The Conversation (0)

Ivanhoe Mines' reports Q1 2026 loss of $2M and adjusted EBITDA of $191M, including $158M of attributable EBITDA from Kamoa-Kakula

Updated Kamoa-Kakula life-of-mine integrated development plan details launchpad for annualized copper production to return to over 500,000 tonnes per annum

Kamoa-Kakula Q1 2026 cost of sales of $3.90/lb. and cash cost (C1) of $2.58/lb. of copper, below guidance range of $2.60/lb. to $3.00/lb.

Kamoa-Kakula's operating margins boosted by the new on-site smelter; from sulphuric acid sales and significantly lower logistics costs

High-strength sulphuric acid production averaging 1,350 tonnes per day; new contract prices up >50% year-to-date at $725 per tonne

Construction of Platreef's Shaft #3 was completed on schedule, increasing hoisting capacity five-fold

Earthworks underway on Platreef's Phase 2 concentrator, targeting massive production increase from Q4 2027

Kipushi produced a record 65,044 tonnes of zinc in Q1 2026, at average cash cost (C1) of $0.86/lb. of zinc; cash costs tracking at low end of 2026 guidance range

Ivanhoe's 2026 group exploration budget upsized to $127M; $86M allocated to Makoko District in Western Forelands

Ivanhoe Mines' (TSX: IVN,OTC:IVPAF) (OTCQX: IVPAF) President and Chief Executive Officer, Marna Cloete, and Chief Financial Officer David van Heerden today announce the company's financial results for the first quarter of 2026, as well as an operations and project development update.

Ivanhoe Mines is a leading Canadian mining company with three principal tier-one mining operations in Southern Africa: the Kamoa-Kakula Copper Complex in the Democratic Republic of the Congo (DRC); the ultra-high-grade Kipushi zinc-copper-lead-germanium mine, also in the DRC; and the Platreef platinum, palladium, nickel, rhodium, gold, and copper mine in South Africa.

In addition, Ivanhoe Mines is expanding the Makoko District copper discovery in the Western Forelands, in the DRC, as well as exploring for new sedimentary-hosted copper discoveries across its vast and highly prospective exploration licence packages in the DRC, Angola, Zambia, and Kazakhstan.

All figures are in U.S. dollars unless otherwise stated.

Founder and Co-Chairman Robert Friedland commented:

Ivanhoe has a portfolio of tier-one mines powered by hydroelectric and solar power… built to withstand disruption. Our company is ideally positioned in this volatile environment, with exploding global demand for the copper, zinc, nickel and precious metals that we produce.

"Our Kamoa-Kakula Copper Complex and smelter are ramping up in a very strong price environment for the two most critical elements on our planet: copper, which is the King of Metals, and sulphuric acid (H2SO4), which is the King of Chemicals. Kamoa-Kakula benefits from a powerful natural hedge: our sulphuric acid production. H2SO4, which is a by-product of our copper smelter, is growing into a one-million-dollar-a-day operating credit, massively offsetting rising diesel prices. This advantage is supported by our high-grade ore, which has the lowest hydrocarbon intensity per tonne of produced copper of any major mine in the world.

"At the same time, our team are executing a disciplined turnaround at Kamoa-Kakula. The plan is clear, the execution is underway… and the strong tailwinds in copper prices adds to the momentum. We will fully capitalize on our strategic advantages.

"Ivanhoe leads the copper world in our exploration programs. We have extremely strong momentum in the discovery process for major copper systems. The Makoko District copper discovery in the Western Forelands is an emerging giant in the making, and its significance is growing around the clock. Soon, we will reveal our development plans for the Western Forelands."

FINANCIAL HIGHLIGHTS

OPERATIONAL HIGHLIGHTS

Conference call for investors on Thursday, May 7, 2026

Ivanhoe Mines will hold an investor conference call to discuss the results on Thursday, May 7, 2026, at 10:30 a.m. Eastern time / 7:30 a.m. Pacific time. The conference call will conclude with a question-and-answer (Q&A) session. Media are invited to attend on a listen-only basis.

To view the webcast, use the link:

https://meetings.lumiconnect.com/400-357-152-754

Audience Phone Number:

Local – Toronto: (+1) 416-855-9085

Toll Free – North America: (+1) 800- 990-2777

An audio webcast recording of the conference call, together with supporting presentation slides, will be available on Ivanhoe Mines' website at www.ivanhoemines.com.

After issuance, the condensed consolidated interim financial statements and Management's Discussion and Analysis will be available at www.ivanhoemines.com and www.sedarplus.ca.

Read Ivanhoe's 9th Annual Sustainability Report and First Quarter 2025 Sustainability Review:

https://www.ivanhoemines.com/investors/document-library/#sustainability

Ivanhoe's 2025 Annual Sustainability Review and Q1 2026 Quarterly Sustainability Review are both available in the sustainability section of our website.

The reports provide a detailed review of each project's health and safety, environmental, and social activities, as well as more information on the various sustainability initiatives underway across the group.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_ivanhoesustainability1.jpg

During the first quarter of 2026, the group achieved a combined Lost Time Injury Frequency Rate (LTIFR) of 0.41 and a Total Recordable Injury Frequency Rate (TRIFR) of 2.15 per 1,000,000 hours worked. Regrettably, two loss-of-life incidents occurred at Kamoa-Kakula during the quarter.

A breakdown of Ivanhoe's health and safety performance is available in the Q1 2025 Sustainability Review.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_ivanhoesustainability2.jpg

Principal projects and review of activities

1. Kamoa-Kakula Copper Complex

39.6%-owned by Ivanhoe Mines

Democratic Republic of the Congo

The Kamoa-Kakula Copper Complex is operated as the Kamoa Holding joint venture between Ivanhoe Mines and Zijin Mining. The complex covers a licence area of 400 square kilometres and is approximately 25 kilometres southwest of the town of Kolwezi on the far western edge of the Central African Copperbelt.

Kamoa Holding holds an 80% interest in Kamoa-Kakula, with the DRC government holding the remaining 20% interest. Ivanhoe and Zijin Mining, therefore, each hold an indirect 39.6% interest in Kamoa-Kakula, with Crystal River holding an indirect 0.8% interest. Kamoa-Kakula's full-time employee workforce is over 7,481, and over 90% are Congolese.

Copper production at Kamoa-Kakula commenced in May 2021 from the Phase 1 concentrator, which was delivered ahead-of-schedule. Two further concentrator expansions were also subsequently successfully delivered, also ahead of schedule, as well as an on-site 500,000-tonne-per-annum, direct-to-blister copper smelter that was completed in 2025. Kamoa-Kakula ranks among the largest and highest-grade copper complexes globally.

| Kamoa-Kakula summary of operating and financial data | |||||||||||||||

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |||||||||||

| Ore tonnes milled (000's tonnes) | 3,108 | 3,374(3) | 3,456 | 3,622 | 3,723 | ||||||||||

| Copper ore grade processed (%) | 2.32% | 2.35% | 2.47% | 3.58% | 4.10% | ||||||||||

| Copper recovery (%) | 85.6% | 85.7% | 82.7% | 85.4% | 87.4% | ||||||||||

| Copper in concentrate produced (tonnes) | 61,906 | 71,569 | 72,143 | 112,009 | 133,120 | ||||||||||

| Contained copper in blister or anode produced (tonnes)(1) | 71,417 | - | - | - | - | ||||||||||

| Payable copper sold (tonnes)(2) | 66,619 | 78,469 | 61,528 | 101,714 | 109,963 | ||||||||||

| Cost of sales per pound ($ per lb.) | 3.90 | 3.80 | 3.23 | 2.85 | 1.87 | ||||||||||

| Cash cost (C1) ($ per lb.) | 2.58 | 2.99 | 2.62 | 1.89 | 1.69 | ||||||||||

| Realized copper price ($ per lb.) | 5.79 | 4.98 | 4.42 | 4.34 | 4.19 | ||||||||||

| Sales revenue before remeasurement ($'000) | 872,539 | 782,691 | 555,293 | 868,846 | 922,411 | ||||||||||

| Remeasurement of contract receivables ($'000) | (10,237) | 83,353 | 11,072 | 6,443 | 50,986 | ||||||||||

| Sales revenue after remeasurement ($'000) | 862,302 | 866,044 | 566,365 | 875,289 | 973,397 | ||||||||||

| EBITDA ($'000) | 397,476 | 331,121 | 195,597 | 325,181 | 594,337 | ||||||||||

| EBITDA margin (% of revenue) | 46% | 38% | 35% | 37% | 61% | ||||||||||

All figures in the above tables are on a 100%-project basis. Metal reported in concentrate is before refining losses or deductions associated with smelter terms. This release includes "EBITDA", "Adjusted EBITDA", "EBITDA margin", "Pro-rata cash and cash equivalents" and "Cash cost (C1)", which are non-GAAP financial performance measures. For a detailed description of each of the non-GAAP financial performance measures used herein and a detailed reconciliation to the most directly comparable measure under IFRS Accounting Standards, please refer to the non-GAAP Financial Performance Measures and Pro-Rata Financial Ratios sections of the MD&A for the three months ended March 31, 2026.

(1) For 2026 only, contained copper includes copper produced by both Kamoa-Kakula's on-site smelter, as well as the toll-treatment of Kamoa-Kakula concentrate at the LCS smelter in Kolwezi. For 2025, toll-treated concentrate into blister at the LCS smelter is captured in the concentrate production of the Phase 1, 2 and 3 concentrators.

(2) Payable copper in concentrate sold is net of 96.7% payability. Payable copper in anode or blister sold is net of 99.7% payability.

(3) Ore tonnes milled in Q4 2025, excludes 160,000 tonnes of ore milled at the smelter's slag flotation plant.

Breakdown of cash cost (C1) per payable pound of copper in saleable product produced:

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | ||||||||||||||

| Mining | ($ per lb.) | 1.39 | 1.22 | 1.22 | 0.73 | 0.63 | ||||||||||||

| Processing | ($ per lb.) | 0.59 | 0.51 | 0.50 | 0.34 | 0.29 | ||||||||||||

| Smelter operating cost | ($ per lb.) | 0.27 | 0.01 | - | - | - | ||||||||||||

| Logistics charges | ($ per lb.) | 0.22 | 0.70 | 0.38 | 0.49 | 0.41 | ||||||||||||

| Refining & treatment charges | ($ per lb.) | 0.12 | 0.13 | 0.21 | 0.14 | 0.19 | ||||||||||||

| Sulphuric acid credits | ($ per lb.) | (0.32) | - | - | - | - | ||||||||||||

| General & Administrative | ($ per lb.) | 0.31 | 0.42 | 0.31 | 0.19 | 0.17 | ||||||||||||

| Cash cost (C1) | ($ per lb.) | 2.58 | 2.99 | 2.62 | 1.89 | 1.69 |

Units in U.S. dollars per payable pound of copper in saleable product produced

The cost of power, which is allocated between mining, processing and smelting in the above cash cost split, can be split out as follows:

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | ||||||||||||||

| Power costs | ($ per lb.) | 0.47 | 0.33 | 0.35 | 0.20 | 0.24 | ||||||||||||

| Power costs as a proportion of total cash cost (C1) | (%) | 18.2% | 11.0% | 13.4% | 10.6% | 14.2% |

Units in U.S. dollars per payable pound of copper in saleable product produced

Cash cost (C1) is prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines, but is not a measure recognized under IFRS Accounting Standards. In calculating the C1 cash cost, the costs are measured on the same basis as the company's share of profit from the Kamoa Holding joint venture, which is contained in the financial statements. C1 cash cost is used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered, finished metal. C1 cash cost excludes royalties, production taxes, and non-routine charges as they are not direct production costs.

