The Conversation (0)

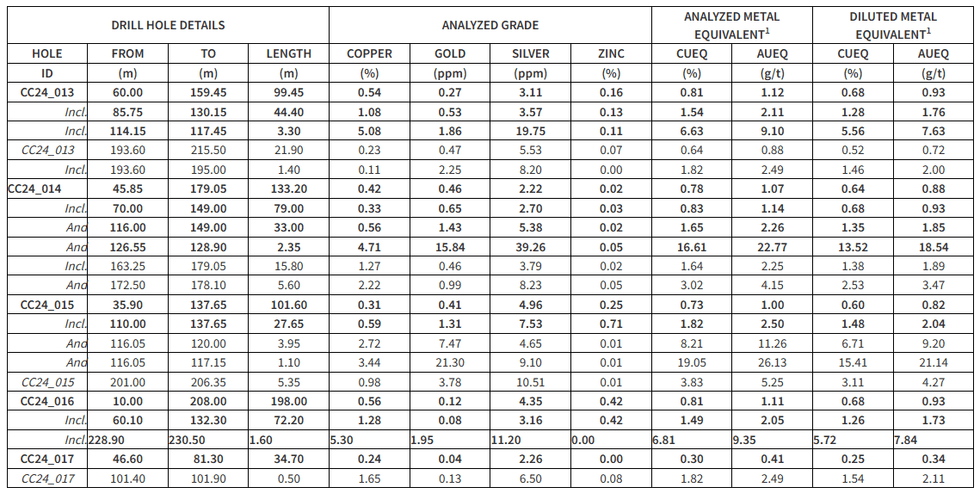

Intrepid Metals Corp. (TSXV: INTR) (OTCQB: IMTCF) ("Intrepid" or the "Company") provides results for 5 additional diamond drill holes from the Company's Corral Copper Property ("Corral Copper" or the "Property") located in Cochise County, Arizona. All 5 holes were drilled in the Ringo Zone which is located along the southern margin of a 3-kilometer-long trend of near surface carbonate replacement ("CRD") and related supergene enrichment oxide copper-gold-silver-zinc mineralization. Highlights from these 5 holes are shown in Table 1.

Additional highlights include:

"The Corral Copper Project has once again returned remarkable shallow copper grades and mineralized intercepts at the Ringo Zone," stated Ken Brophy, Chief Execuitve Officer. "The drilling at Ringo is illustrating the Project's gold endowment with broad intercepts of highly continuous, locally high-grade gold mineralization, including 21.3 gpt Au over 1.1m in hole CC24_15 and 15.84 gpt Au over 4.71m in hole CC24_14, which we expect will make a significant contribution to the economic potential of the project."

