The Conversation (0)

Balkan Mining and Minerals Ltd (ASX: BMM; “BMM” or “the Company”) is pleased to announce the start of the phase 1 drill program at the Gorge Lithium Project located in Ontario, Canada (the "Gorge Lithium Project" or the "Project").

Highlights

The drill program has been designed to systematically test the vertical plunge extensions along strike of outcropping high-grade lithium pegmatites at the Nelson and Koshman occurrences. The phase 1 program comprises up to 1,000m of drilling across an area with very favourable initial results from systematic sampling programs that have identified multiple targets.

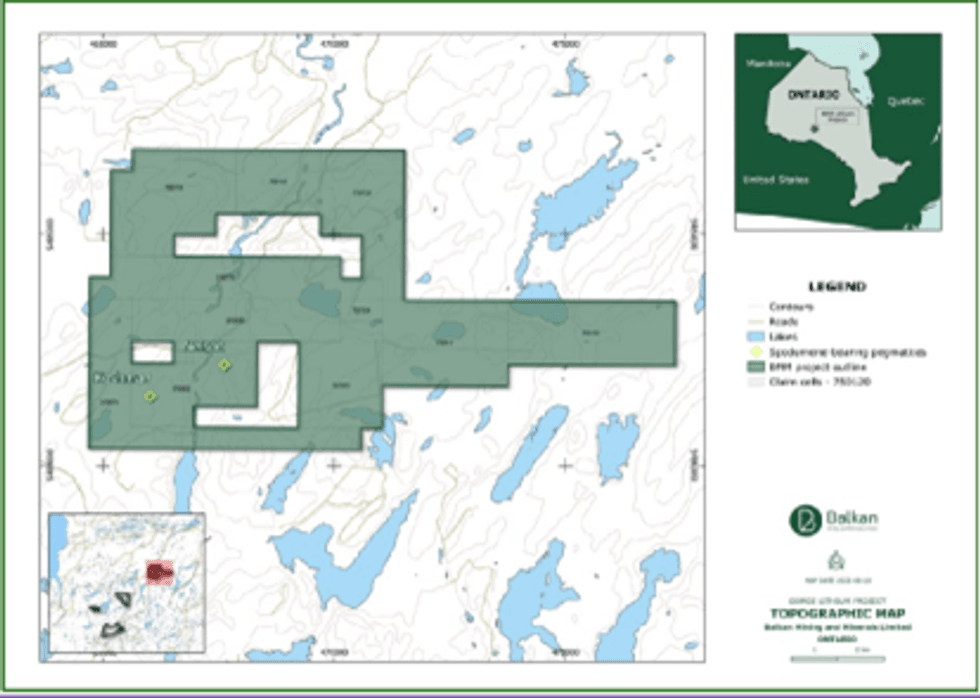

Figure 1 - Gorge Project Location Map

Figure 1 - Gorge Project Location Map

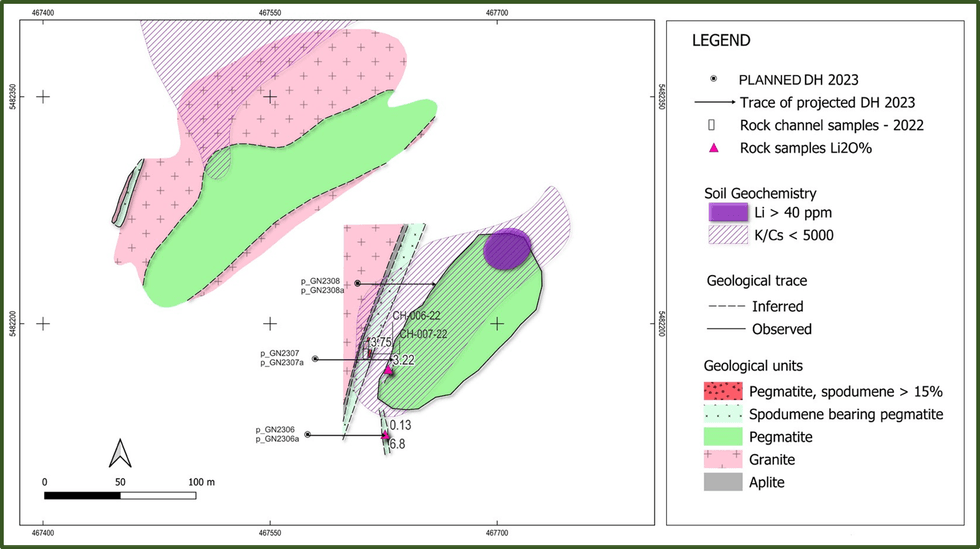

A total of six (6) Diamond Drill (DD) holes have been planned to be carried out at the Nelson pegmatite occurrence which will concentrate on the anomalies identified from previous channel sampling results, which included 1.8m @ 3.75% Li2O, further confirming significant potential of this project (see ASX Announcement dated 16 December 2022).

Figure 2 - Locations of Planned Diamond Drill holes at Nelson

Figure 2 - Locations of Planned Diamond Drill holes at Nelson

An additional six (6) DD holes have been planned to be drilled at the Koshman pegmatite occurrence to test targets identified from both channel and rock chips samples, which included 2.1m of 1.23% Li2O, including 1.1m of 2.2% Li2O from channel sampling and up to 4.28% Li2O from rock chip sampling program (see ASX Announcements dated 16 December 2022 and 28 September 2022).

Click here for the full ASX Release

This article includes content from Balkan Mining, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.