All figures are on a 100% project basis, and metal reported in concentrate is before refining losses or deductions associated with smelter terms.

Kamoa-Kakula produced 71,417 tonnes of contained copper in anode during Q1 2026 at a cash cost (C1) of $2.58/lb.

During the first quarter of 2026, the Phase 1, 2, and 3 concentrators milled a total of 3.11 million tonnes of ore, producing 61,906 tonnes of copper. As revised on March 31, 2026, Kamoa-Kakula's annual production guidance of 290,000 to 330,000 tonnes of copper is maintained.

At quarter-end, inventory contained more than 40,000 tonnes of copper, down from approximately 50,000 tonnes at the end of 2025. The copper inventory at Kamoa-Kakula includes copper in concentrate at the smelter, in the smelter circuit, and in produced anodes. The copper inventory at LCS includes copper in concentrate and in produced blister. In addition, Kamoa-Kakula's on-site copper smelter produced 117,871 tonnes of high-strength sulphuric acid during the quarter. There were 18,578 tonnes of high-strength sulphuric acid in inventory at the end of Q1 2026.

| Summary of quarterly production data from Kamoa-Kakula | |||||||||||||||

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |||||||||||

| Phase 1 & 2 | |||||||||||||||

| Ore tonnes milled (000's tonnes) | 1,534 | 1,712 | 1,838 | 1,991 | 2,211 | ||||||||||

| Copper ore grade processed (%) | 2.35% | 2.32% | 2.50% | 4.12% | 5.01% | ||||||||||

| Copper recovery (%) | 84.1% | 83.2% | 81.3% | 85.4% | 88.3% | ||||||||||

| Copper in concentrate produced (tonnes) | 30,527 | 34,602 | 37,744 | 71,401 | 97,575 | ||||||||||

| Phase 3 | |||||||||||||||

| Ore tonnes milled (000's tonnes) | 1,574 | 1,662 | 1,618 | 1,631 | 1,512 | ||||||||||

| Copper ore grade processed (%) | 2.28% | 2.38% | 2.44% | 2.92% | 2.76% | ||||||||||

| Copper recovery (%) | 87.2% | 88.2% | 84.2% | 85.5% | 85.1% | ||||||||||

| Copper in concentrate produced (tonnes) | 31,379 | 34,814 | 33,522 | 40,608 | 35,545 | ||||||||||

| Combined Phase 1, 2 and 3(1) | |||||||||||||||

| Ore tonnes milled (000's tonnes) | 3,108 | 3,374 | 3,456 | 3,622 | 3,723 | ||||||||||

| Copper ore grade processed (%) | 2.32% | 2.35% | 2.47% | 3.58% | 4.10% | ||||||||||

| Copper recovery (%) | 85.6% | 85.7% | 82.7% | 85.4% | 87.4% | ||||||||||

| Copper in concentrate produced (tonnes) | 61,906 | 69,416 | 71,266 | 112,009 | 133,120 | ||||||||||

| Smelter | |||||||||||||||

| Contained copper in blister or anode(2) (000's tonnes) | 71,417 | - | - | - | - | ||||||||||

| High-strength sulphuric acid (tonnes) | 117,871 | - | - | - | - | ||||||||||

| Data in bold denotes a quarterly or annual record. | |||||||||||||||

| (1) Excludes ore milled and copper in concentrate produced by smelter's slag flotation plant, prior to heat-up of the smelter. The slag flotation plant produced 2,153 tonnes of copper in concentrate and 877 tonnes of copper in concentrate in Q3 2025 and Q4 2025, respectively. (2) For 2026 only, contained copper includes copper produced by both Kamoa-Kakula's on-site smelter, as well as the toll-treatment of Kamoa-Kakula concentrate at the LCS smelter in Kolwezi. For 2025, toll-treated concentrate into blister at the LCS smelter is captured in the concentrate production of the Phase 1, 2 and 3 concentrators. | |||||||||||||||

Kamoa mining area to ramp up volumes as Kakula mine development advances towards re-opening higher-grade areas

For Q2 2026, the Kamoa mines area, which includes the Kamoa 1, Kansoko and Kahala underground mines, is expected to mine at a combined rate of 540,000 tonnes per month, equivalent to 6.5 million tonnes per annum (Mtpa) on an annualized basis, with a head grade of approximately 2.3% copper. There is sufficient ore from the Kamoa mines to fully utilize the Phase 3 concentrator.

In the second half of 2026, the mining rate from the Kamoa mines area is expected to increase to approximately 700,000 tonnes per month, or 8.5 Mtpa on an annualized basis. The increase in the mining rate is driven primarily by production from the new Kahala box cut. The increase in tonnes mined at Kamoa in the second half of 2026 will be processed by the Phase 1 and 2 concentrators.

The Phase 1 and 2 concentrators have completed the processing of the surface stockpiles. Ore feed into the Phase 1 and 2 concentrators in Q2 2026 will come from the western side of Kakula at a rate of approximately 400,000 tonnes per month, or 4.8 Mtpa annualized, at a grade of approximately 3% copper. Throughout the second quarter, the Phase 1 and 2 concentrators will be campaigned, or batch operated, due to reduced ore availability.

In the second half of 2026, the mining rate at Kakula is expected to increase to 500,000 tonnes per month, or 6.0 Mtpa annualized, at an average grade of approximately 3.5% copper.

The above production rates are factored into the 2026 guidance, which was revised on March 31, 2026, to between 290,000 and 330,000 tonnes of contained copper in anode or blister.

Updated Mineral Resource estimate reaffirms the long-term potential of the Kamoa-Kakula Copper Complex

The Kamoa-Kakula MRE, released on March 31, 2026, underpins a mine plan for the Kamoa-Kakula Copper Complex to ramp up production to over 500,000 tonnes of copper per annum from 2028 onwards. This includes operating the Phase 1, 2 and 3 concentrators at a steady-state rate of 17 million tonnes per annum over approximately 25 years.

The updated Indicated Mineral Resource estimate is relatively unchanged at 1.27 billion tonnes of ore at a grade of 2.65%, containing approximately 34 million tonnes of copper, supporting long-term optionality, including the potential for a Phase 4 expansion. In addition, the Inferred Mineral Resources consist of a further 336 million tonnes grading 1.82%, containing approximately 6.1 million tonnes of copper.

The updated Mineral Reserve estimate is 466 million tonnes of ore at a grade of 2.82% copper, containing 13.1 million tonnes of copper. This estimate incorporates changes to the mine design and extraction sequence, taking into account cautious geotechnical parameters from

world-leading experts. In addition, the Mineral Reserve estimate does not include any tonnes inside Kakula's existing workings, which were developed prior to the seismic activity.

Following recommendations from the Kamoa-Kakula MRE, Kamoa Copper has commenced work on an optimized Feasibility Study covering the next five years of operation. This will be accompanied by a Pre-Feasibility Study (PFS) on the remaining life-of-mine. The study is expected to be completed in Q1 2027.

Launchpad for Kamoa-Kakula's return to over 500,000 tonnes of copper is set as crews advance back toward the high-grade eastern section

Kamoa-Kakula will increase focus on development activities over the next 18-24 months, establishing long-term access development and mine services ahead of the active mining fronts, applying conservative near-term underground development advance rates.

Development will focus on establishing the peripheral access drives around the Kakula Mine before stoping (production mining) in the newly developed mining areas begins. Production stoping is planned to start at Kamoa in H2 2026 and stoping at Kakula is expected to commence in H1 2027.

Project 95 upgrades to the Phase 1 and 2 concentrators near completion; commissioning underway

The Project 95 upgrades to the Phase 1 concentrator have been completed, with commissioning well advanced. The Project 95 upgrades to the Phase 2 concentrator are expected to be completed in the coming weeks. Both sets of upgrades are expected to be fully commissioned and operational in June.

Kamoa-Kakula's Project 95 is expected to increase Phase 1 and 2 concentrator recoveries to 95% from the design recovery rate of 87% by regrinding and refloating the underflow from the tailings concentrator thickener.

Construction of Project 95 is complete, with commissioning underway. Once ramped up, Project 95 is expected to boost the recovery of the Phase 1 and 2 concentrators by up to 95%, depending on feed grade.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_004full.jpg

Kamoa-Kakula's on-site, 500,000 tonnes-per-annum copper smelter ramped up to 60% capacity; By-product sulphuric acid sales benefiting from global supply chain disruptions

The smelter is targeting production of approximately 850 tonnes per day of copper in anode, equivalent to an annualized rate of 300,000 tonnes of copper, which is approximately 60% of the design capacity. Further ramp-up is constrained by the availability of concentrate to feed the smelter. Management is currently evaluating the toll treatment of local third-party copper concentrates to further advance the smelter ramp-up and improve margins.

In addition to copper anodes, the smelter is producing high-strength sulphuric acid at an average rate of 1,350 tonnes per day, equivalent to 60% of the annualized production capacity. The first sales of acid from the smelter took place in early 2026 to nearby mining operations in the DRC Copperbelt. There are currently six offtakers purchasing acid from Kamoa-Kakula's mine gate.

The market in the DRC Copperbelt for sulphur and high-strength sulphuric acid remains tight, predominantly due to the following factors: the closure of the Strait of Hormuz, which is a source for approximately 80% of sulphur imported into Africa; export restrictions of acid imposed by Zambia; and, smelters in Zambia and the DRC, which produce sulphuric acid as byproduct, are currently shut down for maintenance.

An offtake contract for Kamoa-Kakula's sulphuric acid was recently signed for delivery in June and priced at $725 per tonne. All remaining offtake contracts will be retendered and repriced by the end of the quarter.

The first shipment of 99.7%-pure copper anodes produced by Kamoa-Kakula's copper smelter, shipped along the Lobito Railway Corridor, arrived at the Atlantic port of Lobito during the quarter. The anodes are currently being shipped to Europe for refining and are expected to arrive imminently. The transit time from the DRC Copperbelt to Lobito port via rail averages seven days, compared with more than three weeks when transported by truck to the ports of Durban or Dar es Salaam. Flooding in April caused temporary damage to parts of the Lobito Corridor's rail infrastructure in Angola. Shipments of Kamoa-Kakula's anodes along the rail line have temporarily stopped, but are expected to resume later this month.