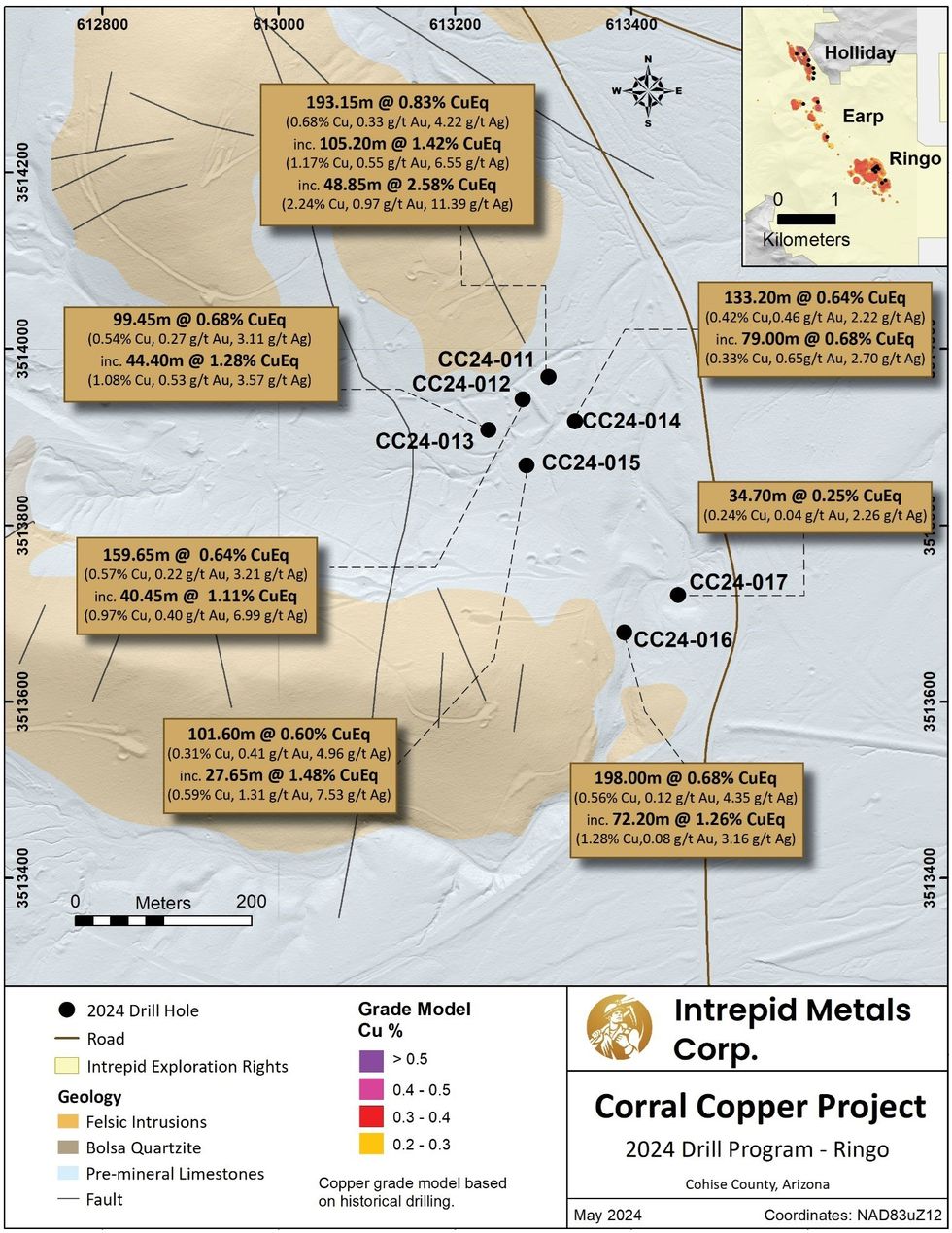

The Ringo Zone is located at the southern end of a 3-kilometer-long string of copper-gold-silver-zinc bearing carbonate replacement bodies (Figure 1). The Ringo Zone measures approximately 900m (northwest to southeast) by 800m (southwest to northeast) and contains favorable Abrigo Limestone (and Bolsa Formation), pre-mineral intrusions, alteration and copper-gold-silver-zinc replacement style mineralization and secondary enriched copper oxide zones that are locally high-grade. To date, Intrepid has completed 9 holes in the Ringo Zone for a total of 2105m. Highlights from holes CC24-013 through CC24-017 are included in Table 1 below and full results are within Table 2. Hole CC24_16 was prematurely shut down due to drill rods breaking down hole and ended in robust mineralization.

Table 1. Highlight composite drill intercepts for the Ringo Zone1

The Corral Copper 2024 Drill Campaign

Intrepid has completed 20 diamond drill holes (~3,900m) as part of a planned 5,000m program within its private lands at Corral Copper. Intrepid is drill testing a 3.5 by 1.5 km copper-gold-silver-zinc mineralized footprint to demonstrate its potential to host economic CRD, skarn, and related porphyry copper mineralization.

Precious and base metal mineralization at Corral Copper is concentrated in structurally controlled northeast dipping siliciclastic and carbonate sedimentary rocks including (oldest to youngest) Cambrian Bolsa Quartzite, upper-Cambrian Abrigo Limestone, Devonian Martín limestone and Mississippian Escabrosa limestone (Figure 1). The most intense mineralization occurs in the Abrigo Limestone (main host) and Bolsa Quartzite, which are intruded locally by a series of Jurassic (and possibly younger) mineralized intrusions including the Star Hill, Copper Bell and Sniveler porphyries, quartz latite sills, and cross-cutting mineralized breccia bodies.

The Corral Copper Property includes the Holliday, Earp and Ringo zones (northwest to southeast, which are related zones of discontinuously outcropping, locally high grade CRD and skarn related mineralization and associated supergene enrichment mineralization that are interpreted to have formed in the distal porphyry copper geological environment). Please refer to footnotes for details regarding assumptions for metal equivalent calculations and true widths.

