The Conversation (0)

American Rare Earths (ASX: ARR | OTCQX: ARRNF and AMRRY) (“ARR” or the “Company”) is pleased to announce the results of its Updated Halleck Creek Scoping Study, confirming the project’s strong economics, scalability, and strategic importance.

Compiled by independent engineering firm Stantec Consulting Services Inc., the Study highlights Halleck Creek’s strong economic potential, strategic advantages, and clear pathway to development as a U.S.-based rare earths project. Located in Wyoming, a Tier 1 mining jurisdiction, Halleck Creek benefits from state land tenure, allowing for accelerated permitting and development.

Compelling Economics & Scalable Growth

The Updated Scoping Study confirms Halleck Creek as a world-class rare earths project with robust financials and long-term scalability:

First-Mover Advantage & U.S. Supply Chain Security

As the only large-scale rare earths project in the U.S. with a clear path to production, ARR is positioned to secure a domestic, tariff-free supply of critical minerals for U.S. and allied markets.

Clear Development Pathway & Future Growth

Halleck Creek’s staged development approach ensures financial and operational flexibility, allowing ARR to scale production in alignment with market demand:

CEO Commentary

Chris Gibbs, CEO of American Rare Earths, commented:

"The Updated Scoping Study reinforces Halleck Creek strong economic potential, strategic permitting advantage and clear pathway to development. With a large-scale resource and favourable economics, we are uniquely positioned to help secure America’s rare earth supply and reduce dependence on foreign sources.

"The 6 Mtpa case highlights Halleck Creek’s billion-dollar potential, delivering an NPV10% of US$1.17B and an IRR of 28%, showcasing the project’s scalability. The 3 Mtpa base case offers a low-risk entry point, producing 1,833 metric tonnes of NdPr oxide annually, with an NPV10% of US$558M, an IRR of 24%, and a 2.7-year payback period.

"With a scalable development pathway under evaluation, Halleck Creek has the potential to become a major supplier to U.S. and allied markets. Future production scenarios could position ARR among the top rare earth producers outside China, reinforcing America’s supply chain security for decades to come.

"And we’re not just mining—we are developing a fully integrated U.S. supply chain, refining and producing high- purity rare earth oxides for American manufacturers. Halleck Creek aligns with the growing push for Made-in- America critical minerals, securing a domestic supply for defense, aerospace, and high-tech manufacturing.”

Next Steps & Milestones

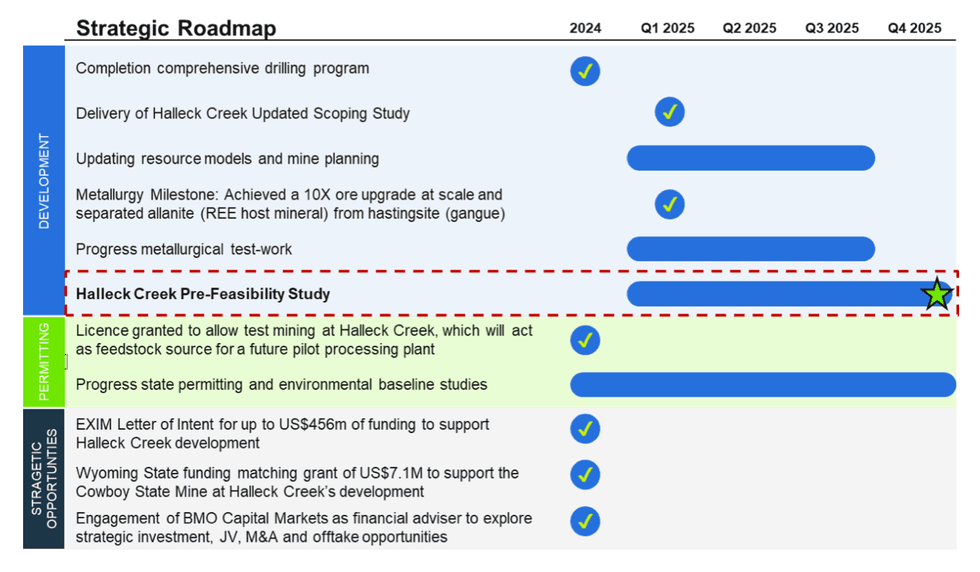

Building on strong execution in 2024, ARR is advancing key milestones to further de-risk and develop Halleck Creek, as outlined in the Updated Scoping Study and supported by recent metallurgy results. These developments reinforce the project's scalability and strategic importance as a leading U.S. rare earths asset. With a staged development approach, first production could be as early as 2029, subject to ongoing technical and economic assessments. The Company is looking at ways to fast-track development, including plans to commence Phase One of a pilot plant for the beneficiation process. The roadmap ahead highlights key next steps for 2025 and the next major stage gate in the project’s development.

Click here for the full ASX Release

This article includes content from American Rare Earths, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.