The sulphuric acid load out facility at Kamoa-Kakula's on-site copper smelter. The smelter produced 117,871 tonnes of high-strength sulphuric acid during the first quarter.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_005full.jpg

The construction of Kamoa-Kakula's on-site, 60-MW solar facility with battery storage is expected to be operational from early Q3; plans well advanced to double on-site solar capacity to 120 MW by the end of 2027

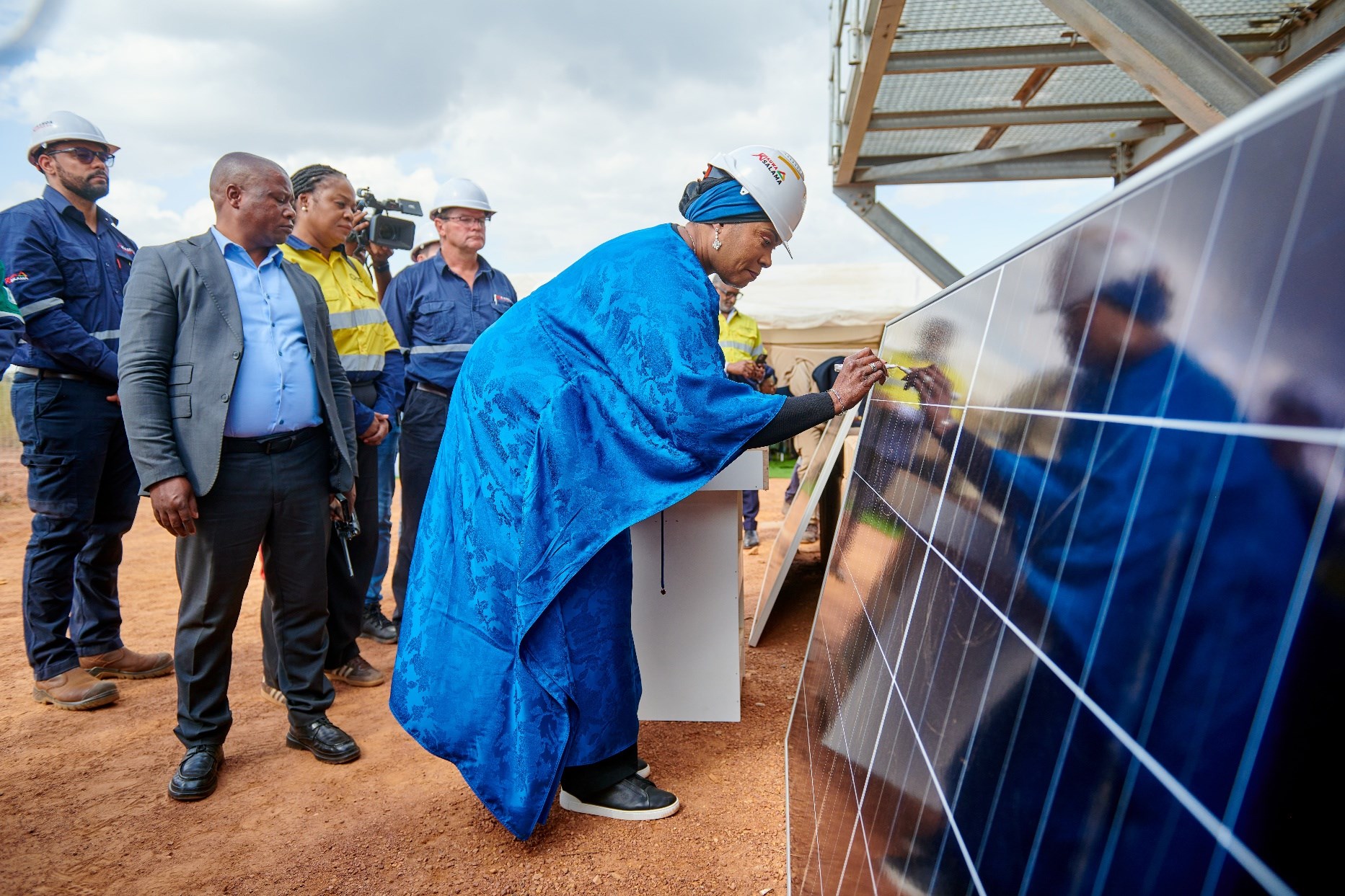

Construction of Kamoa-Kakula's on-site solar photovoltaic (PV) facilities is nearing completion. The facilities are expected to deliver a combined 60 MW of baseload power to the copper complex from July. The two facilities are owned, operated, and funded by CrossBoundary Energy and Green World Energie. The two facilities have a combined installed capacity of 433 MW of Solar Photovoltaic (PV) and 1,107 MWh of battery energy storage system (BESS) capacity. Kamoa Copper will be the sole offtaker of the electricity produced by both facilities. The 60-MW facility, once commissioned, will be the largest solar project of its kind with battery storage on the African continent.

Kamoa-Kakula is advancing plans to double the on-site solar power capacity, with battery storage, to 120 MW by the end of 2027. On April 24, 2026, a tender was awarded and a PPA was signed for an additional 30-MW on-site solar PV facility, with battery storage. Construction is expected to be completed in Q3 2027. Her Excellency, Fifi Masuka Saini, Governor of Lualaba Province, DRC, attended the signing ceremony of the PPA with Green World Energie. A further 30 MW solar PV facility is currently undergoing tender adjudication and is expected to be awarded in the coming month.

Aerial view over Kamoa-Kakula's solar (PV) facility with battery storage. Once operational in early Q3 2026, the facility will be the largest solar project with battery storage of its kind in Africa.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_006full.jpg

Her Excellency Fifi Masuka Saini, Governor of Lualaba Province, DRC, attended the signing ceremony of the power purchase agreement for the expansion of the on-site solar facilities at Kamoa-Kakula. Kamoa-Kakula plans to have a total of 120 MW of on-site solar power capacity, with battery storage, installed by the end of 2027.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_007full.jpg

COPPER PRODUCTION, CASH COST AND CAPITAL EXPENDITURE GUIDANCE

| Kamoa-Kakula Guidance | 2026 | 2027 | ||||

| Contained copper in anode or blister (tonnes) | 290,000 - 330,000 | 380,000 - 420,000 | ||||

| Cash cost (C1) ($ per payable pound of copper in saleable product produced) | 2.60 - 3.00 | 2.10 - 2.50 | ||||

| Capital expenditure ($ million) | 1,100 - 1,400 | 750 - 950 |

Guidance figures are on a 100% project basis and metal reported in concentrate is before refining losses associated with smelter terms.

Kamoa-Kakula's guidance is based on several assumptions and estimates. It involves estimates of known and unknown risks, uncertainties, and other factors that may cause the actual results to differ materially.

Although mining of the Kakula orebody has restarted, risk factors remain, including the integrity of underground infrastructure, once fully dewatered, the ability to ramp up underground operations in line with expectations, and the ability to access new mining areas in the required time. Guidance for Kamoa-Kakula is based on an assessment of these factors that management believes are reasonable at this time, given all available information.

2026 and 2027 production and cash cost (C1) guidance, which was revised on March 31, 2026, includes updated mine designs at both the Kamoa and Kakula mines which include a longer period of up-front development to support a more sustainable future rate of mining. Development will be focused over the next two years to complete more peripheral development around the Kakula Mine before stoping of the newly developed areas begin. Ivanhoe Mines targets annualized copper anode or blister production to return to over 500,000 tonnes from 2028, at a target cash cost (C1) of less than $2.00/lb.

Production guidance from 2026 is reported as contained tonnes of copper in anode or blister, whereas previously guidance was provided as copper in concentrate. With the ongoing ramp-up of the on-site Kamoa-Kakula smelter to its annualized run rate of 500,000 tonnes per annum, the majority of concentrate produced by the Phase 1, 2, and 3 concentrators is expected to be processed through the smelter producing copper anodes.

Cash cost (C1) guidance is based primarily on assumptions, including tonnes of ore mined, feed grades of processed copper ore, concentrator recoveries, as well as the timing and ramp-up of the on-site smelter, among other variables.

The 2026 cash cost (C1) guidance for Kamoa-Kakula is based on assumptions relating to the expected realization price of high-strength sulphuric acid price and the cost of diesel. Both the average realized price of sulphuric acid and the average cost of diesel has increased above the Q1 2026 levels. Although Ivanhoe Mines catered for a temporary period of elevated diesel prices when setting its cash cost (C1) guidance, if the current prices for high strength sulphuric acid and diesel remains at the current levels for the remainder of the year, Ivanhoe estimates that cash cost (C1) will be 5% higher than initially estimated.

Cash cost (C1) is a non-GAAP measure used by management to evaluate operating performance and includes all direct mining, processing, stockpile rehandling, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination (predominantly China), which are recognized as a component of sales revenues, are added to cash cost (C1) to arrive at an approximate cost of delivered finished metal.

For historical comparatives and a reconciliation to the most directly comparable measure under IFRS, see the non-GAAP Financial Performance Measures section of the MD&A for the three months ended March 31, 2026.

2. Kipushi Mine

62%-owned by Ivanhoe Mines

Democratic Republic of the Congo

The ultra-high grade Kipushi underground zinc-copper-germanium-silver-lead mine in the DRC is located adjacent to the town of Kipushi on the Zambian border, approximately 30 kilometres southwest of Lubumbashi on the Central African Copperbelt. Kipushi is approximately 250 kilometres southeast of the Kamoa-Kakula Copper Complex. Ivanhoe acquired a 68% interest in the Kipushi Mine in November 2011, through Kipushi Holding, which is 100%-owned by Ivanhoe Mines. The balance of 32% in the Kipushi Mine was held by the DRC state-owned mining company, Gécamines. As per the updated joint venture agreement signed in late 2023, Gécamines' ownership increased to 38% in Q1 2025.

Ivanhoe, together with its joint-venture partner, restarted the Kipushi zinc mine in mid-2024, with the ramp-up to steady state operations continuing during the quarter. On November 17, 2024, His Excellency Félix Tshisekedi, President of the Democratic Republic of the Congo, along with a government delegation, officially reopened the Kipushi zinc mine. Ramp-up of Kipushi is ongoing, following the successful completion of the debottlenecking program in Q3 2025.

Kipushi summary of operating and financial data

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |||||||||||

| Kipushi concentrator | |||||||||||||||

| Ore tonnes milled (tonnes) | 196,774 | 194,140 | 168,862 | 153,342 | 151,403 | ||||||||||

| Feed grade of ore milled (% zinc) | 36.96% | 36.18% | 37.81% | 33.37% | 32.16% | ||||||||||

| Zinc recovery (%) | 90.63% | 87.71% | 89.36% | 85.22% | 87.93% | ||||||||||

| Zinc in concentrate produced (tonnes) | 65,044 | 61,444 | 57,200 | 41,788 | 42,736 |

Data in bold denotes a quarterly record.