Figure 1. Geological map showing diamond drill hole locations for the 2024 Drill Program2

Figure 1. Geological map showing diamond drill hole locations for the 2024 Drill Program2

Figure 1 includes historical data marked as such by the legend. Please refer to footnotes for additional details.

Table 2. Composite drill intercepts for Corral Copper Project Holes CC24-013 to CC24-0171

Table 3. Drill hole location information for holes CC24-013-CC24-0171

Technical Information

All scientific and technical information in this news release has been prepared by, or approved by Daniel MacNeil, P.Geo. Mr. MacNeil is a Technical Advisor to the Company and is a qualified person for the purposes of National Instrument 43-101 - Standards of Disclosure for Mineral Projects.

Mr. MacNeil has verified the drilling data disclosed in this news release, including the assay and test data underlying the information or opinions contained in this news release. Mr. MacNeil verified the data disclosed (or underlying the information disclosed) in this news release by reviewing imported and sorted assay data; checking the performance of blank samples and certified reference materials; reviewing the variance in field duplicate results; and reviewing grade calculation formulas. Mr. MacNeil detected no significant QA/QC issues during review of the data and is not aware of any sampling, recovery or other factors that could materially affect the accuracy or reliability of the drilling data referred to in this news release.

However, some of the data disclosed in this news release is related to historical drilling results which have been identified as such. Intrepid Metals and Mr. MacNeil have not undertaken any independent investigation of the sampling nor have they independently analyzed the results of the historical exploration work in order to verify the results. Intrepid and Mr. MacNeil considers these historical drill results relevant as the Company is using this data as a guide to plan exploration programs. The Company's current and future exploration work includes verification of the historical data through drilling.

Quality Assurance and Quality Control

Drill core was first reviewed by a geologist, who identified and marked intervals for sampling. The marked sample intervals were then cut in half with a diamond saw; half of the core was left in the core box and the other half was removed, placed in plastic bags, sealed and labeled. Intervals and unique sample numbers are recorded on the drill logs and the samples are sequenced with standards and blanks inserted according to a predefined QA/QC procedure. The samples are maintained under security on site until they are shipped to the analytical lab.

All core samples were sent to ALS Geochemistry (ALS), a division of ALS Global, in Tucson, Arizona, for sample preparation, with pulps sent to the ALS Geochemistry laboratory in Reno, Nevada for analysis. ALS meets all requirements of International Standards ISO/IEC 17025:2017 and ISO 9001:2015 for analytical procedures and is independent of the Company. HQ size core was split and sampled over approximately two metre intervals. Samples were analyzed using: ALS's Fire Assay Fusion method (Au-AA23) with an AA finish for gold and by gravimetric finish (Au-GRA21) for samples assaying greater than 10 ppm (g/t) gold; by a 36-element four acid digest ICP-AES analysis (ME-ICP61) with additional analysis for Ore Grade Cu (Cu-OG62), Ore Grade Zn (Zn-OG62) and Ore Grade Pb (Pb-OG62); and for silver assays above 100 ppm (g/t) by Fire Assay Fusion method with gravimetric finish (Ag-GRA21). ME-ICP61 results were reported in parts per million (ppm), Ore Grade (OG62) results were reported in percent (%). In addition to ALS quality assurance- quality control (QA/QC) protocols, Intrepid implements an internal QA/QC program that includes the insertion of sample blanks, duplicates, and standards, with QA QC control samples comprising approximately 10% of the sample stream.

About Corral Copper

The Corral Copper Property is a district scale advanced exploration and development opportunity in Cochise County, Arizona. Corral Copper is located 15 miles east of the famous mining town of Tombstone and 22 miles north of the historical Bisbee mining camp which has produced more than 8 billion pounds of copper3. Production from the Bisbee mining camp, or within the district as disclosed in the next paragraph, is not necessarily indicative of the mineral potential at Corral.

The district has a mining history dating back to the late 1800s, with several small mines extracting copper from the area in the early 1900s, producing several thousand tons. Between 1950 and 2008, various companies explored parts of the district, but the effort was uncoordinated, non-synergistic and focused on discrete land positions and commodities due to the fragmented ownership. Intrepid has been able to secure data from various sources which provides a solid foundation in creating geological interpretations and identifying new target areas.

The Corral Copper Property is comprised of the Excelsior Property, the CCCI Properties, the Sara Claim Group and the MAN Property. The Company has completed the acquisition of the Excelsior Property and Sara Claim Group through purchase and sale agreements. The Company has the right to acquire the corporate group that holds the CCCI Properties through an option agreement. The Company has the right to acquire the MAN Property through an option agreement. See the "Commitments" section of the Company's most recently filed Management Discussion and Analysis for further details.

