The Conversation (0)

Latin Resources Limited (ASX: LRS) (“Latin” or “the Company”) is pleased to advise that it has secured an additional 1.2 kilometres of tenure covering the interpreted southern strike extension of the Company’s 100% owned high-grade Colina Lithium Prospect (“Colina”). The Company has also dispatched samples to the laboratory, to commence preliminary metallurgical test work as part of the Company’s fast-track strategy.

HIGHLIGHTS

Colina High-Grade Lithium Prospect

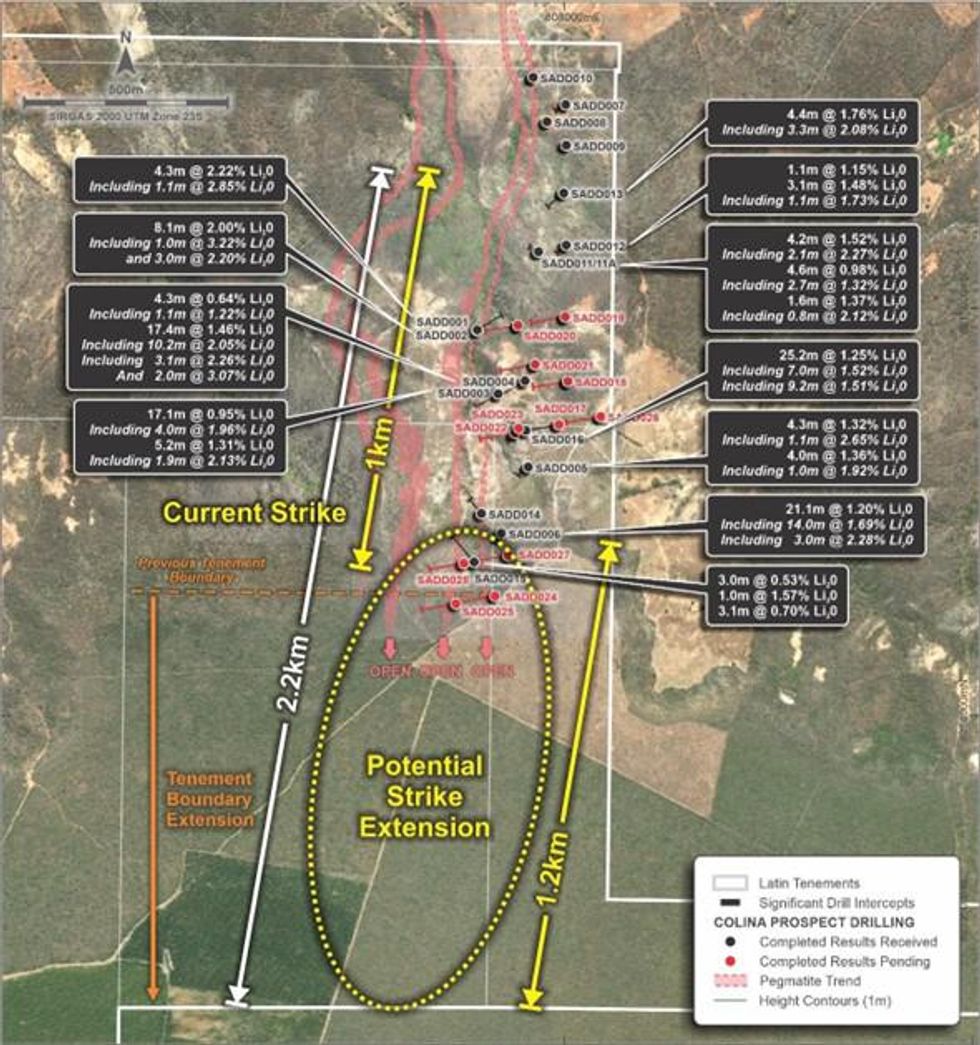

Latin is pleased to announce that it has secured additional exploration rights covering the area directly along strike to the south of the high-grade Colina Project (Figure 2 and Figure 3), where drilling has confirmed the presence of thick, high-grade, near surface pegmatites. The new option agreement extends the Company’s 100% tenure a further 1.2 kilometres to the south, where drilling shows the pegmatites remain open, with the southern most drillhole targeting the main pegmatites, SADD006, returning an intersection of 21.1m @ 1.2%Li2O1.