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |||||||||||

| Payable zinc sold (tonnes) | 54,940 | 48,075 | 49,744 | 43,348 | 30,108 | ||||||||||

| Cost of sales per pound ($ per lb.) | 1.06 | 1.13 | 1.11 | 1.05 | 1.23 | ||||||||||

| Cash cost (C1) ($ per lb.) | 0.86 | 0.86 | 0.95 | 0.96 | 0.93 | ||||||||||

| Realized zinc price ($ per lb.) | 1.47 | 1.44 | 1.27 | 1.23 | 1.29 | ||||||||||

| Sales revenue before remeasurement ($'000) | 160,142 | 133,792 | 126,855 | 92,875 | 79,713 | ||||||||||

| Remeasurement of contract receivables ($'000) | 1,400 | 4,246 | 2,548 | 3,882 | (2,693 | ) | |||||||||

| Sales revenue after remeasurement ($'000) | 161,542 | 138,038 | 129,403 | 96,757 | 77,020 | ||||||||||

| EBITDA ($'000) | 58,485 | 44,211 | 26,674 | 9,295 | 10,508 | ||||||||||

| EBITDA margin (% of sales revenue) | 36% | 32% | 21% | 10% | 14% |

C1 cash cost per pound of payable zinc sold can be further broken down as follows:

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | ||||||||||||||

| Mining | ($ per lb.) | 0.17 | 0.18 | 0.18 | 0.16 | 0.16 | ||||||||||||

| Processing | ($ per lb.) | 0.07 | 0.09 | 0.05 | 0.08 | 0.12 | ||||||||||||

| Logistics charges | ($ per lb.) | 0.46 | 0.44 | 0.49 | 0.50 | 0.47 | ||||||||||||

| Treatment charges | ($ per lb.) | 0.07 | 0.07 | 0.07 | 0.07 | 0.05 | ||||||||||||

| Support services | ($ per lb.) | 0.09 | 0.08 | 0.16 | 0.15 | 0.13 | ||||||||||||

| Cash cost (C1) per pound of payable zinc sold | ($ per lb.) | 0.86 | 0.86 | 0.95 | 0.96 | 0.93 |

Cash cost (C1) is prepared on a basis consistent with the industry standard definitions by Wood Mackenzie cost guidelines but cash cost per pound for the Kipushi Mine has been presented on a per tonne sold basis to eliminate the impact of unsold tonnes of zinc concentrate in inventory. Cash cost (C1) and cash cost per pound are not measures recognized under IFRS Accounting Standards. C1 cash cost is used by management to evaluate operating performance and includes all direct mining, processing, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination, which are recognized as a component of sales revenues, are added to C1 cash cost to arrive at an approximate cost of delivered, finished metal. C1 cash cost excludes royalties, production taxes and non-routine charges as they are not direct production costs.

All figures are on a 100% project basis and metal reported in concentrate is before refining losses or deductions associated with smelter terms.

Kipushi concentrator produced a record 65,044 tonnes of zinc during the quarter

The Kipushi concentrator delivered another record quarter, milling a record 196,774 tonnes of ore at an average grade of 36.96%, producing a record 65,044 tonnes of zinc in concentrate, including a monthly record of 22,968 tonnes in January. The record quarterly production represented a 6% increase compared to Q4 2025. In addition, for the first time, concentrator recoveries averaged over 90% during the quarter. Cash costs (C1) for the first quarter averaged the record set in Q4 2025 of $0.86/lb. Cash costs for the quarter tracked at the low end of full-year guidance of $0.85/lb. to $0.95/lb.

Despite the quarterly record production, the Kipushi concentrator's availability was still affected by electrical grid instability. In addition to increasing the on-site back-up generator capacity in Q4 2025 by 20% to 20MW, upgrades to Kipushi's 120kV electrical intake substation were completed and commissioned in late Q1 2026. The main benefit of the upgrade is that it enables Kipushi operations to safely control and respond more effectively to grid instability. The upgrades will thereby improve the availability and protect the operations of the major infrastructure, such as the concentrator and shaft.

Construction of Kipushi's second tailings storage facility is progressing well

Construction of the second tailings storage facility (TSF) is over 80% complete, with the first deposit of tailings expected from October 2026. Lining of the new TSF's paddock 2B extension has commenced. The new TSF, along with the existing TSF, have been designed to be compliant with Global Industry Standard on Tailings Management (GISTM).

Aerial view of the Kipushi Mine's tailings storage facilities with the new facility under construction (right) adjacent to the existing storage facility (left). The new facility will be fully lined and GISTM compliant. The first deposit of tailings into the new TSF is expected in October 2026.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_008full.jpg

Tendering underway for 10-MW solar facility with battery storage dedicated to the Kipushi Mine.

A tender is currently underway for a solar project, with battery energy storage, dedicated to the Kipushi Mine. The facility would provide baseload power of 10 MW, with up to 200 MWh of battery storage to deliver continuous power over 24 hours. The facility is designed to reduce reliance on backup diesel generators that are used intermittently. The facility would be located on a 70-hectare site, close to the Kipushi Mine site, and would be owned and operated by a third party on a take-or-pay basis. Construction completion is targeted by the end of 2027.

ZINC PRODUCTION, CASH COST AND CAPITAL EXPENDITURE GUIDANCE FOR 2026

| Kipushi 2026 Guidance | |||

| Contained zinc in concentrate (tonnes) | 240,000 to 290,000 | ||

| Cash cost (C1) ($ per pound of payable zinc) | 0.85 to 0.95 | ||

| Capital expenditure ($ million) | 60 |

Guidance figures are on a 100% project basis.

Kipushi's guidance is based on several assumptions and estimates of known and unknown risks, uncertainties, and other factors that may cause the actual results to differ, including the reliability of DRC grid power supply and prevailing logistics rates, among other variables. Metal reported in concentrate is before treatment losses or payability deductions associated with smelter terms.

Kipushi Mine produced 65,044 tonnes of zinc in the first quarter of 2026.

Cash cost (C1) is a non-GAAP measure used by management to evaluate operating performance and includes all direct mining, processing, stockpile rehandling charges, and general and administrative costs. Smelter charges and freight deductions on sales to the final port of destination, which are recognized as a component of sales revenues, are added to cash cost (C1) to arrive at an approximate cost of delivered finished metal.

For historical comparatives and a reconciliation to the most directly comparable measure under IFRS see the non-GAAP Financial Performance Measures section of the company's MD&A for the three months ended March 31, 2026.

3. Platreef Mine

64%-owned by Ivanhoe Mines

South Africa

The Platreef Mine is located on the Northern Limb of the Bushveld Igneous Complex in Limpopo Province - approximately 280 kilometres northeast of Johannesburg and eight kilometres from the town of Mokopane in South Africa. The project is owned by Ivanplats (Pty) Ltd. (Ivanplats), which is 64%-owned by Ivanhoe Mines. A 26% interest is held by Ivanplats' historically disadvantaged, broad-based, black economic empowerment (B-BBEE) partners, which include 20 local host communities with approximately 150,000 people, project employees, and local entrepreneurs. The remaining 10% interest is held by a Japanese consortium, consisting of ITOCHU Corporation, Japan Organization for Metals and Energy Security (JOGMEC), and Japan Gas Corporation.

Platinum-group metals (PGM) mineralization in the Northern Limb is primarily hosted within a 30-kilometre mineralized sequence. Platreef is contiguous with, and along strike from, Valterra Platinum's Mogalakwena PGM operations. Platreef hosts an underground deposit of platinum-group metals, nickel, copper, and gold mineralization, called the Flatreef deposit. The Flatreef is a thick, relatively flat-lying and high-grade orebody, which is amenable to highly mechanized, highly productive, underground bulk mining methods.

Since 2007, Flatreef has become one of the largest undeveloped precious metals deposits globally, with 56 million ounces in platinum equivalent Indicated Mineral Resources and 74 million ounces in platinum equivalent Inferred Mineral Resources, at a 2.0 g/t 3PE + AU cut-off. The Flatreef is also host to one of the world's largest undeveloped nickel sulphide mineral resources.

Following the successful opening of the Platreef Mine in November, 2025, ramp-up of the Phase 1 concentrator is advancing, with commercial production expected mid-year.

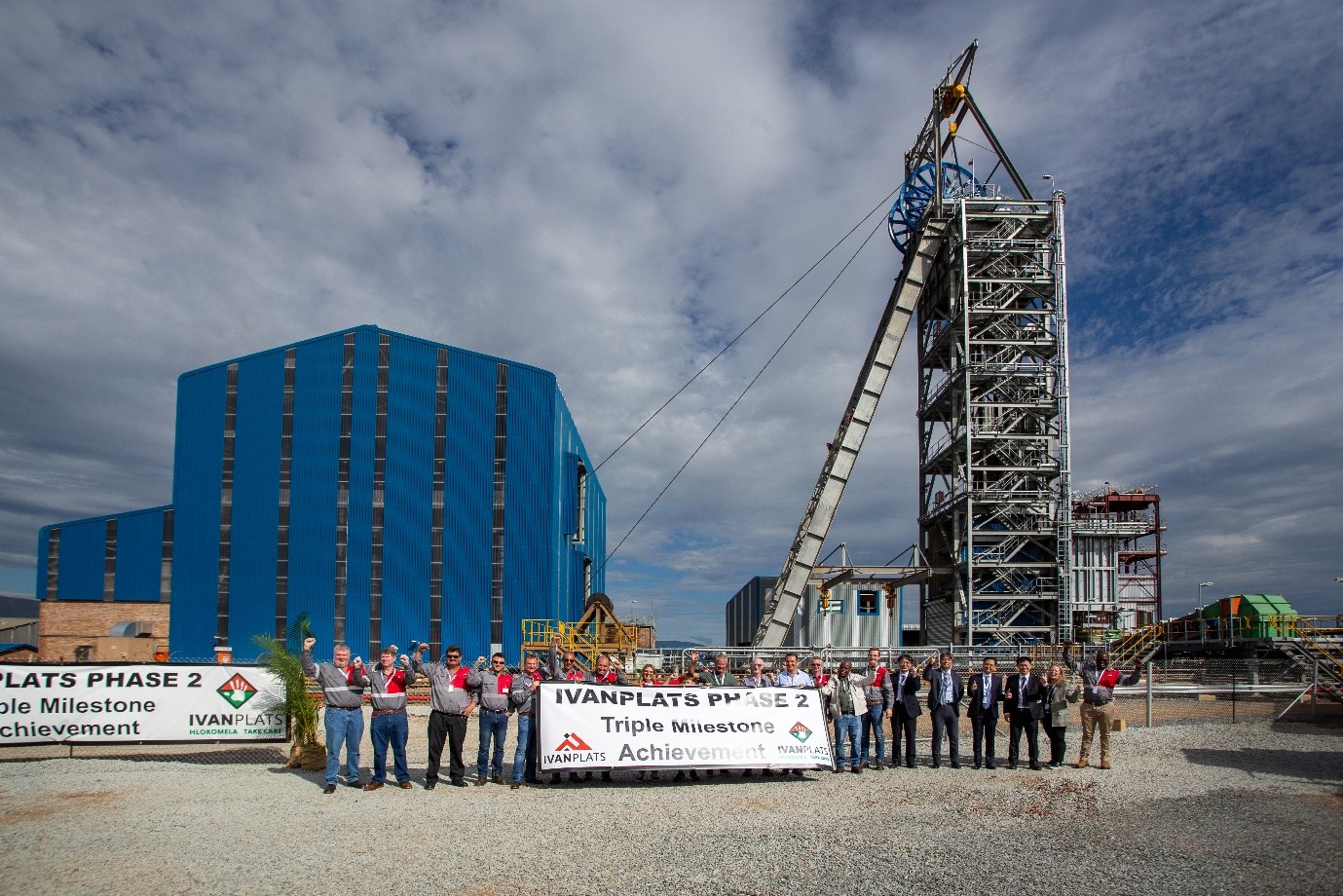

Senior representatives from Ivanplats, Ivanhoe Mines and the Japanese Consortium, in front of the recently completed Shaft #3 headframe and winder house, are celebrating the completion of three major project milestones in the ongoing ramp-up of the Phase 1 operations and the future Phase 2 expansion.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_009full.jpg

