The Conversation (0)

With a market capitalization of approximately C$10 million and no debt, Riverside Resources (TSXV:RRI) has successfully advanced over 80 exploration projects and has completed seven successful spinouts and royalty transactions over its 17-year history. Founded in 2007, the company focuses on precious and base metals, with a unique business model designed to minimize financial risk while maximizing exploration opportunities.

Riverside's diversified portfolio spans different geographies and commodities, including gold, silver, copper and rare earth elements (REE) in Ontario and British Columbia in Canada, and across Mexico. Riverside is well-capitalized, with over $5 million in cash on hand, no debt, and a well-established royalty portfolio. This strong financial position allows the company to continue exploring new opportunities while reducing operational risks.

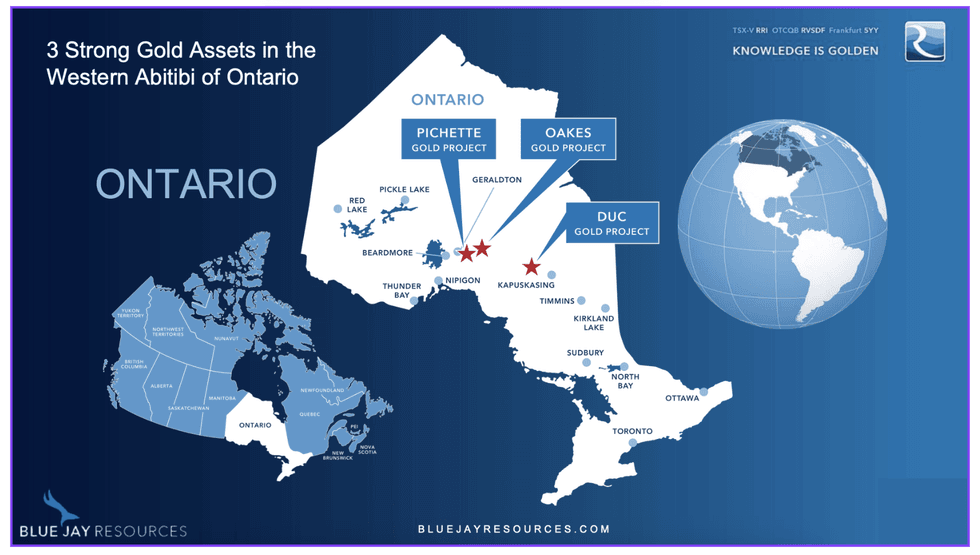

Riverside Resources' Ontario-based gold projects are located in the Western Abitibi region, one of Canada's most prolific gold-producing areas. The company's assets are near Equinox Gold's Greenstone gold mine, which provides significant potential for future development or acquisition. The Greenstone mine is expected to produce more than 390,000 ounces of gold annually for the first five years of its over 15 years of mine life. As this mine nears the end of its life, Riverside's nearby properties could provide valuable ore, potentially making them attractive targets for acquisition by Equinox or other major players in the region.

This Riverside Resources profile is part of a paid investor education campaign.*

Click here to connect with Riverside Resources (TSXV:RRI) to receive an Investor Presentation