Intrepid is confident that by combining modern exploration techniques with historical data and with a clear focus on responsible development, the Corral Copper Property can quickly become an advanced exploration stage project and move towards development studies.

About Intrepid Metals Corp.

Intrepid Metals Corp. is a Canadian company focused on exploring for high-grade essential metals such as copper, silver, lead, and zinc mineral projects in proximity to established mining jurisdictions in southeastern Arizona, USA. The Company has acquired or has agreements to acquire several drill ready projects, including the Corral Copper Project (a district scale advanced exploration and development opportunity with significant shallow historical drill results), the Tombstone South Project (within the historical Tombstone mining district with geological similarities to the Taylor Deposit, which was purchased for $1.3B in 20184, though mineralization at the Taylor Deposit is not necessarily indicative of the mineral potential at the Tombstone South Project) both of which are located in Cochise County, Arizona and the Mesa Well Project (located in the Laramide Copper Porphyry Belt in Arizona). Intrepid has assembled an exceptional team with considerable experience with exploration, developing, and permitting new projects within North America. Intrepid is traded on the TSX Venture Exchange (TSXV) under the symbol "INTR" and on the OTCQB Venture Market under the symbol "IMTCF". For more information, visit www.intrepidmetals.com.

INTREPID METALS CORP.

On behalf of the Company

"Ken Brophy"

CEO

For further information regarding this news release, please contact:

Ken Brophy, CEO

604-681-8030

info@intrepidmetals.com

Notes

Cautionary Note Regarding Forward-Looking Information

Certain statements contained in this release constitute forward-looking information within the meaning of applicable Canadian securities laws. Such forward-looking statements relate to: economic potential of the Property; confirmation of historical results; expansion of Holliday, Earp and Ringo zones; disclosure of additional drill results; the Project's gold endowment; the significant contribution to the economic potential of the project; the potential of the Property to host an economic CRD, skarn and related porphyry copper mineralization; future exploration plans and drilling plans including the estimated number of drill holes, meterage and expected completion date; the Company's confidence in the drill program; details about potential mineralization; the exploration potential of the Corral Copper Property and the Company's other mineral projects; and potential future production.

In certain cases, forward-looking information can be identified by the use of words such as "plans", "expects", "budget", "scheduled", "estimates", "forecasts", "intends", "anticipates" or "believes", or variations of such words and phrases or state that certain actions, events or results "may", "could", "would", "might", "occur" or "be achieved" suggesting future outcomes, or other expectations, beliefs, plans, objectives, assumptions, intentions or statements about future events or performance. Forward-looking information contained in this news release is based on certain factors and assumptions regarding, among other things, the Company can raise additional financing to continue operations; the results of exploration activities, commodity prices, the timing and amount of future exploration and development expenditures, the availability of labour and materials, receipt of and compliance with necessary regulatory approvals and permits, the estimation of insurance coverage, and assumptions with respect to currency fluctuations, environmental risks, title disputes or claims, and other similar matters. While the Company considers these assumptions to be reasonable based on information currently available to it, they may prove to be incorrect.

Forward looking information involves known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward-looking information. Such factors include risks inherent in the exploration and development of mineral deposits, including risks relating to the ability to access infrastructure, risks relating to the failure to access financing, risks relating to changes in commodity prices, risk related to unanticipated geological or structural formations and characteristics risks related to current global financial conditions, risks related to current global financial conditions and the impact of COVID-19 on the Company's business, reliance on key personnel, operational risks inherent in the conduct of exploration and development activities, including the risk of accidents, labour disputes and cave-ins, regulatory risks including the risk that permits may not be obtained in a timely fashion or at all, financing, capitalization and liquidity risks, risks related to disputes concerning property titles and interests, environmental risks and the additional risks identified in the "Risk Factors" section of the Company's reports and filings with applicable Canadian securities regulators.

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Accordingly, readers should not place undue reliance on forward-looking information. The forward-looking information is made as of the date of this news release. Except as required by applicable securities laws, the Company does not undertake any obligation to publicly update or revise any forward-looking information.

Neither the TSX Venture Exchange nor its Regulation Services Provider (as that term is defined in the policies of the TSX Venture Exchange) has reviewed or accepts responsibility for the adequacy or accuracy of this release.