Platreef summary of quarterly production data from Phase 1 commissioning

| Q1 2026 | Q4 2025 | Q3 2025 | |||||||

| Platreef Phase 1 concentrator | |||||||||

| Ore tonnes milled (DMT) | 27,512 | 25,543 | - | ||||||

| Feed grade of ore milled (g/t) | 2.78 | 2.64 | - | ||||||

| Recovery (%) | 57% | 45% | - | ||||||

| PGM production (3PE + Au ounces) | 1,428 | 965 | - |

Shaft #3 to expand hoisting capacity at the Platreef Mine five-fold, unlocking Phase 1 operations while supporting underground development for Phase 2 expansion from Q4 2027

Production from the 0.8-Mtpa Phase 1 concentrator started on November 18, 2025. Since first production, approximately 2,400 ounces of platinum, palladium, rhodium, and gold have been produced.

Since first production, the Platreef Mine's Phase 1 concentrator has batch-processed (campaigned) lower-grade development ore. Therefore, production results are not representative of Phase 1's steady-state operations. The recent completion of Shaft #3 increases hoisting capacity by approximately five times, enabling the concurrent hoisting of ore and development waste, which was previously not possible with Shaft #1 alone. Once Shaft #3 is ramped up within the coming weeks, the hoisting bottleneck will be removed, and the Phase 1 concentrator will be continuously fed with higher-grade ore from production mining. The first long-hole stope blast (production mining) took place in early April on the 850-metre level. The Phase 1 concentrator is expected to steadily ramp up to commercial production from mid-year.

Construction of Platreef's Shaft #3, along with its associated underground materials-handling and crushing plants, was completed on schedule in late March and is currently undergoing the final stages of commissioning. In addition, on April 1, 2026, the winder license was approved by the regulator, authorizing the shaft's commercial use. Shaft #3 will also hoist the waste development required in preparation for the Phase 2 expansion, which is on schedule to be completed by the end of 2027. Early works on the Phase 2 expansion's surface infrastructure also started during the first quarter. The breaking of ground on the 3.3-million-tonne-per-annum Phase 2 concentrator site took place ahead of schedule on April 9, 2026.

Underground development will also significantly ramp up in preparation for the start-up of the Phase 2 concentrator, which is expected to be operational by the end of next year. Underground development will focus on opening additional mining areas to increase the mining rate to feed the new 3.3-Mtpa Phase 2 concentrator.

Shaft #2's slipe and line contract was awarded to United Mining Services (UMS) of Johannesburg, South Africa, in Q1 2026. The slipe and line method is a mining technique used to widen vertical shafts, while simultaneously installing a permanent lining to support the shaft walls. Using this method, Shaft #2 will be widened from its current diameter of 3.1 metres to 10 metres. Site mobilization was completed by UMS during the first quarter, with the first 'slipe' blast of Shaft #2 taking place on schedule on April 1, 2026. Shaft #2 is expected to be ready to hoist labour and materials by the end of 2028 and ready to hoist ore by the end of 2029, supporting both the steady-state operations of Phase 2, as well as the future Phase 3 expansion.

Breaking of ground took place at Phase 2 concentrator construction site; Phase 2 is expected to increase production to over 450,000 ounces of platinum, palladium, rhodium and gold from Q4 2027

The Ivanplats' project team broke ground on the Phase 2 concentrator site on April 9, 2026. DRA Global is the engineering, procurement, and construction management (EPCM) contractor for the Phase 2 underground infrastructure and the 3.3-million-tonne-per-annum Phase 2 concentrator. DRA Global was the EPCM contractor that delivered Platreef's Phase 1 concentrator on schedule in June 2024. The Phase 2 concentrator is targeted for completion by the end of next year.

Concurrently with the major earthworks now underway at the Phase 2 concentrator site, engineering work is focused on completing the process and mechanical design and equipment layouts. The procurement of long-lead mechanical and electrical equipment has already commenced.

Platreef's $700 million Phase 2 project finance facility closed

In December 2023, Ivanplats concluded a senior debt facility with Société Générale and Nedbank Limited to fund the construction of Phase 1. An initial $70 million was drawn, with a further $30 million drawn in the second quarter of 2025.

Following the completion of the Phase 2 expansion study, Ivanhoe Mines entered into negotiations to enlarge the project finance package to fund the Phase 2 expansion's capital requirements. As announced on January 12, 2026, credit approvals were received, and underwriting engagements were signed with Societe Generale, Absa Bank Limited and Nedbank Limited for a $700 million senior project finance facility. The Phase 2 facility amends and upsizes the Phase 1 facility, resulting in approximately $600 million of net additional capital. Financial close of the upsized senior project finance facility took place on April 30, 2026.

Financing for the future Phase 3 expansion is expected to be underpinned by cash flow generated from Platreef's Phase 1 and 2 operations.

Ivanplats' senior management and project team at the breaking of ground of the Phase 2 concentrator construction site. Construction of the 3.3-Mtpa concentrator is expected to be completed in Q4 2027.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_010full.jpg

Aerial view of the Platreef Mine site, showing the existing surface infrastructure, as well as an outline of the locations for the future Phase 2 and 3 concentrators, adjacent to the current Phase 1 concentrator.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_011full.jpg

4. Global Exploration Portfolio

Ivanhoe's group exploration budget has been upsized to $127 million from $90 million for 2026. The 2026 budget is more than double the group's 2025 exploration expenditure of $60 million, as confidence continues to grow across the company's exploration portfolio. The total group exploration budget is allocated as follows: $86 million to the Western Forelands Exploration Project in the DRC, $20 million to the company's joint venture in Kazakhstan, and the remaining $20 million to Ivanhoe's exploration activities in Angola, Zambia and South Africa.

Western Forelands Exploration Project, DRC

54%- to 100%-owned by Ivanhoe Mines

The Western Forelands Exploration Project consists of a licence package covering 2,427 square kilometres (km2) adjacent to the Kamoa-Kakula Copper Complex in the Democratic Republic of the Congo (DRC). The area of the Western Forelands licence package is approximately six times larger than that of the Kamoa-Kakula Copper Complex.

The Western Forelands 2026 drilling program is set to be Ivanhoe's largest to date, with more than 80,000 metres of diamond core and 16,000 metres of reverse circulation (RC) drilling planned. The diamond drilling program primarily focuses on step-out and infill drilling in the Makoko District. In addition, a 16,000-metre RC drilling program is planned for the Kamilli regional target area within the Western Forelands licence area, once the area becomes accessible in the dry season.

Nine diamond drill rigs have been operating since January, completing approximately 20,000 metres across 34 holes. All-weather drill pads and road access were constructed before the wet season, which runs from early November to late April, to enable drilling year-round. The RC program takes place only during the dry season.

The 2025 Mineral Resource for Makoko District, released on May 13, 2025, estimates 0.8 million tonnes of contained copper in the Indicated category and 8.4 million tonnes in the Inferred category, at a 1% copper cut-off. The Makoko District currently ranks as the World's fifth-largest and highest-grade copper discovery since Kakula in 2016.

An updated Mineral Resource estimate is expected to be released in Q3 2026, which will include drill results from the 2025 program and up to March 2026. This Mineral Resource update will support a pre-feasibility mine design and is scheduled for completion by Q2 2027.

The 2026 drill program aims to partially upgrade higher-grade portions of the Inferred Mineral Resource to the Indicated Mineral Resource category, as well as expand the total footprint of the Makoko District, which is open to the south and east.

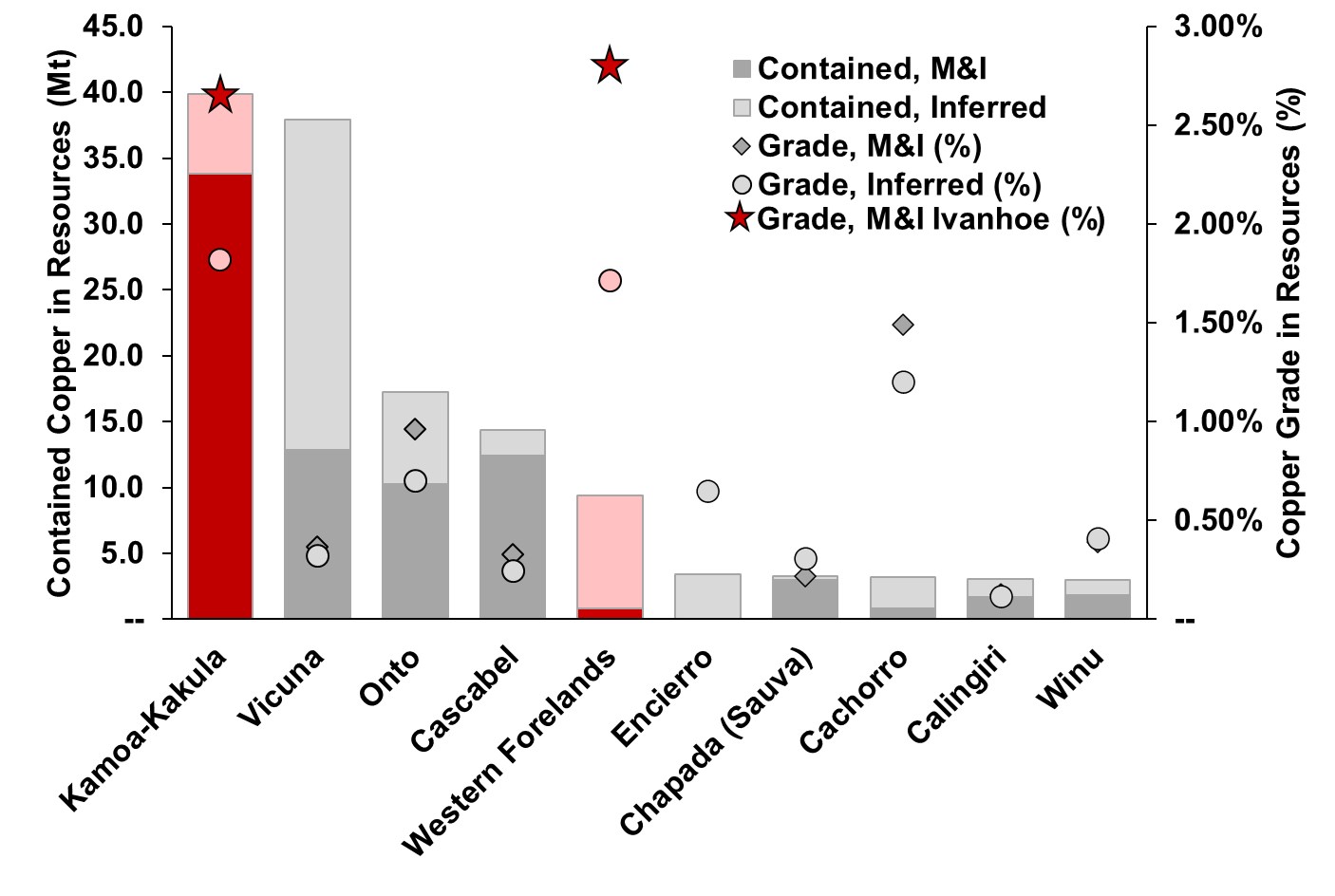

The Makoko District ranks as the world's highest-grade and fifth-largest copper discovery of the past decade. Ivanhoe's geologists have discovered a total of 52.5 million tonnes (115.7 billion pounds) of contained copper in the Western Forelands shelf, including Kamoa-Kakula.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_012full.jpg

Source: Company filings, S&P Global Market Intelligence.

