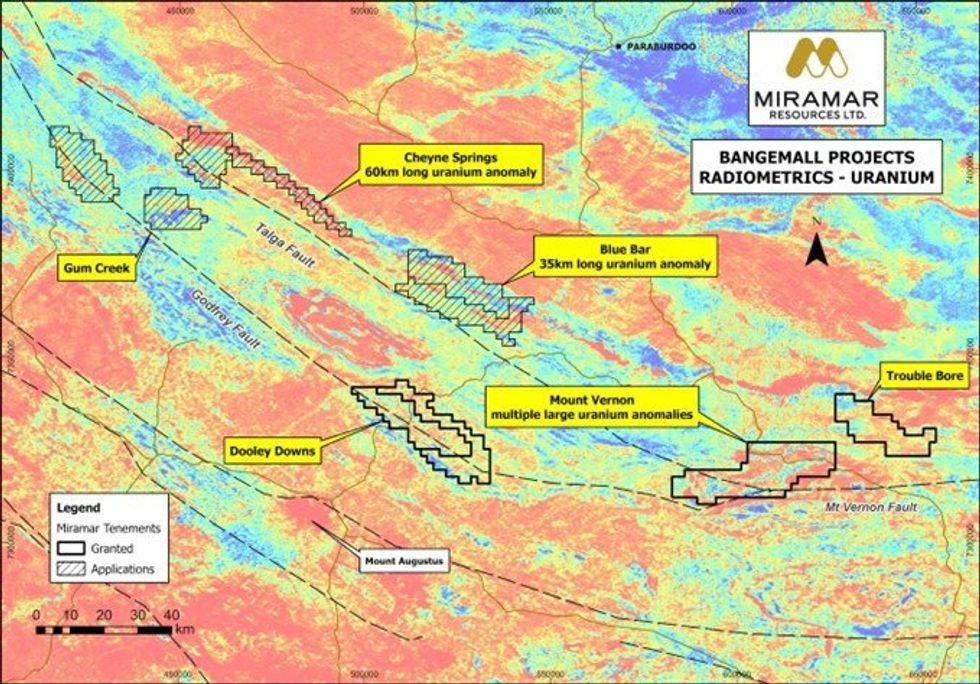

Regional radiometric data shows multiple very large and high-amplitude uranium anomalies that stretch over at least 100km of strike and across several of Miramar’s tenements (Figure 1).

Miramar’s Executive Chairman, Mr Allan Kelly, said the Company’s strategic Bangemall landholding has potential for multiple commodities and deposit types.

“Proterozoic orogens throughout Australia and worldwide host many large base and precious metal deposits, and we believe the Capricorn Orogen should be no exception,” Mr Kelly said.

“Whilst our current focus is on exploring for Norilsk-style nickel, copper and platinum group elements at our Mount Vernon and Trouble Bore Projects, we have a very long list of attractive exploration targets we aim to systematically explore,” he added.

Figure 1. Regional uranium radiometric image for Bangemall Project tenements.

Figure 1. Regional uranium radiometric image for Bangemall Project tenements.

Cheyne Springs Target

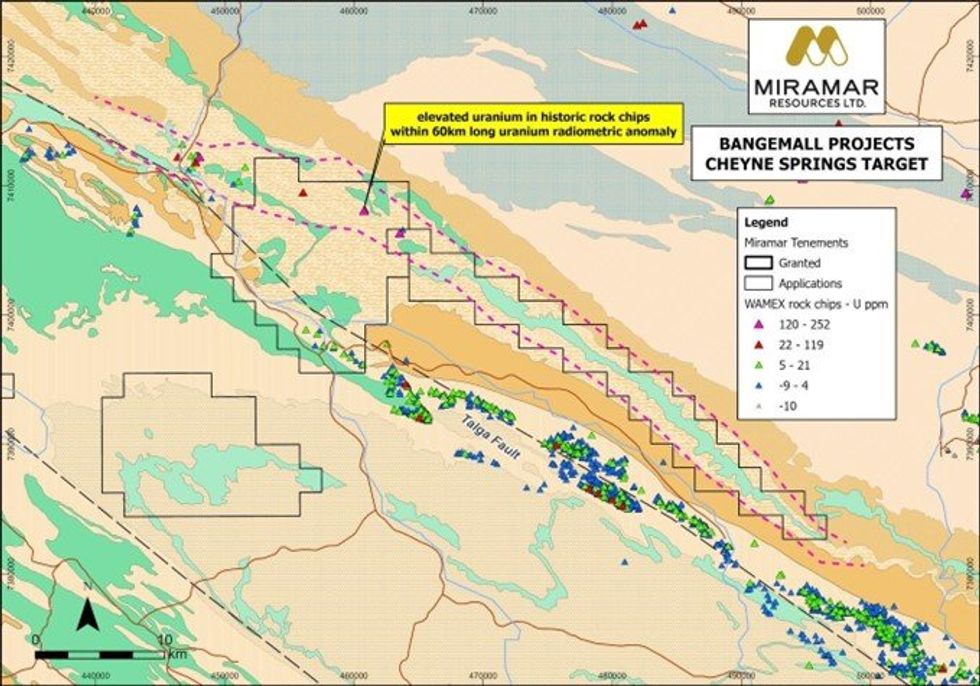

A well-defined, 60-kilometre-long uranium anomaly is located within the Cheyne Springs Target towards the northern edge of the Edmund Basin, at the contact with the older Ashburton Basin rocks (Figure 2).

The very large radiometric anomaly has been virtually unexplored except for a few wide-spaced rock chip samples that returned results up to 246ppm U (i.e. 290ppm U3O8) (WAMEX Reports a78053, a81036, a91967 and a92435) (Figure 3).

The Company is working towards grant of the tenement applications at Cheyne Springs, and the adjacent Blue Bar Target.

Figure 2. Cheyne Springs tenement applications showing uranium in limited historic rock chip results in relation to the 60-kilometer-long regional uranium radiometric anomaly (pink dashed line).

Figure 2. Cheyne Springs tenement applications showing uranium in limited historic rock chip results in relation to the 60-kilometer-long regional uranium radiometric anomaly (pink dashed line).

Click here for the full ASX Release

This article includes content from Miramar Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.