The Conversation (0)

Surefire Resources NL (“Surefire” or “the Company”) is delighted to announce the results of the Pre-Feasibility Study (PFS) for the Company’s flagship Victory Bore Project, located close to existing infrastructure with direct transport links to Geraldton Port in Western Australia.

The Company has commenced discussions with interested Saudi companies as partners in the KSA processing operation, and is arranging meetings at the forthcoming Future Minerals Forum (FMF) being held January 2024 in Riyahd, KSA.

The PFS was completed to an accuracy of +/- 25% to 35%, on time, and on-budget and undertaken by METS Engineers, Snowden Optiro, together with other specialist groups providing reliable cost estimates, and using conservative commodity pricing.

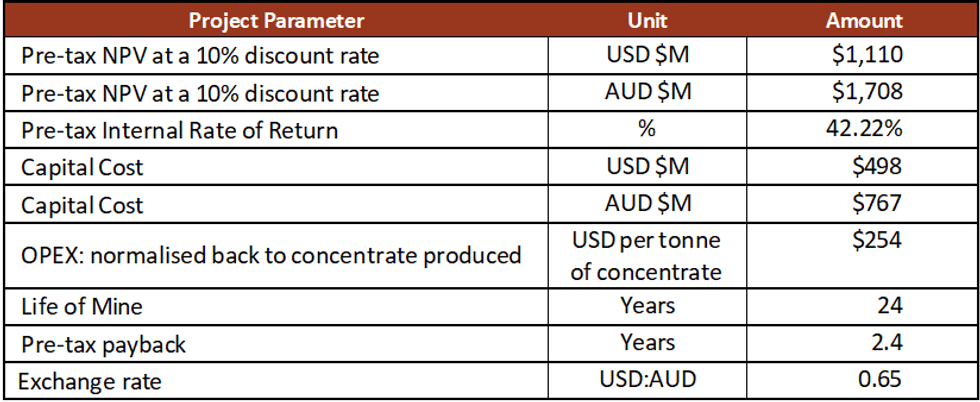

Table 1 Summary of project economics estimate. All values are approximate rounded to nearest significant digit.

Table 1 Summary of project economics estimate. All values are approximate rounded to nearest significant digit.

The Company’s approach to this maiden and landmark study of the Victory Bore Project is to use industry standard processing for a range of products to maximise the value, allowing for a reliable and demonstrable low-risk business concept. These outstanding financial results demonstrate that offshore processing is the correct approach in a global economic backdrop of rising capital and operating costs (Figure 1).

The Company has a non-binding Memorandum of Understanding (MoU) in place with the Ministry of Investment Saudi Arabia (MISA) for vanadium and critical mineral processing in the Kingdom of Saudi Arabia (see ASX announcement 16 August 2023).