Notes: Chart ranks all other new copper discoveries made since 2015 based on contained copper in resources on a 100% basis. Information based on public disclosure as of May 5, 2026. Kamoa-Kakula Copper Complex consists of the deposits of Kamoa (discovered by Ivanhoe Mines in 2008) and Kakula (discovered by Ivanhoe Mines in 2015). The Mineral Resource estimate for Kamoa-Kakula is as at March 31, 2026. Vicuña is a combination of both the Mineral Resources of Filo Del Sol and Josemaria. Mineral Resources estimates for the Western Forelands include the Makoko District (consisting of Makoko, Makoko West, Kitoko) and Kiala at a 1.0% cut-off grade, as at May 1, 2025. Data has not been reviewed by S&P Global.

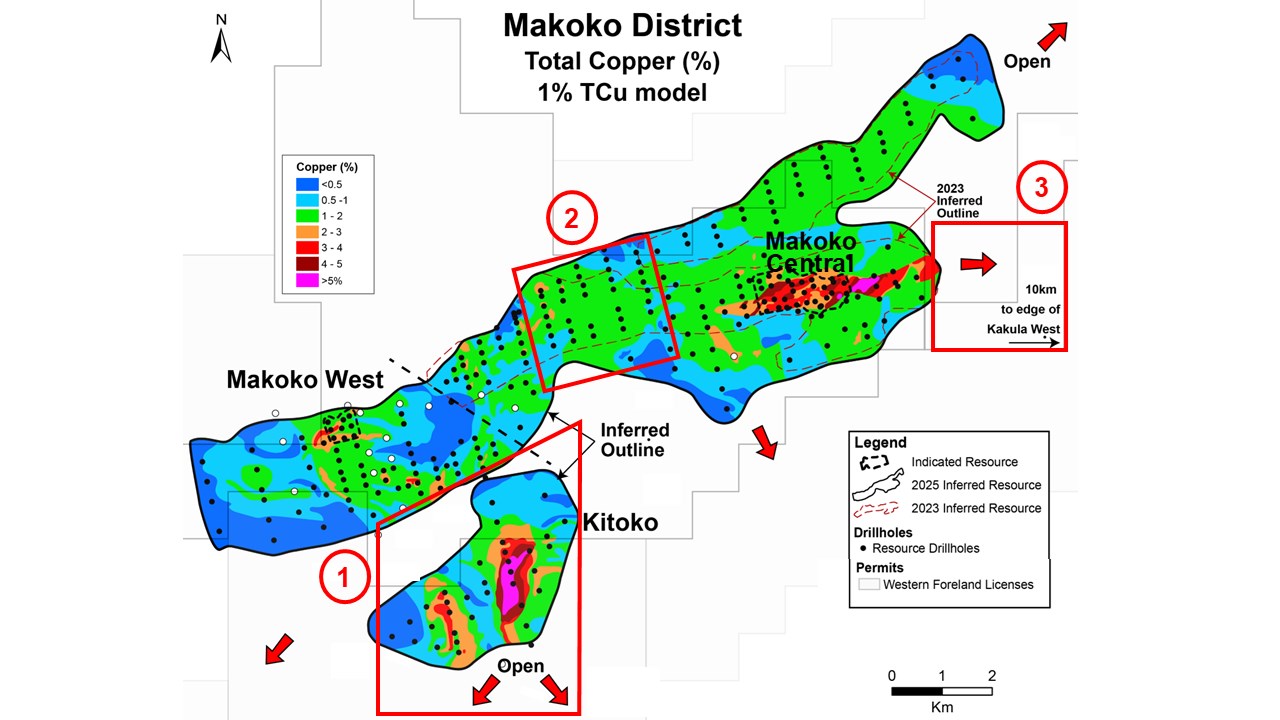

Footprint of Makoko District continues to expand; Makoko now within eight kilometres of Kakula West

Diamond drilling of the Makoko District is focused on three main areas, as shown in Figure 1 below.

Step-out drilling continues to confirm the extension of Makoko Central to the east and down-dip to the south. Since the 2025 Mineral Resource estimate, the strike length of the Makoko District has increased by two km, to 15 km. In-fill drilling aims to reduce the spacing between drill holes to less than 200 metres to upgrade Inferred resources to the Indicated category. The program will include drilling for geotechnical and metallurgical test work, which will inform the engineering studies expected to start in H2 2026.

Exploration activities in the Western Forelands will ramp up with the imminent onset of the dry season. Improved access during the dry season will significantly improve the productivity of exploration activities. An additional two diamond drill rigs are expected to be mobilized in the coming weeks, in addition to the RC drill rigs.

Plan view of the outline of the Makoko District Mineral 2025 Resource at a 1% cut off, outlining the three main areas for drilling in 2026.

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_013full.jpg

Following the success of the audio-magnetotellurics and magnetotellurics (AMT-MT) geophysics survey completed in 2025, further AMT-MT surveys are planned during the dry season. A wireline geophysics program is also scheduled to begin in Q2 2026. Properties collected in this program will be used to enhance the interpretation of existing high-resolution airborne geophysical datasets.

A diamond drilling crew from Titan Drilling of Lubumbashi, DRC, drilling in the Western Forelands

To view an enhanced version of this graphic, please visit:

https://images.newsfilecorp.com/files/3396/296293_90bddb00f42b590f_014full.jpg

North-Western Province, Zambia

100%-owned by Ivanhoe Mines

Ivanhoe's geologists believe that the Central African Copperbelt extends further west from the Western Forelands basin into western Zambia and eastern Angola.

Ivanhoe Mines was awarded a 7,757-square-kilometre (km²) exploration licence package, located in a highly strategic area of Zambia's North-Western Province in early Q2 2025. The 100%-owned landholding is over three times larger than Ivanhoe's Western Forelands Exploration Project and is situated between the company's existing DRC assets and the Angolan exploration licences. Ivanhoe's significantly underexplored licence package in Zambia has the potential to unlock the next generation of copper discoveries.

Initial exploration activities in 2025 were focused on analyzing historical geophysical and geological data from the licence's previous owners, as well as conducting an airborne gravity gradiometer (AGG) and magnetics survey. Data analysis from the surveys has generated four target areas across the licence for follow-up drilling.

The 2026 exploration program consists of both drilling the identified target areas and conducting further geophysical surveys. Tenders for both work programs were awarded in Q1 2026, with site mobilization expected following approval of the environmental project brief by the Zambian Environmental Management Authority (ZEMA). A 7,000-metre diamond drilling program across 14 holes is planned for the upcoming dry season and is expected to commence in the coming month.

Moxico and Cuando Cubango Provinces, Angola

100%-owned by Ivanhoe Mines

Ivanhoe Mines is leveraging its proven exploration expertise from the Western Forelands and Kamoa-Kakula to unlock a major new frontier in Angola. The company has secured approximately 22,000 km² of highly prospective exploration licences in the Moxico and Cuando Cubango provinces, one of the largest greenfield sediment-hosted copper exploration packages in the region.

Following the signing of a mining investment contract with Angola's National Agency for Mineral Resources on November 27, 2023, with limited to no prior exploration to date, exploration activities commenced with airborne magnetic and airborne gravity geophysical mapping of the full 22,000 km2 licence package in June 2024. Ivanhoe's exploration team then commenced a 600-km² baseline soil geochemical sampling. Other field work completed since consists of ground-based geophysical work, including Audio-frequency Magnetotellurics (AMT), Magnetotellurics (MT), and Passive Seismic surveys.

A 12-hole stratigraphic drill program was started in late 2025 and paused after one drill hole was completed due to the onset of the wet season. Drilling recently restarted and is expected to be completed by the end of the year. Currently, one diamond drill rig is operating, with a second expected to commence imminently.

The Chu-Sarysu Basin Exploration Joint Venture, Central Kazakhstan

20%-owned by Ivanhoe Mines

Ivanhoe Mines has established a strategic exploration joint venture with UK-based Pallas Resources to unlock the potential of the Chu-Sarysu Copper Basin in Kazakhstan. The basin is recognised as the world's third-largest sediment-hosted copper district. The partnership covers a vast and highly prospective 16,708 km² licence area, enriched by a comprehensive archive of Soviet-era exploration data.

Under the agreement announced on February 12, 2025, Ivanhoe has committed to $18.7 million in exploration funding over an initial two-year period, with the option to increase its ownership stake to 80% through staged earn-in milestones.

The initial $18.7 million investment has been fully drawn down for the initial geophysical and diamond-drilling program, which began in Q3 2025. From May 2026, an additional $20 million will be invested in the joint venture, more than doubling the planned drill program to approximately 40,000 metres. The additional budget will be allocated across all licences, thereby increasing Ivanhoe's earn-in across them all.

Regional and prospect-scale geophysical and geochemical surveys, as well as the stratigraphic drilling completed to date, have shown significant promise across the underexplored, high-potential copper district.

Mokopane Feeder Project, South Africa

100%-owned by Ivanhoe Mines

Ivanhoe Mines is advancing exploration on the Northern Limb of South Africa's Bushveld Complex, adjacent to Ivanplats' flagship Platreef Mine. The company is targeting a significant gravity-high anomaly interpreted as a potential massive nickel-copper sulphide primary feeder zone for the region's rich mineralization, including the world-class Flatreef deposit.

Following the completion of comprehensive geological and geophysical data analysis in early 2024, Ivanhoe has identified multiple drill targets. A 6,000-metre diamond drilling program commenced in Q1 2025, with 3,300 metres completed across two holes by the end of 2025. No drilling was completed in Q1 2026. Drilling is expected to restart in the second quarter. Exploration activities in the first quarter focused on reprocessing historic seismic data to further generate drill targets.

