The Conversation (0)

Frontier Energy Limited (ASX: FHE; OTCQB: FRHYF) (Frontier or the Company) engaged independent specialist energy and resources consultancy ResourcesWA, to undertake an assessment (the Report) of Western Australia’s major electricity network, the South West Interconnected System (SWIS).

The Report focused on evaluating potential capacity for large scale connections at existing substations and terminals across the 330kV and 220kV transmission network, from now until 2032.

This Report was commissioned by the Company to gain a better understanding of new large- scale developments on the SWIS, similar to the potential of the Bristol Spring Renewable Energy Project (the Project) in the short to medium term.

The development of multiple, large scale energy projects on the SWIS would affect wholesale electricity prices (if supply outstripped demand) and therefore potential returns on Frontier’s Stage One Project development that is planned to commence in 2024.

The Report however concluded that “there are no other opportunities that exist on the SWIS for the development of a connected generator of the scale of the Bristol Spring Renewable Energy Project in the short or medium term”. The reasons for this include:

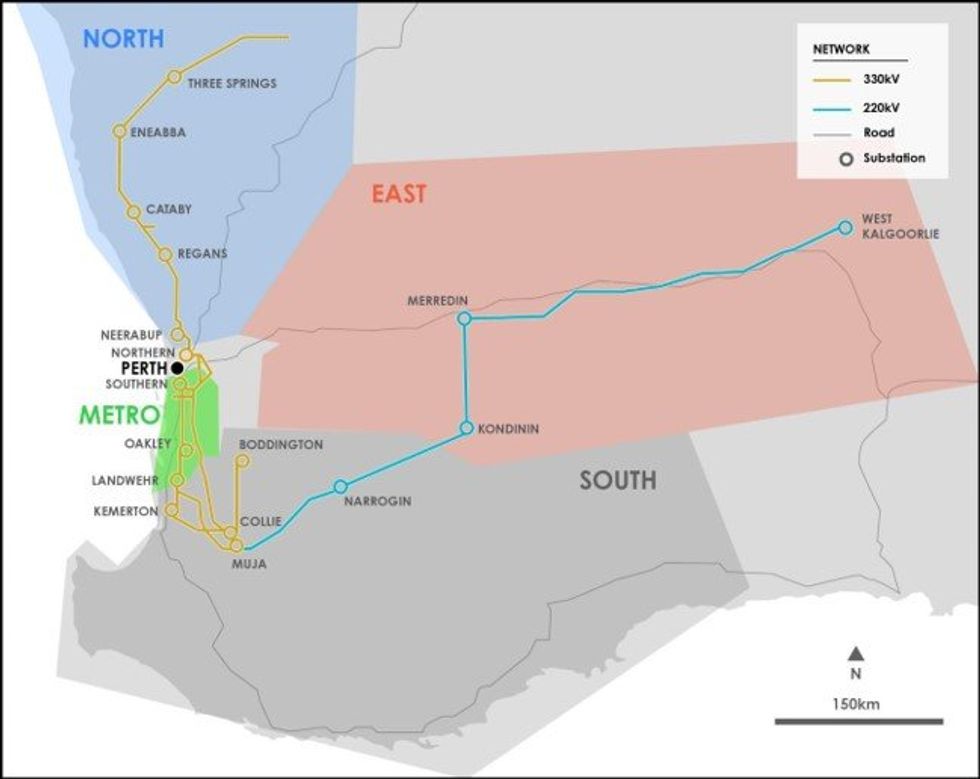

Figure 1: SWIS 330kV – 220kV network and Regions

Figure 1: SWIS 330kV – 220kV network and Regions

The Report supports the Australian Energy Market Operator annual Wholesale Electricity Market Electricity Statement of Opportunities (ESOO Report), which stated “the urgency of advancing generation, storage, demand side management and transmission projects to bolster reliability and support a rapid and orderly energy transition. Its findings emphasise the need for additional capacity procurement and expedited progress of capacity projects in the SWIS.” The ESOO Report also highlighted demand is forecast to increase significantly over the next decade to at least 78% (Expected Case), with an Upside Case increasing by more than 220%.

A copy of the ESOO "Report is attached to this announcement.

Frontier Managing Director, Sam Lee Mohan, commented: “While we always believed the Bristol Springs Renewable Energy Project was the best undeveloped renewable energy project in WA, we did not appreciate that it is the only project of its size that can access the SWIS network in the short to medium term. This again highlights what a unique opportunity the Company has with the Project, as well as the growing importance of the Project to the State, at a time when energy prices are continuing to rise and energy security is becoming more important than ever.

The next few months are shaping up as the most significant in the Company’s history with multiple major events on the horizon. First, we expect to complete the acquisition of Waroona Energy Inc. in December 2023. This transaction will then be followed by a DFS for Waroona’s Stage One Solar development (120MW) as well as the Peaking Plant Study expected to be released in 1Q24.”

This article includes content from Frontier Energy, licensed for the purpose of publishing on Investing News Australia. This article does not constitute financial product advice. It is your responsibility to perform proper due diligence before acting upon any information provided here. Please refer to our full disclaimer here.