The Conversation (0)

Critical Metals Corp. (Nasdaq: CRML) (“Critical Metals Corp” or the “Company”), a leading critical minerals mining company, today announced for the first time three new assay results from the 2024 diamond drill hole program at the Fjord Deposit at the Tanbreez Rare Earth Project in Greenland.

Highlights – 2024 New Diamond Drill Hole Results

Tony Sage, Executive Chairman of the Company, commented:

“These additional 2024 diamond drill hole results indicate the consistent grades of rare earth and gallium, with a high proportion of critical heavy rare earths. Our rare earth grades and gallium concentration, position Tanbreez as a strategically important asset for Western supply chains. With China's control over the rare earth market and gallium, securing sources of these critical minerals has become paramount for U.S. defense capabilities and national security. The progress we've made, with 1,316 meters of diamond core drilling completed in 2024, and over 1,850 meters of drilling as part of our 2025 Fjord Resource Upgrade resource extension program, significantly strengthens our ability to build on our substantial resource base. With further assays pending and more drilling underway, we see strong potential to grow the scale and nature of the project's mineral inventory.”

Summary New Drill Hole Results

Drill hole collars and assay Tables 1 and 2 and Figure 1 and Appendix 1, 2 and 3.

| Hole ID | Depth (m) | TREO (%) | HREO (% of TREO) | ZrO₂ (%) | Ga₂O₃ (ppm) | ||||||

| D-24 | 85.70 | 0.42 | 26.3% | 1.58 | 99 | ||||||

| E-24 | 62.30 | 0.40 | 26.5% | 1.57 | 93 | ||||||

| F-24 | 107.45 | 0.40 | 25.5 | 1.57 | 93 | ||||||

| Cut-off | 0.30 |

Table 1 – 2024 New assay results summary for D-24, E-24, F-24

New Drill Hole Results

Drill Hole D-24

Drilled vertically to 85.7m from surface and intersected high-grade rare earths and metal oxides mineralisation averaging:

Drill Hole E-24

Drilled vertically to 62.3m from surface and intersected high-grade rare earths and metal oxides mineralisation averaging:

Drill Hole F-24

Drilled vertically to 107.45m from surface and intersected high-grade rare earths and metal oxides mineralisation averaging:

Figure 1 - Tanbreez Site Visit August 29 Malcolm Day Director CRML, Greg Barnes JV Partner, George Karageorge CTO, Anna Wingle Tanbreez Mining Greenland

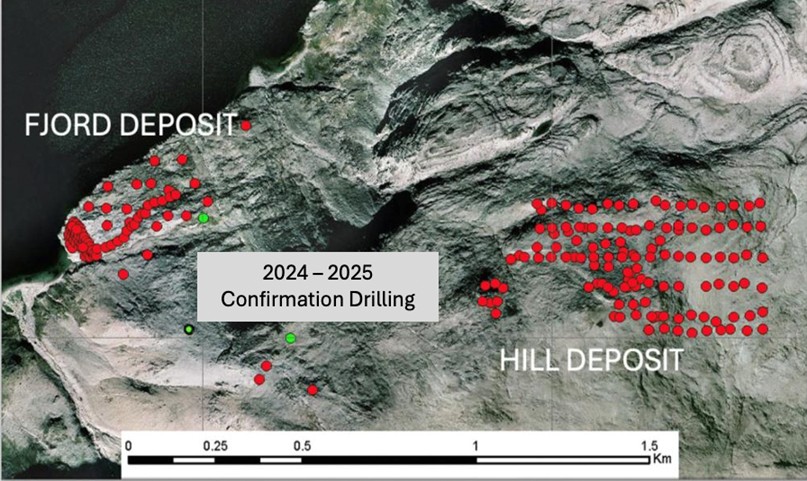

Figure 2 - Fjord and Hill Deposit drill hole locations for 2007, 2010, 2013, 2024 in red with 2025 drill hole collars completed in July with 9 diamond holes awaiting drilling.

Drill Hole Statistics

Drill hole collars and assay Tables 1 and 2 and Figure 1 and Appendix 1, 1A , 2 and 3.

| Hole ID | Depth From | Depth To | Interval | TREO% | HREO% | ZrO2 % | Ta2O5 ppm | Nb2O5 ppm | Ga2O5 ppm | |

| A1-24 | - | 40.00 | 40.00 | 0.48 | 0.13 | 1.86 | 134 | 1513 | 103 | |

| A2-24 | - | 41.00 | 41.00 | 0.51 | 0.14 | 1.96 | 145 | 1685 | 96 | |

| B-24 | - | 58.00 | 58.00 | 0.49 | 0.13 | 1.99 | 144 | 1651 | 101 | |

| C-24 | - | 65.00 | 65.00 | 0.54 | 0.14 | 1.98 | 156 | 1741 | 89 | |

| D-24 | 1.00 | 63.00 | 62.00 | 0.42 | 0.11 | 1.58 | 112 | 1344 | 99 | |

| E-24 | 1.00 | 62.30 | 61.30 | 0.40 | 0.11 | 1.57 | 105 | 1336 | 93 | |

| F-24 | 0.00 | 72.00 | 72.00 | 0.40 | 0.10 | 1.57 | 103 | 1256 | 93 |

Table 2 - 2024 Drill Hole Assay results summary to date 2024 diamond drill hole program in the Fjord Area. Assay results are reported for drill holes D, E and F. A1, A2, B and C were reported on 22 August 2025. Remaining assay results for holes G to Z are expected to be reported in Q3, 2025.

Background – Fjord Deposit Drilling

The 2024–2025 drilling campaign in the Fjord area has targeted confirmatory and step-out holes to:

All drill holes in this program are vertical, intersecting the sub-horizontal layers at true thickness. The three holes reported here return TREO grades between ~0.40% and 0.42% with approximately 26% HREO, along with ZrO₂ values of 1.57–1.58% and gallium oxide contents of 93–99 ppm. These results are consistent with historical assays and demonstrate the persistence of grade and mineralogy across the Fjord deposit.

From a deposit classification perspective, the kakortokite-hosted REE mineralisation is best described as stratiform magmatic, confined entirely to the kakortokite unit and not observed in adjacent lithologies such as lujavrite or naujaite. This strong lithological control underpins confidence in resource modelling, supports bulk mining strategies, and provides reliable input for geology domaining.

Given the continuity of mineralization over several kilometres, the Fjord deposit represents a significant portion of the overall Tanbreez mineral inventory. Ongoing drilling is expected to further delineate these resources, with pending assays from additional holes likely to extend the known mineralised envelope and refine the grade distribution.

Sampling over the 2024 diamond holes was taken over kakortokite intervals above the Black Madonna lower boundary.

Gallium Results

The gallium oxide Ga2O3 mineralization assay results ranges from low to high is 90ppm to 100ppm for the four 2024 drillholes published to date.

Drill holes that were not assayed for gallium, tantalum and niobium in 2013 will be assayed from existing pulps submitted to ALS Metallurgical in Perth for analysis in the coming months.

ALS laboratories will also assay all sample for gallium for the 2024 and 2025 drill holes with results that will be published in September and October 2025. The gallium oxide results for all diamond holes published to date may add a credit to the TREO-HREO mixed concentrate.