SELECTED QUARTERLY FINANCIAL INFORMATION

The following table summarizes selected financial information for the prior eight quarters. Revenue from commercial production at the Kipushi Mine commenced in Q4 2024. All revenue from production at Kamoa-Kakula is recognized within the Kamoa Holding joint venture. Ivanhoe did not declare or pay any dividend or distribution in any financial reporting period.

| Three months ended | ||||||||||||

| March 31, | December 31, | September 30, | June 30, | |||||||||

| 2026 | 2025 | 2025 | 2025 | |||||||||

| $'000 | $'000 | $'000 | $'000 | |||||||||

| Revenue | 165,529 | 138,435 | 129,403 | 96,757 | ||||||||

| Cost of sales | (132,537 | ) | (120,518 | ) | (122,151 | ) | (100,217 | ) | ||||

| Finance income | 43,895 | 45,099 | 43,855 | 43,583 | ||||||||

| Share of (loss) profit from joint venture | (42,040 | ) | 45,647 | 11,305 | 15,704 | |||||||

| General administrative expenditure | (19,428 | ) | 4,518 | (2,068 | ) | (10,378 | ) | |||||

| Exploration and project evaluation expenditure | (15,951 | ) | (19,722 | ) | (10,324 | ) | (8,585 | ) | ||||

| Deferred tax (expense) recovery | 3,157 | (32,995 | ) | 3,169 | 7,842 | |||||||

| Finance costs | (4,132 | ) | (9,314 | ) | (20,920 | ) | (4,947 | ) | ||||

| Share-based payments | (2,604 | ) | (5,324 | ) | (6,194 | ) | (4,447 | ) | ||||

| (Loss) profit attributable to: | ||||||||||||

| Owners of the Company | 17 | 54,687 | 33,057 | 44,051 | ||||||||

| Non-controlling interests | (2,045 | ) | (14,774 | ) | (2,505 | ) | (8,726 | ) | ||||

| Total comprehensive (loss) income attributable to: | ||||||||||||

| Owners of the Company | (29,917 | ) | 83,544 | 55,839 | 60,900 | |||||||

| Non-controlling interest | (5,095 | ) | (11,687 | ) | (3 | ) | (7,066 | ) | ||||

| Basic profit per share | 0.00 | 0.04 | 0.02 | 0.03 | ||||||||

| Diluted profit per share | 0.00 | 0.04 | 0.02 | 0.03 | ||||||||

| Three months ended | ||||||||||||

| March 31, | December 31, | September 30, | June 30, | |||||||||

| 2025 | 2024 | 2024 | 2024 | |||||||||

| $'000 | $'000 | $'000 | $'000 | |||||||||

| Revenue | 77,020 | 40,818 | - | - | ||||||||

| Cost of sales | (81,771 | ) | (51,563 | ) | - | - | ||||||

| Share of profit from joint venture | 107,948 | 73,620 | 83,507 | 89,616 | ||||||||

| Finance income | 41,623 | 56,041 | 60,164 | 62,873 | ||||||||

| General administrative expenditure | (9,957 | ) | (19,633 | ) | (10,573 | ) | (12,345 | ) | ||||

| Exploration and project evaluation expenditure | (9,145 | ) | (15,845 | ) | (12,813 | ) | (10,589 | ) | ||||

| Finance costs | (7,838 | ) | (6,849 | ) | (471 | ) | (32,871 | ) | ||||

| Deferred tax (expense) recovery | 4,374 | 12,663 | 575 | 1,398 | ||||||||

| Share-based payments | (2,418 | ) | (2,977 | ) | (7,504 | ) | (8,505 | ) | ||||

| Loss on fair valuation of embedded derivative liability | - | - | (4,171 | ) | (20,727 | ) | ||||||

| Profit (loss) attributable to: | ||||||||||||

| Owners of the Company | 129,760 | 99,344 | 117,942 | 76,401 | ||||||||

| Non-controlling interests | (7,560 | ) | (11,338 | ) | (9,760 | ) | (9,885 | ) | ||||

| Total comprehensive income (loss) attributable to: | ||||||||||||

| Owners of the Company | 135,033 | 60,964 | 141,525 | 88,223 | ||||||||

| Non-controlling interest | (7,161 | ) | (15,158 | ) | (7,469 | ) | (8,672 | ) | ||||

| Basic profit per share | 0.10 | 0.07 | 0.09 | 0.06 | ||||||||

| Diluted profit per share | 0.10 | 0.07 | 0.09 | 0.06 | ||||||||

DISCUSSION OF RESULTS OF OPERATIONS

Review of Ivanhoe Mines ("Ivanhoe" or the "Company") for the three months ended March 31, 2026 vs. March 31, 2025

The Company recorded a loss for Q1 2026 of $2 million and total comprehensive loss of $35 million compared to a profit of $122 million and total comprehensive income of $128 million for the same period in 2025. The main contributor to the loss for period was the Company's share of loss from the Kamoa Holding joint venture of $42 million. The Kamoa Holding joint venture incurred a loss for the quarter as a result of a $183 million tax adjustment in settlement of tax claims related to tax audit assessments of Kamoa Copper in prior years.

Kamoa Copper files a tax return annually. The DRC tax authorities then have up to 5 years to audit and raise any disputes regarding the company's filings. Differences can arise due to ambiguity in mining taxation in the DRC. When disputes arise, DRC companies can either follow judicial proceedings or settle the matter before it goes to court. Kamoa Copper's tax settlement pertains to disputes raised for the 2022 to 2024 tax years. It is Kamoa Copper's expectation that the $183 million settlement will close out any income tax disputes up to the end of 2024. The total income tax expense previously paid for the period from 2022 to 2024 was $729 million.

The total comprehensive loss for the three months ended March 31, 2026, included an exchange loss on translation of foreign operations of $33 million, compared to an exchange gain on translation of foreign operations recognized for the same period in 2025 of $6 million, resulting mainly from the strengthening of the South African Rand by 3% from December 31, 2025, to March 31, 2026.

Included in general and administrative expenditure for the three months ended March 31, 2026 is foreign exchange losses of $7 million whereas the general and administrative expenditure for the same period in 2025 included a foreign exchange loss of $1 million.

Ivanhoe's exploration and project evaluation expenditure amounted to $16 million for the three months ended March 31, 2026 and was $9 million for the same period in 2025. Of the total exploration and project evaluation expenditure for the first quarter of 2026, $5 million related to the Company's Kazakhstan exploration, $1 million related to the Company's Angolan exploration, and the remainder ($10 million) related mainly to exploration at Ivanhoe's Western Forelands exploration licences.

Finance income amounted to $44 million for the three months ended March 31, 2026, and $42 million for the same period in 2025. Included in finance income is the interest earned on loans to the Kamoa Holding joint venture to fund past development which amounted to $36 million for the three months ended March 31, 2026, and $34 million for the same period in 2025.

Review of the Kamoa-Kakula Copper Complex for the three months ended March 31, 2026 vs. March 31, 2025

The Kamoa-Kakula Copper Complex sold 66,619 tonnes of payable copper in Q1 2026, realizing revenue of $862 million for the Kamoa Holding joint venture, compared to 109,963 tonnes of payable copper sold for revenue of $973 million for the same period in 2025. The Company recognized a loss in aggregate of $6 million from the joint venture for the three months ended March 31, 2026 and income of $142 million for the same period in 2025, which can be summarized as follows:

| Three months ended | ||||||

| March 31, | ||||||

| 2026 | 2025 | |||||

| $'000 | $'000 | |||||

| Company's share of (loss) profit from joint venture | (42,040 | ) | 107,948 | |||

| Interest on loan to joint venture | 36,254 | 34,080 | ||||

| Company's (loss) income recognized from joint venture | (5,786 | ) | 142,028 | |||

The Company recognized its share of loss from the Kamoa Holding joint venture of $42 million in Q1 2026 compared to a profit of $108 million the same period in 2025 and is broken down in the following table:

| Three months ended | ||||||

| March 31, | ||||||

| 2026 | 2025 | |||||

| $'000 | $'000 | |||||

| Revenue from contract receivables | 872,539 | 922,411 | ||||

| Remeasurement of contract receivables | (10,237 | ) | 50,986 | |||

| Revenue | 862,302 | 973,397 | ||||

| Cost of sales | (572,576 | ) | (453,263 | ) | ||

| Gross profit | 289,726 | 520,134 | ||||

| General and administrative costs | (64,807 | ) | (34,520 | ) | ||

| Amortization of mineral property | (4,171 | ) | (4,996 | ) | ||

| Profit from operations | 220,748 | 480,618 | ||||

| Finance costs | (87,123 | ) | (59,356 | ) | ||

| Foreign exchange loss | (12,885 | ) | (815 | ) | ||

| Finance income and other | 5,559 | 5,316 | ||||

| Impairment (1) | - | (9,177 | ) | |||

| Profit before taxes | 126,299 | 416,586 | ||||

| Current tax expense | (221,658 | ) | (102,228 | ) | ||

| Deferred tax expense | (19,007 | ) | (47,938 | ) | ||

| (Loss) profit after taxes | (114,366 | ) | 266,420 | |||

| Non-controlling interest of Kamoa Holding | 29,436 | (48,343 | ) | |||

| Total comprehensive (loss) income for the period attributable to the owners of the joint venture | (84,930 | ) | 218,077 | |||

| Company's share of (loss) profit from joint venture (49.5%) | (42,040 | ) | 107,948 | |||

(1) The impairment recognized for the three months ended March 31, 2025, relates to the generators damaged in the fire that occurred on-site in January 2025.

Of the $862 million of revenue recognized by Kamoa-Kakula during the three months ended March 31, 2026, $50 million relates to the sale of 107,700 tonnes of sulphuric acid.