Figure 1: New diamond drilling rig on site at Colina

The resource definition campaign is well underway at Colina, there has been 25 holes drilled for a total of 4800 metres. There are now three diamond rigs drilling, with a fourth rig arriving in late July. The plan is for a total of over 100 holes to be drilled for an estimated 25,000m of diamond core drilling to be completed. This program is likely to be expanded to include step out drilling to the south to outline the full strike extent of the identified pegmatites, as well as deeper holes to test for additional stacked pegmatites as previously announced2.

Figure 2: Colina Prospect, showing new tenure covering interpreted strike extensions, completed drill collars3 and significant intersections received to date

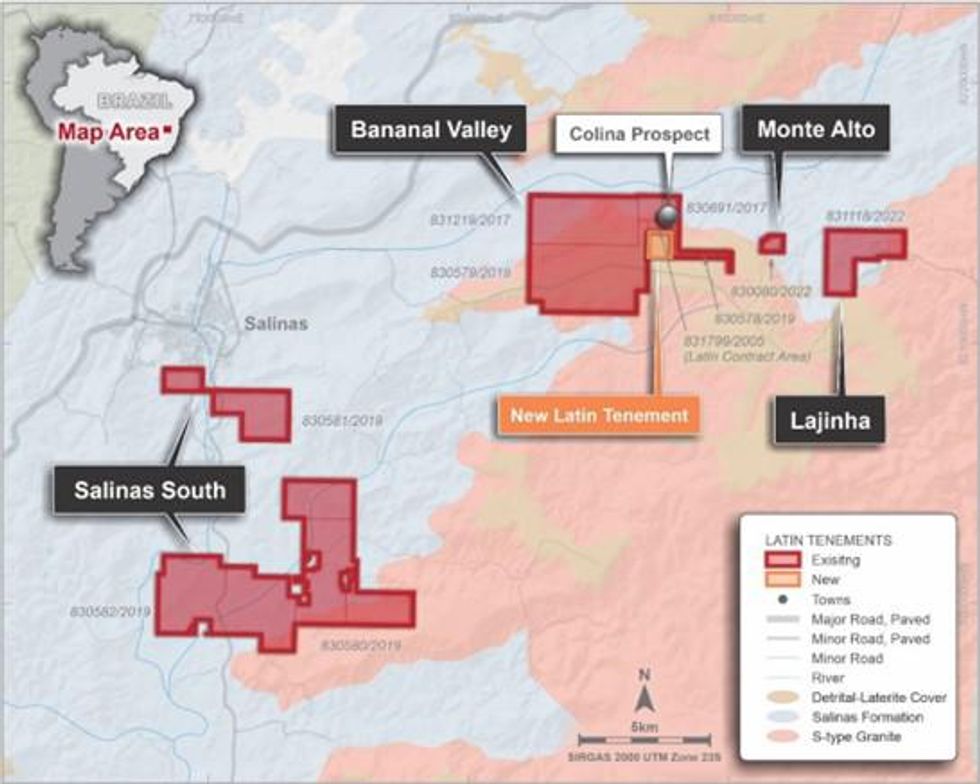

Figure 3: Regional Salinas Lithium Project tenure

Colina High-Grade Lithium Prospect – Metallurgical Test Work

The Company can confirm that samples have now been received at the SGS laboratory in Brazil, enabling the commencement of the planned preliminary metallurgical test work on the Colina lithium pegmatite. The planned test work will include Dense Media Separation (“DMS”) and flotation testing to determine lithium recovery into final concentrates, and detailed mineralogical and petrological studies to confirm individual miner species present in the Colina pegmatite.

Click here for the full ASX Release

This article includes content from Latin Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.