The Conversation (0)

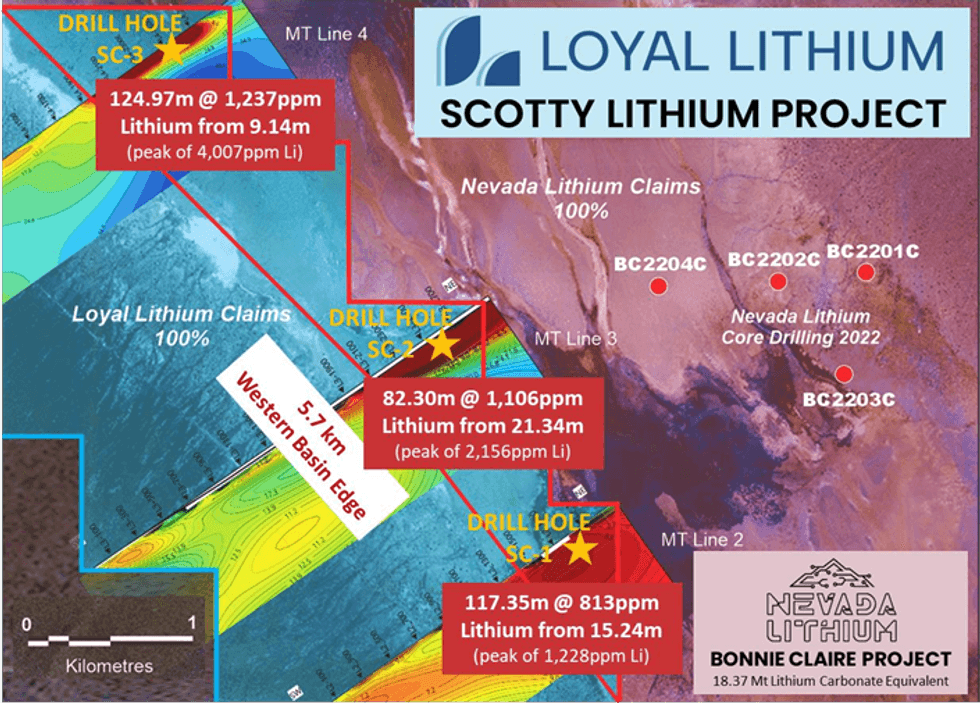

Loyal Lithium Limited (ASX: LLI) (Loyal or the Company) is thrilled to confirm the discovery of a significant lithium basin at the 100% owned Scotty Lithium Project in Nevada, USA. The average lithium grade of the drillholes measures 1,120ppm with a 700ppm cut-off, starting near the surface (9m deep) and spans a 3.6km² area with an average thickness of 108m. Drilling and geophysics data will be utilised for a 3D model and for the creation of an Exploration Target. The basin's 5.7km western edge offers the potential for cost-effective mining due to its alluvial fan rocks, providing excellent accessibility for surface mining. Nevada Lithium’s (CSE:NVLH) neighbouring Bonnie Claire Project has successfully produced battery- grade lithium carbonate from its sedimentary basin drill cores. The Scotty Lithium Project occurs within close proximity to all-weather roads and power infostructure, and is strategically located just 40km north of Beatty, 220km from Las Vegas, and 330km from Tesla’s Nevada Gigafactory.

Highlights:

Loyal Lithium’s Managing Director, Mr Adam Ritchie, commented:

"The Scotty Lithium Project continues to deliver with spectacular drilling assay results confirming strong lithium mineralisation, representing significant resource potential.”

“With the support of a 5.7km western edge, the sedimentary basin could potentially be accessed via traditional mining solutions from surface. The neighbouring Bonnie Claire Project has recently completed pilot plant test work to produce a high-grade lithium carbonate from the adjoining sedimentary clay”.

“Nevada lithium is alive, and the Scotty Lithium Project has shown its potential to play a significant role in the emerging North American lithium supply chain.”

Figure 1: Scotty Lithium Project –Mineralised Sedimentary Basin - MT traverses projected to the horizontal

Figure 1: Scotty Lithium Project –Mineralised Sedimentary Basin - MT traverses projected to the horizontal

Project and Exploration Program Overview

The Scotty Lithium Project is located 220 km northwest of Las Vegas, NV and is contained within the Sarcobatus Flat, a known lithium-bearing sediment basin. Nevada Lithium’s (CSE:NVLH) neighbouring Bonnie Claire Project is also contained within the same basin. Early this year, Nevada Lithium purchased Iconic Minerals Ltd. who in 2021 completed a PEA on the resource at the Bonnie Claire project.8

Click here for the full ASX Release

This article includes content from Loyal Lithium Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.