The realized, provisional and forward copper prices used for the remeasurement (mark-to-market) of contract receivables for the three months ended March 31, 2026, and for the same period in 2025, can be summarized as follows:

| Three months ended | ||||||

| March 31, | ||||||

| 2026 | 2025 | |||||

| Realized during the period - open at the start of the period | ||||||

| Opening forward price ($/lb.)(1) | 5.64 | 4.01 | ||||

| Realized price ($/lb.)(1) | 5.79 | 4.14 | ||||

| Payable copper tonnes sold | 36,666 | 79,985 | ||||

| Remeasurement of contract receivables ($'000) | 12,254 | 21,811 | ||||

| Realized during the period - new copper sold in the current period | ||||||

| Provisional price ($/lb.)(1) | 5.92 | 4.11 | ||||

| Realized price ($/lb.)(1) | 5.78 | 4.28 | ||||

| Payable copper tonnes sold | 39,696 | 45,527 | ||||

| Remeasurement of contract receivables ($'000) | (11,869 | ) | 16,807 | |||

| Open at the end of the period - open at the start of the period | ||||||

| Opening forward price ($/lb.)(1) | 5.63 | - | ||||

| Closing forward price ($/lb.)(1) | 5.52 | - | ||||

| Payable copper tonnes sold | 13,583 | - | ||||

| Remeasurement of contract receivables ($'000) | (3,372 | ) | - | |||

| Open at the end of the period - new copper sold in current period | ||||||

| Provisional price ($/lb.)(1) | 5.64 | 4.35 | ||||

| Closing forward price ($/lb.)(1) | 5.52 | 4.44 | ||||

| Payable copper tonnes sold | 26,922 | 64,436 | ||||

| Remeasurement of contract receivables ($'000) | (7,250 | ) | 12,368 | |||

| Total remeasurement of contract receivables ($'000) | (10,237 | ) | 50,986 | |||

| (1) Calculated on a weighted average basis | ||||||

The finance costs recognized in the Kamoa Holding joint venture can be broken down as follows:

| Three months ended | ||||||

| March 31, | ||||||

| 2026 | 2025 | |||||

| $'000 | $'000 | |||||

| Interest on shareholder loans | 73,205 | 68,817 | ||||

| Interest on provisional and advance payment facilities | 24,257 | 40,197 | ||||

| Interest on syndicated loans | 11,266 | 11,243 | ||||

| Interest on bank loans and overdraft facilities | 18,965 | 7,498 | ||||

| Lease liability unwinding | 1,610 | 1,783 | ||||

| Interest on equipment financing facilities | 1,383 | 1,757 | ||||

| Rehabilitation unwinding | 1,725 | 2,253 | ||||

| Interest capitalized as borrowing costs | (45,288 | ) | (74,192 | ) | ||

| 87,123 | 59,356 | |||||

Review of the Kipushi Mine for the three months ended March 31, 2026 vs. March 31, 2025

The Company sold 54,940 tonnes of payable zinc produced by the Kipushi Mine in the first quarter of 2026, realizing revenue of $162 million at a cost of sales of $129 million. This is compared to 30,108 tonnes of payable zinc sold for the same period in 2025, realizing revenue of $77 million at a cost of sales of $82 million. The cost of sales for Q1 2026 also included depreciation and amortization of $25 million, which was $14 million for Q1 2025.

The realized, provisional, and forward zinc prices used for the remeasurement (mark-to-market) of contract receivables of Kipushi for the three months ended March 31, 2026, can be summarized as follows:

| Three months ended | ||||||

| March 31, 2026 | ||||||

| 2026 | 2025 | |||||

| Realized during the period - open at the start of the period | ||||||

| Opening forward price ($/lb.)(1) | 1.41 | 1.34 | ||||

| Realized price ($/lb.)(1) | 1.47 | 1.28 | ||||

| Payable zinc tonnes sold | 32,966 | 11,596 | ||||

| Remeasurement of contract receivables ($'000) | 4,152 | (1,496 | ) | |||

| Realized during the period - new zinc sold in the current period | ||||||

| Provisional price ($/lb.)(1) | 1.51 | 1.32 | ||||

| Realized price ($/lb.)(1) | 1.47 | 1.30 | ||||

| Payable zinc tonnes sold | 23,430 | 20,432 | ||||

| Remeasurement of contract receivables ($'000) | (2,447 | ) | (878 | ) | ||

| Open at the end of the period - new zinc sold in the current period | ||||||

| Provisional price ($/lb.)(1) | 1.47 | 1.31 | ||||

| Closing forward price ($/lb.)(1) | 1.47 | 1.29 | ||||

| Payable zinc tonnes sold | 31,510 | 9,676 | ||||

| Remeasurement of contract receivables ($'000) | (305 | ) | (319 | ) | ||

| Total remeasurement of contract receivables ($'000) | 1,400 | (2,693 | ) | |||

(1) Calculated on a weighted average basis

Financial position of the Company as at March 31, 2026, vs. December 31, 2025

The Company's total assets decreased by $49 million, from $7,626 million as at December 31, 2025, to $7,577 million as at March 31, 2026. The decrease in total assets was mainly attributable to the decrease in cash and cash equivalents by $132 million, as explained below, the decrease in the Company's investment in the Kamoa Holding joint venture by $6 million, offset in part by the increase in property, plant and equipment of $53 million as project development continued at the Platreef Mine.

Cash and cash equivalents and short-term deposits decreased by $131 million, from $885 million as at December 31, 2025, to $754 million as at March 31, 2026. The Company spent $62 million on project development and acquiring other property, plant, and equipment and $71 million on its operating activities, primarily due to $65 million in interest repayments during the quarter. Of the total interest repaid during the three months ended March 31, 2026, $30 million related to the semi-annual interest repayment on the Senior Notes, $14 million related to repayments of interest on advance payment facilities, $5 million related to interest on overdraft facilities, and $4 million related to interest on other term loan facilities.

The Company's investment in the Kamoa Holding joint venture decreased by $6 million from $3,571 million as at December 31, 2025, to $3,565 million as at March 31, 2026. The Company's investment in the Kamoa Holding joint venture can be broken down as follows:

| March 31, | December 31, | |||||

| 2026 | 2025 | |||||

| $'000 | $'000 | |||||

| Company's share of net assets in joint venture | 2,244,861 | 2,286,901 | ||||

| Loan advanced to joint venture | 1,319,943 | 1,283,689 | ||||

| Total investment in joint venture | 3,564,804 | 3,570,590 |

The Company's share of the net assets in the Kamoa Holding joint venture can be broken down as follows:

| March 31, 2026 | December 31, 2025 | ||||||||||||

| 100% | 49.5% | 100% | 49.5% | ||||||||||

| $'000 | $'000 | $'000 | $'000 | ||||||||||

| Assets | |||||||||||||

| Property, plant and equipment | 7,302,950 | 3,614,960 | 7,085,455 | 3,507,300 | |||||||||

| Indirect taxes receivable | 1,123,730 | 556,246 | 1,141,769 | 565,176 | |||||||||

| Current inventory | 719,594 | 356,199 | 759,207 | 375,807 | |||||||||

| Mineral property | 740,201 | 366,399 | 744,371 | 368,464 | |||||||||

| Long-term loan receivable | 454,389 | 224,923 | 428,363 | 212,040 | |||||||||

| Other receivables | 290,975 | 144,033 | 364,097 | 180,228 | |||||||||

| Trade receivables | 483,948 | 239,554 | 336,094 | 166,367 | |||||||||

| Cash and cash equivalents | 140,090 | 69,345 | 310,590 | 153,742 | |||||||||

| Run of mine stockpile | 104,790 | 51,871 | 104,790 | 51,871 | |||||||||

| Income taxes receivable | - | - | 88,289 | 43,703 | |||||||||

| Right-of-use asset | 35,515 | 17,580 | 39,834 | 19,718 | |||||||||

| Deferred tax asset | 29,114 | 14,411 | 30,201 | 14,949 | |||||||||

| Prepaid expenses | 8,218 | 4,068 | 18,484 | 9,150 | |||||||||

| Non-current deposits | 3,127 | 1,548 | 3,127 | 1,548 | |||||||||

| Liabilities | |||||||||||||

| Shareholder loans | (2,666,792 | ) | (1,320,062 | ) | (2,593,586 | ) | (1,283,825 | ) | |||||

| Term loan facilities | (963,659 | ) | (477,011 | ) | (1,069,004 | ) | (529,157 | ) | |||||

| Advance payment facilities | (920,708 | ) | (455,750 | ) | (906,915 | ) | (448,923 | ) | |||||

| Trade and other payables | (692,173 | ) | (342,626 | ) | (675,358 | ) | (334,302 | ) | |||||

| Deferred tax liability | (387,785 | ) | (191,954 | ) | (369,851 | ) | (183,076 | ) | |||||

| Overdraft facility | (282,169 | ) | (139,674 | ) | (276,430 | ) | (136,833 | ) | |||||

| Rehabilitation provision | (133,614 | ) | (66,139 | ) | (132,004 | ) | (65,342 | ) | |||||

| Income taxes payable | (100,009 | ) | (49,504 | ) | - | - | |||||||

| Dividends payable | (51,100 | ) | (25,295 | ) | (87,242 | ) | (43,185 | ) | |||||

| Provisional payment facilities | (76,433 | ) | (37,834 | ) | (80,756 | ) | (39,974 | ) | |||||

| Lease liability | (39,783 | ) | (19,693 | ) | (44,075 | ) | (21,817 | ) | |||||

| Other provisions | (52,138 | ) | (25,808 | ) | (34,806 | ) | (17,229 | ) | |||||

| Non-controlling interest | (535,205 | ) | (264,926 | ) | (564,641 | ) | (279,497 | ) | |||||

| Net assets of the joint venture | 4,535,073 | 2,244,861 | 4,620,003 | 2,286,901 | |||||||||

Before commencing commercial production in July 2021, the Kamoa Holding joint venture principally used loans from its shareholders to develop the Kamoa-Kakula Copper Complex through investing in development costs and other property, plant, and equipment.

Advance payment facilities represent financing arrangements linked to Kamoa-Kakula's offtake agreements with its customers. Each customer has provided advance payment facilities which are repaid by offsetting amounts payable in terms of provisional invoices in accordance with the terms of each agreement.

The repayments of the advanced payment facilities of the Kamoa Holding joint venture can be summarized as follows:

| More than | |||||||||||||||

| 0-3 months | 3-6 months | 6-12 months | 12-24 months | 24 months | |||||||||||

| $'000 | $'000 | $'000 | $'000 | $'000 | |||||||||||

| At March 31, 2026 | 24,708 | 12,000 | 52,000 | 632,000 | 200,000 | ||||||||||

Overdraft facilities represent drawn unsecured financing facilities from DRC financial institutions at an attractive cost of capital, utilized to augment cash generated from operations for Kamoa-Kakula's continued expansion and working capital. Total current overdraft facilities amount to $337 million, with an interest rate of approximately 6.5%.

The term loan facilities of the Kamoa Holding joint venture, incur interest at a weighted average rate of 8.53% per annum and can be summarized as follows:

| Description | Repayment terms | Maturity date | March 31, | December 31, |

| 2026 | 2025 | |||

| $'000 | $'000 | |||

| Syndicated term facility | Repayable in eight equal quarterly installments starting from March 31, 2026 | Dec-27 | 350,711 | 398,868 |

| Standard Bank facility agreement | Full repayment on July 2026 with extension option. | Jul-26 | 200,576 | 198,870 |

| Equipment financing facilities | Installments on each quarterly facility repayment date | Dec-27 | 28,923 | 34,951 |

| Bank of Africa facility | Repayable in monthly installments | Nov-26 | 11,525 | 15,623 |

| United Bank for Africa loan facility | Interest is paid bi-annually & the principal is repaid on maturity. | Oct-26 | 123 | 50,472 |

| Offshore Term facility | Interest is paid quarterly & four quarterly payments of the principal amount starting on 31 December 2026 and eight (80%) of the principal on maturity. | Oct-27 | 371,801 | 370,221 |

| Total term loan facilities | 963,659 | 1,069,004 |

The repayments of the term loan facilities of the Kamoa Holding joint venture can be summarized as follows:

| More than | |||||