The Conversation (0)

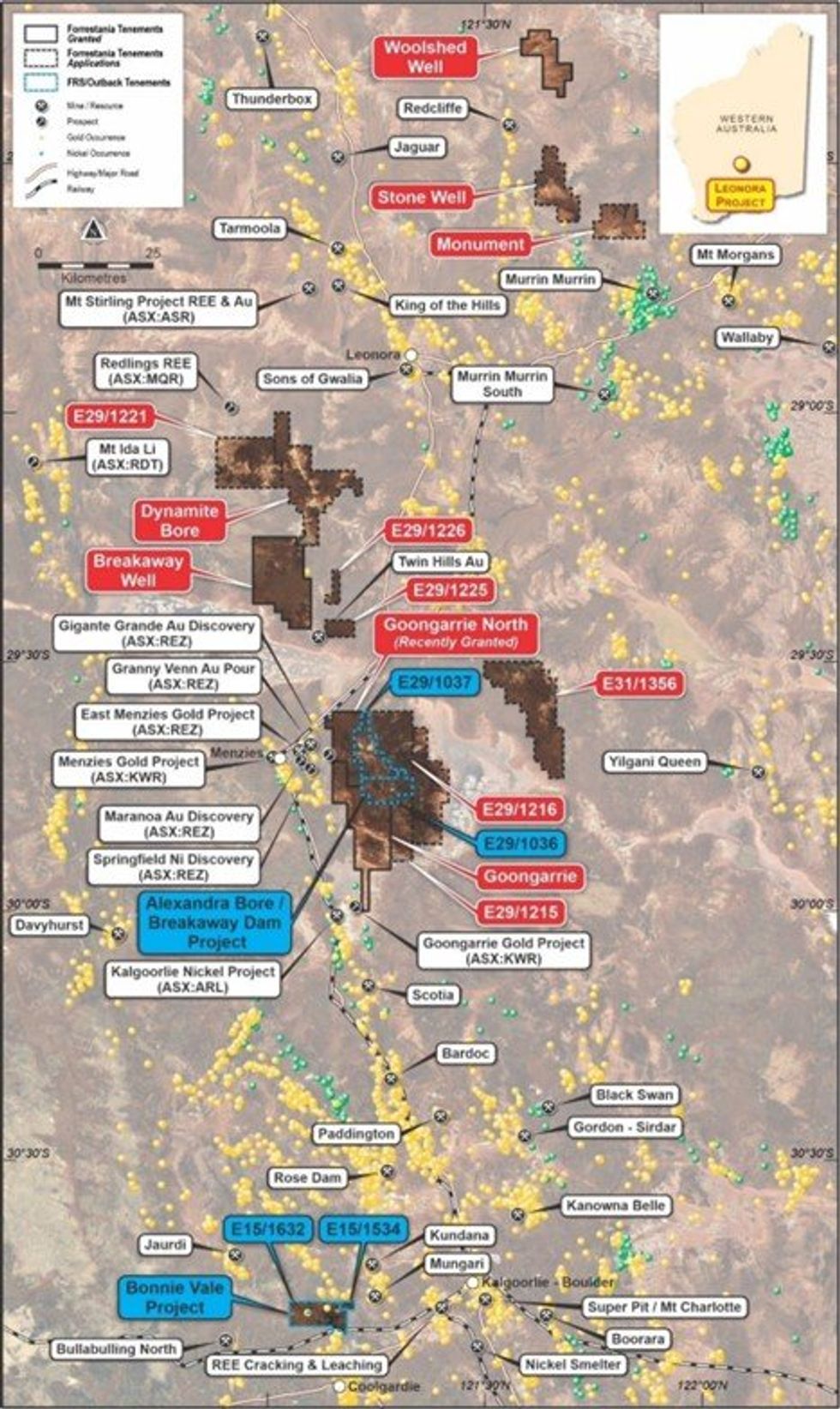

Forrestania Resources Limited (ASX:FRS) (Forrestania or the Company), is pleased to provide an update on activities at its Eastern Goldfields project area located north of Coolgardie and north of Kalgoorlie, around the gold mining districts of Leonora, Coolgardie and Menzies (see figure 1). The Eastern Goldfields project area comprises eighteen tenements (eight ELs and ten EL applications) that are strategically located over areas that the Company believes are highly prospective for multi-commodities, particularly lithium, gold, REE and copper.

Highlights:

“The rationale for entering into the option agreement with Outback Minerals already appears to be justified. The confirmed presence of multiple pegmatite outcrops, some up to ~100m in strike length, provides us with additional confidence in the discovery potential on these tenements. We are prioritising our activities to prepare for a maiden drilling programme, as soon as possible.”

Discussion:

The Company has recently completed a mapping and reconnaissance field trip to the newly acquired Eastern Goldfields tenements. The focus of the trip was to further enhance the Company’s geological understanding of the project areas, as well as to further assess the potential for lithium mineralisation.

The newly acquired tenements (Alexandra Bore / Breakaway Dam project (E29/1037 and E29/1036) have never previously been explored for their lithium potential, with previous historic exploration instead focussed on copper, gold and nickel, despite the known presence of pegmatites.

The Bonnie Vale project area (E15/1534 and E15/1632) has also never been explored for its lithium potential, with previous explorers focussing on the tenement’s gold prospectivity.

Mapping and field work is on-going, but the company is pleased to announce that additional pegmatites have been mapped at both project areas, specifically on E29/1037 and E15/1632.

Figure 1: The Eastern Goldfields project area (recent acquisitions highlighted in blue)

Figure 1: The Eastern Goldfields project area (recent acquisitions highlighted in blue)

Alexandra Bore / Breakaway Dam Project (E29/1037 and E29/1036) and Balarky Prospect (E29/1158)

The Company recently completed a mapping and reconnaissance field trip to the newly acquired Alexandra Bore / Breakaway Dam project area (see Figure 2).

Pegmatites have previously been mapped by the company at the Alexandra Bore / Breakaway Dam project areas1 and ongoing field reconnaissance is currently underway.

Significantly, additional pegmatite outcrops have recently been mapped at surface by Company geologists, with outcropping pegmatites ranging from ~43m and up to ~100m in strike length (see Figures 3, 4, 5 and 6). These pegmatites were located approximately 300m apart and have never previously been tested for lithium or LCT pathfinder minerals. Indeed, the Alexandra Bore / Breakaway Dam project area has only previously been explored for copper and gold1 and the potential for lithium mineralisation has yet to be fully evaluated. Importantly, these outcrops are all located within the mapped greenstone or close to greenstone/granite contacts (as interpreted by GSWA).

Click here for the full ASX Release

This article includes content from Forrestania Resources, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.