The Conversation (0)

Reach Resources Limited (ASX: RR1 & RR1O) (“Reach” or “the Company”) engaged globally renowned geological consultants RSC Consultants Limited (RSC) to assess the potential of the Company’s Gascoyne projects for:

HIGHLIGHTS

CEO Jeremy Bower commented:

“RSC’s independent expert analysis confirms our belief that our landholding in the Gascoyne has the potential to host significant battery metal deposits.

Phase 1 of the assessment focused on the lithium potential at our Critical Elements Projects and has not only cemented Morrissey Hill as our primary lithium target but importantly has identified three new lithium target areas. Each of the areas are defined by the presence of a highly fertile parent granite and supported by key multi-element geochemistry including lithium, caesium, tantalum, tin and rubidium which are all well documented associations of lithium bearing “rare metal” LCT pegmatite mineral systems.

This is an exciting time for the Company and our shareholders, and we look forward to delivering updates to the market over the coming months. The Future is within Reach”.

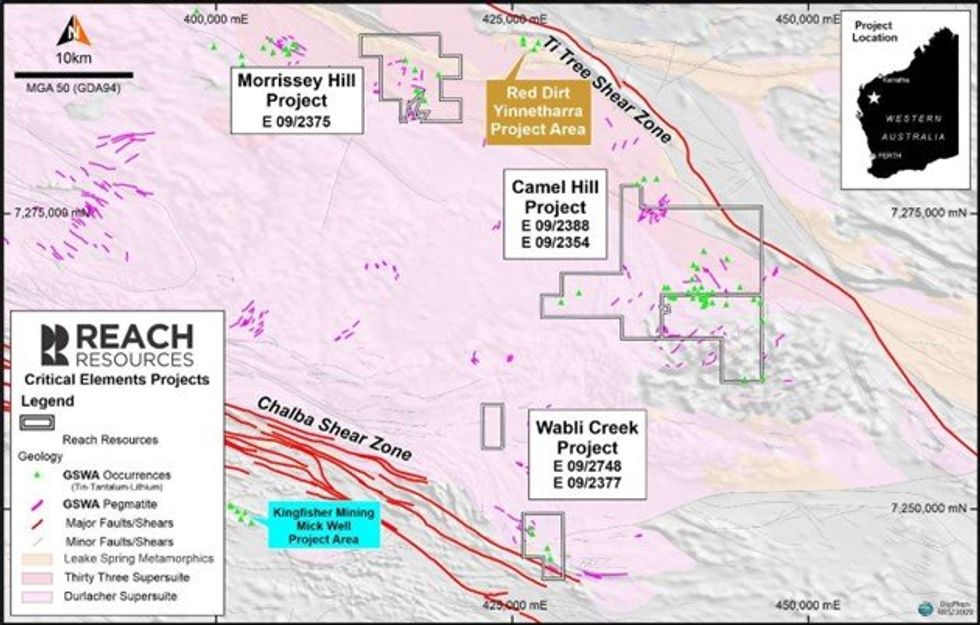

Phase 1 of the assessment focused on the lithium potential of the Company’s Critical Elements Projects which includes the newly acquired Morrissey Hill and Camel Hill projects as well as the Wabli Creek project (Figure 1).

Figure 1: Critical Elements Projects

Figure 1: Critical Elements Projects

The assessment included a review of relevant deposit models and mineralisation styles of interest, regional and local geology, local mineral systems, academic papers, open file company and government reports and all available geochemical, geophysical and remote-sensed data sets.

Click here for the full ASX Release

This article includes content from Reach Resources, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.