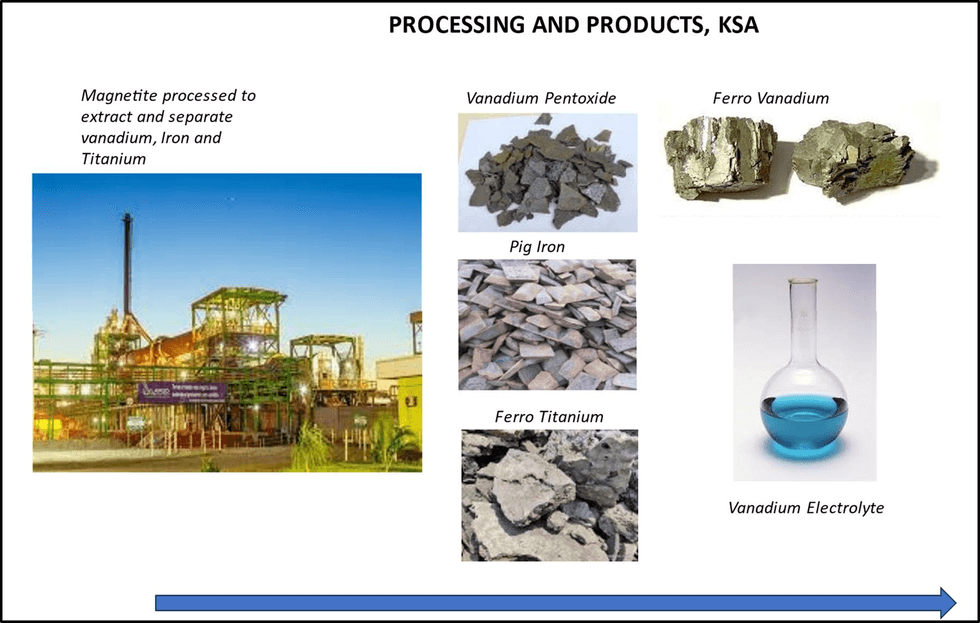

The Company’s engagement with the Kingdom of Saudi Arabia (KSA) as a low power and fuel cost jurisdiction, allows the project significant advantages of reduced operating costs, and producing final products for nearby markets. The KSA has a significant steel sector with demand for vanadium products, including ferrovanadium and vanadium electrolyte for Vanadium Redox Batteries.

Management Comment: Mr Paul Burton, Surefire Resources Managing Director said “This is an outstanding result for our world class critical minerals project and shows that in the current economic environment, offshore processing is the right approach to getting this project into development and production. We look forward to taking this project forward, completing the next significant milestones and engaging with KSA companies interested in being part of our project and development”.

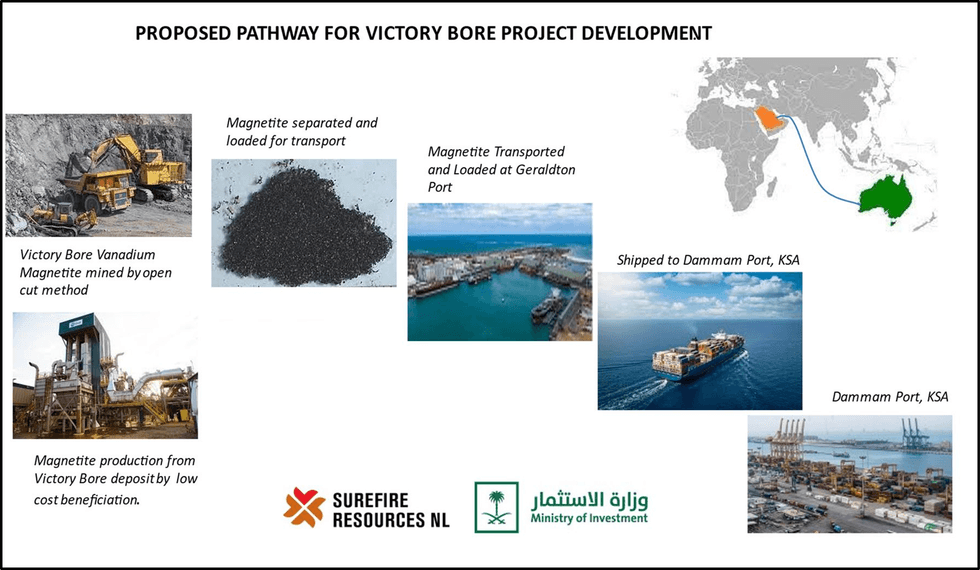

Figure 1 Development proposal for the Victory Bore Vanadium Project: mining and concentrate production in Australia, final product production in the low cost jurisdiction of the KSA.

Figure 1 Development proposal for the Victory Bore Vanadium Project: mining and concentrate production in Australia, final product production in the low cost jurisdiction of the KSA.

SUMMARY OF KEY PFS RESULTS

Surefire has based the PFS on producing approximately 1.25 million tonnes per year (Mt/a) of high quality vanadium- titanium magnetite concentrate at the Victory Bore mine site in Western Australia, and to produce up to six products from that concentrate in KSA:

Note: The final product mix may differ in a future Feasibility Study as processes may be optimised further to maximise recoveries and revenues.

Click here for the full ASX Release

This article includes content from SUREFIRE RESOURCES NL, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.