The Conversation (0)

Asara Resources Limited (ASX: AS1; Asara or Company) is pleased to announce that it has signed a binding Subscription Agreement with Barbet L.L.C FZ (Barbet) to raise $2.3m (Placement) which affirms Barbet’s commitment to the Company and its flagship asset, the Kada Gold Project in Guinea (Kada).

Following completion of the Placement, Mr. Timothy Strong has stepped down as Managing Director and Mr. Matthew Sharples has been appointed Chief Executive Officer. Mr. Strong will remain on the Board as Executive Director – Corporate Strategy & Affairs.

Executive Director, Tim Strong commented:

‘’We are pleased that Barbet have continued to show their commitment to the Company and its flagship Kada project by participating in a further Placement. This Placement will allow the Company to fastrack its exploration efforts.

I am also delighted to welcome Matt Sharples to the management team. Matt, who joined the Company as a consultant in October 2024, has been instrumental in recommencing operations at Kada. Matt provides a wealth of knowledge, and an undeniable passion for Guinea and I look forward to supporting him as we move the Kada project through the value chain towards a feasibility study. Both Matt and I are confident of the resource potential of Massan and the surrounding areas which will be drill tested in the coming months.’’

Placement Details

The Placement is comprised of the issue of 104,517,541 fully paid ordinary shares (Placement Shares) at an issue price of $0.022 raising $2,299,385.90 (before costs). per share. Following the Placement, Barbet holds 19.89% of the Company.

The proceeds of the Placement will be applied towards an upcoming drill program and exploration activities at Kada and general working capital. The Placement Shares will be issued under the Company’s existing placement capacity under ASX Listing Rule 7.1, and accordingly no shareholder approval is required. The Placement Shares will rank pari passu with existing securities on issue.

Executive Changes

Chief Executive Officer

Matthew has been appointed Chief Executive Officer, effective 14 February 2025. Matthew Sharples is a mining professional with over 20 years of experience in mine development, investment consulting and M&A. Matt specialises in the geological evaluation and development of gold projects, with a particular focus on project development from the initial stage to production.

Matt was Co-Founder and CEO of the private mining fund Sycamore Mining. Under his stewardship, the group's flagship asset, the Kiniero Mine (Guinea), grew from a total resource base of 1.5Moz Au to 3.5Moz Au (JORC) and was sold to Robex Resources in 2022 for a project valuation of US$160m. Matt has worked worldwide in the mining and resources industry, in the UK, Africa, Asia and Australia, with Robex, Sycamore, Wood Mackenzie, Xstrata and BHP Billiton.

Matt holds an MSc in Basin Evolution and Dynamics, Royal Holloway, University of London, United Kingdom, and a BSc in Geology, University of Durham, United Kingdom. Matt is a director and shareholder of substantial shareholder, Barbet L.L.C FZ.

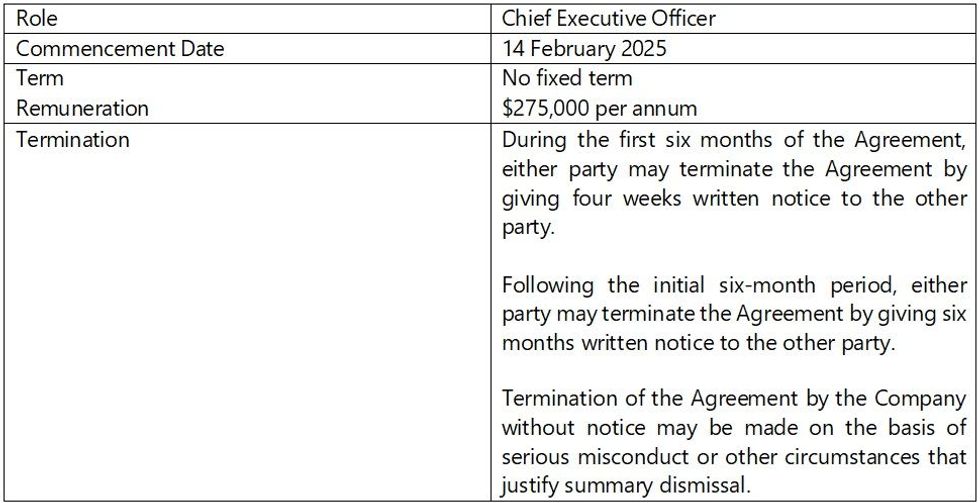

The material terms of Matthew Sharple’s employment agreement are as follows:

Click here for the full ASX Release

This article includes content from Asara Resources Limited, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.